First Deflation, Then Inflation. But the Timing…?

-

John Mauldin

John Mauldin

- |

- June 2, 2012

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinUS Unemployment Turns Back South

A Synchronized Global Slowdown

Why Would You Buy a Bond with Negative Interest?

First Deflation, Then Inflation

New York, Madrid, Tuscany, and Singapore

A New Adventure

And Bad Dad

One of the more frequent questions I am asked in meetings or after a speech is whether I think we will have inflation or deflation. My ready answer is, "Yes." Then I stop, which I must admit is rather fun, as the person who asked tries to digest the answer. And while my answer is flippant, it's also the truth, as I do expect both outcomes. So the follow-up question (after the obligatory chuckle from the rest of the group) is for a few more specifics. And the answer is that I expect we will first see deflation and then inflation, but the key is the timing. Today we will examine that question in more detail, as we look at how interest rates could actually be negative (!!!) this week in German and Swiss bonds and why the US ten-year has dipped below 1.5%. The very poor May employment number needs some analysis, too, and we'll check the prospects of a synchronized global slowdown. Rarely have I come to a Friday with so much data that simply begs for a more thorough look, but we will try to hit at least the most important topics.

US Unemployment Turns Back South

The US unemployment numbers for May were released this morning, and they were rather dismal. Mainstream economists were expecting something on the order of 150,000 new jobs, but they came in sharply lower at 69,000. March and April estimates were revised down 50,000. As long-time readers know, I pay as much or more attention to the direction of the revisions than to the actual monthly numbers, as the direction of the revision is a reasonable leading indicator. And what it indicates is what I was writing four months ago: we are in for another summer of poor jobs growth.

With the revisions, we have had the first back to back sub-100,000 new jobs months since last summer, with the average gain for the last three months a poor 96,000.

The unemployment rate rose to 8.2%, as the labor force rose a very strong 642,000. This is why I wrote, at the beginning of this recession some four years ago, that employment would take longer to come back this cycle. That is because of the way they count employment. If you have not looked for a job in the last four weeks, you are not counted as unemployed. The rise in the labor force is largely due to the growing number of people now looking for jobs, as those on extended unemployment benefits are beginning to come to the end of their two-year benefits period in fairly large numbers each month.

As more people look for a job, the statistical reality is that it takes more new jobs to move the unemployment number down. And with numbers like this month's, that means the unemployment rate will start to march back up. That is not something anyone wants, least of all politicians, who are fond of taking credit when the number of jobs rise but try to change the subject when unemployment climbs.

The more realistic unemployment number would be one that counted people who are unemployed but would take a job if they could get one. While economists can argue how to actually come up with that number, nobody (without a serious political bias) would argue that it is less than 10%, and some would argue it's north of 12%. And the duration of unemployment is now back to a median time of over 9 months, with that number sadly rising as well. It is just taking longer to find a job if you don't have one.

CNN Money did a story last month with the note that "... there are far more jobless people in the United States than you might think. Last year, 86 million Americans were not counted in the labor force because they didn't keep up a regular job search. While it's true that the unemployment rate is falling, that doesn't include the millions of nonworking adults who aren't even looking for a job anymore. And hiring isn't strong enough to keep up with population growth. As a result, the labor force is now at its smallest size since the 1980s when compared to the broader working age population."

The household survey (which is different from the establishment [or business] survey) showed the creation of 422,000 jobs. We get the unemployment percentage (of 8.2%) from the household survey. You can't really look at the monthly numbers on the household survey, because they fluctuate wildly. "Change in the adjusted household survey over the last five months: +491,000, +879,000, -418,000, -495,000, +400,000. That nets out to +857,000, little different from the establishment survey's 823,000. Further evidence that one should look at the adjusted household numbers as a longer-term check on the establishment survey and basically ignore the monthly changes." (The Liscio Report)

The interesting thing to me in the household report was that the number of part-time jobs was up 757,000, which is far larger than the rise in the number of employed. Full-time employment actually dropped by 266,000. The broader measure of people who are unemployed or underemployed (part-time but wanting full-time work) is now back up to 14.8%. The Gallup Poll people, using a different survey basis, show an 18% underemployed rate.

But why should we worry? "The jobless rate in the U.S. could drop to as low as 6 percent by the first half of 2013, a bigger decrease than most economists currently project, according to research from the Federal Reserve Bank of New York. The relationship between the number of Americans newly unemployed and those recently finding work indicates joblessness will continue to decline, according to economist Aysegul Sahin." (BusinessWeek) Such scholarly work should help Mr. Sahin to land a job with the White House on the President's Council of Economic Advisors. Although, to be fair to the Fed, their more consensus view is that unemployment will still be 7.4% to 8.1% in the 4th quarter of 2013.)

Perhaps the key driver of the US economy is consumer spending. And consumer spending requires consumers to have income. But this month's survey and the revisions to recent reports shows that hours worked are down slightly and wages are not keeping up with inflation. Total payrolls were down 0.3% for May, which is just a killer for consumer spending. GDP for the first quarter was revised down to 1.9%, and it looks like this quarter may not be any better or may even be worse, despite the higher expectations of mainstream economists.

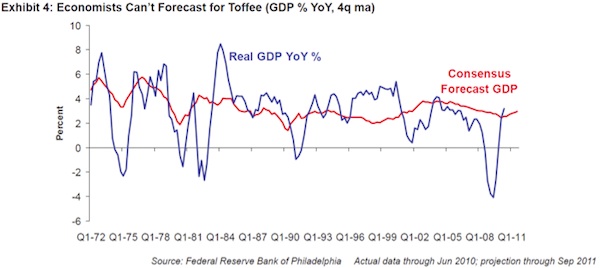

But I suggest that you not take much comfort from consensus forecasts. There are certain analysts who I can almost always count on to be wrong. And they get there with the aid of a large number of graphs and charts and words to prove their points. But being consistently wrong can be useful, and I appreciate the effort it involves. However, there is wrong and there is just really bad. The Blue Chip economics consensus has never forecast a recession. And they largely miss recoveries. Essentially, they always forecast a continuation of the current trend. As a group, they are largely useless. They are not even a good contrarian indicator.

My friend James Montier (now of GMO) has long had fun with the poor track record of consensus economic forecasts. This graph pretty much says it all.

A Synchronized Global Slowdown

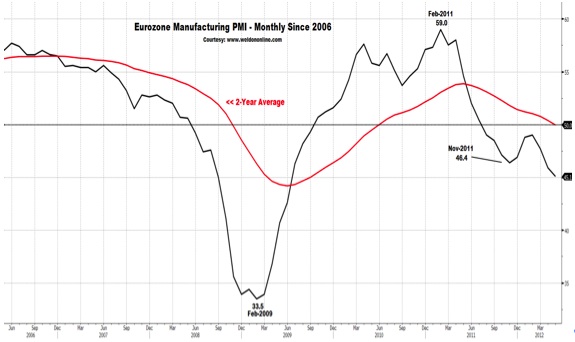

While synchronized swimming may be an event (if an odd one) at this summer's London Olympics, a synchronized global slowdown is not an event in which you want to get a medal. We looked at a spate of bad data last week, and we got even more this week. Lost in the bad employment data this morning was the news out of Asia. Australian manufacturing is clearly in a recession. India is posting its slowest growth in nine years. China is on the edge of a downturn in manufacturing. Unemployment is rising all over Europe and is much worse than in the US. German (!!!) credit default swaps are rising and are now higher than in 2008! Bank deposits in Europe are contracting at a faster rate than at any time in the last 14 years (the farthest back I can find data).

And while I don't want to steal too much thunder from next week's Outside the Box, I will pass along just this one graph from Greg Weldon (www.weldononline.com), showing that the PMI numbers for Europe came in almost universally bad. Note that the two-year average is getting ready to go negative.

Like what you’re reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

The jobs number suggests the US is at stall speed. I wrote at the beginning of the year that if someone could guarantee 2% growth for the year I would take it. That still seems like a good bet, as I don't think we are going to get near 2%. An economic shock from Europe, which is quite possible, could push the US and most of the rest of the world into recession. The weakness in China and the rest of Asia gives even more cause for concern.

Recessions are almost always by definition deflationary. And with that thought in mind, let's turn our eyes to this week's rather puzzling moves in European interest rates.

Why Would You Buy a Bond with Negative Interest?

It is entirely understandable why Spanish and Italian interest rates are rising, as the news, especially from Spain, is quite negative. But so far, there is little evidence that there is significant shorting of Spanish debt, as almost everyone believes that the European Central Bank will ride to the rescue of Spain, as it has in the recent past. That is a tough environment for short sellers. One morning you wake up and there is massive movement against your short position and you can't get out without large losses. But the longer interest rates rise without ECB intervention, the more likely they are to rise even faster at some point, forcing either an ECB intervention or a failed Spanish bond auction and an eventual default. Given that the latter events are so disastrous, it is not unreasonable to think that the ECB will act, at some point.

Yields on Spanish ten-year bonds are now at 6.62%, up 50 basis points in the last 45 days. That is a record 548 basis points higher than similar German debt. Greece, Portugal, and Ireland had to seek aid when rates rose over 7%. "Economy Minister Luis de Guindos said late yesterday that the future of the euro is at stake, as data showed a net 66 billion euros ($81 billion) of capital left Spain in March. 'I don't know if we're on the edge of the precipice, but we're in a very, very, very difficult situation,' he said at a conference in Sitges, Spain.

"Investors have lost more on Spanish debt this year than any government securities apart from those of Greece. Spain, the fourth-biggest euro economy, owes bondholders 731 billion euros, more than the three countries that have already been bailed out combined. (Prime Minister) Rajoy's suggestion that his country risks being forced out of capital markets reinforces concern that it may not be able to manage its debts..." (Bloomberg)

But in recent speeches, ECB president Mario Draghi has said that European leaders must clarify their own vision of what Europe is to be. He correctly points out that it should not be up to the ECB to fill a policy vacuum created by European inaction.

" 'Can the ECB fill the vacuum of lack of action by national governments on fiscal growth? The answer is no,' Draghi told the European Parliament. 'Can the ECB fill the vacuum of the lack of action by national governments on the structural problem? The answer is no.'

"In his sharpest criticism yet of euro zone leaders' handling of the crisis, Draghi urged they spell out detailed plans for the euro and fiscal cooperation, something he believes will require governments to surrender some of their sovereignty to succeed.

"'How is the euro going to look like a certain number of years from now? What is the union vision that you have a certain number of years from now? The sooner this is specified, the better it is,' Draghi said." (Reuters)

That does not sound like a man who wants to buy Spanish bonds. And that is why, the longer he hold off, the more the market may sense he is waiting on European leaders to act. And that may take some time, as so far all they seem to want to do is kick the much-dented can down the road.

But even given the pessimism in Europe, why should Germany be able to sell €5 billion of two-year bonds at zero percent interest last week and see them trade this week at a slightly negative interest? Why would anyone buy a bond that is guaranteed to not even give you your money back? Is that a sign of severe potential deflation?

The answer is, not really. Buying German bonds, even at a slightly negative rate, is actually a cheap call option on the eurozone breaking up. A German bond that became a new Deutschemark-denominated bond would rise in value at least 40-50% almost overnight. If you are a pension fund, for instance, with a lot of sovereign debt from a variety of European peripheral countries and you think a break-up of the eurozone is possible, it is a way to hedge your investment portfolio.

Switzerland actually sold outright this week bonds that have a negative coupon. Again, not a sign of deflation but another call option, betting that the Swiss Central Bank will have to give up on its peg to the euro. That peg has got to be one of the biggest losing trades in central banking history, and the Swiss seem determined to lose even more money. If the euro goes to $1.15 or lower, that trade becomes an even more massive loser. At what point in the next year will the Swiss Central Bank decide it has endured all the pleasure it can stand in fighting the fall of the euro? If they abandoned the peg, the move in the Swissie (as traders call the Swiss franc) would be large and almost instantaneous. And the reward for investors outside of Switzerland buying Swiss bonds with a negative yield will be large.

First Deflation, Then Inflation

As noted above, recessions are by definition deflationary. Deleveraging events are also deflationary. A recession accompanied by deleveraging is especially deflationary. That is why central banks all over the world have been able to print money in amounts that in prior periods would have sent inflation spiraling upward. This drives gold bugs nuts as they see the money being printed, but they are not factoring in the velocity of money. If the velocity of money were flat, inflation would be quite significant by now. But velocity has been falling and is going to fall even further. The US Fed and the ECB are going to be able to print more money than we can imagine without stoking inflation ... at least for a while longer.

Like what you’re reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

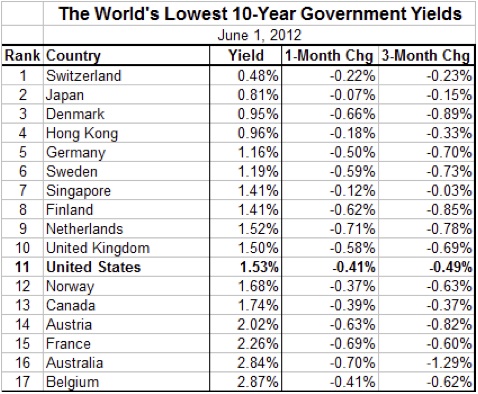

But interest rates are down in a lot of countries. Look at this table of ten-year bond yields (courtesy of Barry Ritholtz at The Big Picture):

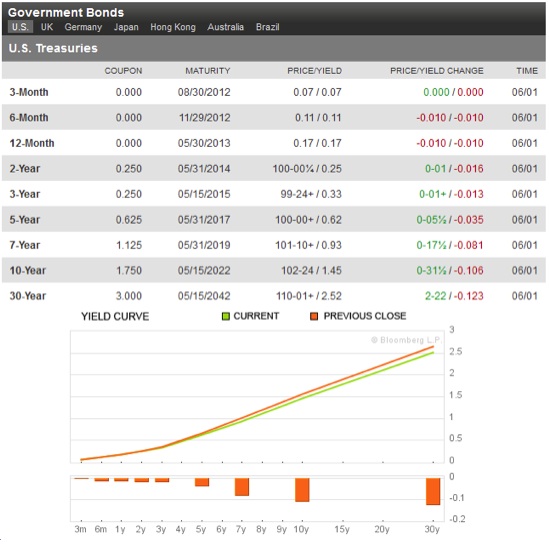

Today's employment numbers not only sent stocks tumbling and gold soaring, they had a significant effect on bond yields, which fell across the board. Look at today's numbers from Bloomberg.com. Note the 30-year US Treasury is at 2.52%!

One of the champions, for a rather long time, of the deflationary outlook has been my friend David Rosenberg (formerly chief economist at Merrill and now with Gluskin Sheff in Toronto). He has been talking for years about a target of 1.5% for the ten-year US bond. Today we got down to 1.5% and did not even pause, ending the day at 1.47%. I noted that in a phone conversation to Rich Yamarone, the chief economist at Bloomberg, and he said he believes we will scare 50 basis points before we are through. To which Rosie replied in a later text, "He's nuts." We will all be at a special evening for the University of Texas McCombs School of Business next Thursday. I will offer to hold their coats while they have a lively discussion.

Since I was thinking about bond yields, I called Dr. Lacy Hunt (one of the more brilliant economists in the country, and not just in my opinion). He has been forecasting interest rates for a long time and been the guiding light at Hoisington Asset Management, which has established perhaps the best track record I know of for bond returns, if a tad volatile. They have been long bonds for a very long time, which has been the correct position, if a difficult and lonely one. Most bond managers think rates are set to rise.

Not Lacy. He thinks we will get close to 2% on the 30-year bond and has said so for decades. (Interestingly, he will be in the audience on Thursday, along with Van Hoisington. I think I will refrain from saying anything about bonds that night and talk about something more predictable, like politics or Europe.)

Dr. Gary

Shilling wrote his first book, called simply Deflation, in 1998 and followed it up recently with another great

work, titled The Age of Deleveraging. He first went long bonds in 1982, which has been one of the great trades of

the last 30 years. He lists a whole host of reasons for a deflationary period

over the next few years.

The argument for deflation is

rather straightforward. The boom in the US and much of the world from 1982

until 2008 was partially the result of financial innovations and massive

leveraging. That process has come to its end, and the private sector is

deleveraging and will do so even further as the economy softens and we slip

into the next recession. Governments are coming to the end of their ability to

borrow money at reasonable rates in Europe, and soon in Japan and eventually in

the US (and that time is not as far off as we would like). I described the

whole process in my book Endgame.

Assuming the US government deals with its coming deficit crisis in a realistic

manner, the results will be deflationary. I will comment later on the Fed

response.

The next big deflationary force is the slowing of the velocity of money. I have written numerous e-letters and devoted a lot of space in the book to the velocity of money and won't go into it again here. It has been falling for five years, pretty much as I wrote it would, back in 2006. (I was writing about the velocity of money at least as far back as 2001, and probably earlier. It is a very important concept to grasp.) We are now close to the historical average velocity of money, but since velocity is mean-reverting it will go well below the historical average. This process takes years; it is not something that is going to end any time soon.

A slow-growth, Muddle-Through economy is deflationary. High and persistent unemployment is deflationary.

Absent some new piece of data that I can't see now, we are in for lower bond yields in the US. Rates are going lower and are going to stay low for longer than any of us can imagine.

I think the Fed will respond to the government acting in a fiscally responsible manner, which is inherently deflationary, by fighting that deflation with the only tool it has left; and that is outright monetization of debt. They will call it something else, of course, but that will be the actual outcome.

And they will be able to monetize more than you think they can without causing a repeat of the 1970s. Eventually it will catch up to us, as there is no free lunch, but they are betting they will be able to reduce some of the threat of actual inflation by cutting back on the money supply and raising rates. But we are years off from that. So, yes, at some point inflation will be back.

Anybody who says they know the timing is a lot more confident in his/her crystal ball than I am. Mine is rather cloudy on this topic. But I think I can see out a year or so, and it looks like continued low rates and deflation. By the way, just to appease the gold bugs among my readers, given my deflationary call, I will note in passing that solid gold stocks were up hugely during the deflationary Great Depression of the '30s. Even with the dollar on the gold standard. Just saying.

New York, Madrid, Tuscany, and Singapore

It is time to hit the send button, as I have to get up too early to go to New York this morning (it is already way too late). I get back Tuesday and then head to Austin on Thursday, as noted above. Then it's another quick trip to New York the following week for my partners at Altegris. I will be doing some media on that trip as well.

Like what you’re reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

The on Friday that week, hopefully after I finish my letter, I get on a plane for Rome and then Tuscany but via an overnight stay in Madrid. I normally can wait to book tickets and get reasonable prices (everything is relative), and use the system-side upgrades I get from American Airlines to fly business or first. This time nothing was working. Finally, Myra, who does my travel and stays busy at it, realized the problem was the London Olympics. Traffic flow is messed up. The best way for me to go is through Madrid. Spend the night and fly out at a civilized hour the next morning.

That means I can meet with interesting people in Madrid rather than staying in a stuffy airport hotel. But I can't eat dinner at ten PM (as is the custom) and get home at 2 AM. So I suggest a late lunch at a place that is cool. Cool trumps food. Get them both?! You are my next BBF. You drop me off at five and go on your way. You get $25,000 worth of secrets (I will only hold back one or two). The secrets of the universe for a fun dinner.

I'm back from Italy for a week, then it's off to NYC for a day. That night I fly to Singapore from JFK, through Frankfurt. While the speaker fee was quite fair, I just wanted to not beat up my body, so the deal was, I get to travel on Singapore Air in one of their first-class cabins. I have heard it is the best experience one can have on a commercial flight. I am quite looking forward to it.

I am not in Singapore long, and so get back on Saturday to New York, where I will stay two nights before taking off for the week to the Naval War College in Newport, Rhode Island, which may be one of the coolest times I spend this year. I will fill you in on the details later.

And then we have David Kotok's Maine fishing trip the first Friday in August. Then home the second week of August for almost 30 days. What a brilliant plan! Travel close to 200,000 miles in one year, and your plan is to be in Texas in August and early September? Texas as in the Furnaces of Hell? Texas in August? Oh well. God did in fact create air conditioning. I will survive.

A quick note about my travels. It seems like I am always on the road. It is an insane schedule –I get that. But each trip in and of itself makes perfect sense. Bluntly, most of them are for money. My speaking fees are high enough that I get excited to get on a plane and go somewhere. And if that excitement wears thin, then we will raise the price until the thrill returns.

Now, next Thursday is a freebie for Lew Spellman. It also gets my great friends in for an evening and Rosie in the night before for some guy time. We don't get enough of that. Austin is a quick trip. I can see George and Meredith Friedman of Stratfor for lunch and into the afternoon, comparing notes on the world. A few more meetings with fun people, then on to the hotel to read, think, and write before dinner – and then we are on. I get a charge out of doing panels with guys like Rosie and Rich. You have to bring your "A" game or you get crushed.

A New Adventure

The problem of late is just so many great opportunities that I don't feel I can say no to, although if I keep ending up in NYC I may need to get some kind of timeshare. I half expect this run could end for any reason at any minute, and I want to enjoy it. I honest to God have to pinch myself sometimes to make sure I'm not dreaming. Some of this seems so surreal, from the perspective of this country boy. Now, I work hard as Hades, but lots of people work hard. I recognize my good fortune and just want to enjoy it while it lasts.

And thank you gentle reader, for making it happen. Without you sticking with me, it would never have turned out this well. I am grateful.

And, we will soon be announcing significant changes to our publishing business. We have created Mauldin Economics, with an in-house team of analysts and editors to bring my readers world-class investment advice, including specific buy and sell recommendations. We have worked a long time to figure out how to do this in a manner that Tiffani and I and our entire, rapidly growing team can be proud of. At the end of the day, it is all about serving you.

Our first new investment product will come your way within two weeks, along with major changes in our website. And there will be more publications and website features in the near future.

But with all the changes, one thing will not change. I will write this letter every week for as long as I can, and it will be free. If you like what you read here, then every now and then take the time to introduce me to a few of your friends. I can always use another best friend like you.

And Bad Dad

But sometimes friends and even Dads really mess up. As many of you know, I have Korean twin girls who we adopted at six months old. They were beyond identical. While their siblings could tell them apart, they were almost 14 before I could be right more than 50% of the time. Honestly, in the early years, I was wrong a lot. That was not good, but by their early teens I got it up to about 90% of the time.

Fast-forward. Two weeks ago I said that I was in Tulsa for the graduation of my daughter. I was late getting there because of my investment conference. When the other twin, Amanda, graduated from the same school a few years ago, it was later in May; so I just assumed there would be no conflict, when we planned our conference. But there was, sadly. And though I left very early the morning after the conference, between late flights and an early start to the ceremony this year, I just simply missed her walking.

But I got there and we all went out. But then I had mentioned in this letter about the trip and graduation and all, and instead of saying "Abigail" I said "Amanda"! It was Abigail's moment and Bad Dad, who finished writing at 6 in the morning, just blew it.

But Abigail, I am proud of you for getting it done and already having several internships in addition to your job. There are some kids I worry about, but you are not one of them. You are a winner and always will be, and any firm that gets you will be lucky.

Like what you’re reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

And the twins both gave me graduation pictures. Standing in the same robe, in front of the same flag. My assistant Mary put them side by side on my office wall. And looking at them, for a second they were four years old again and Dad couldn't tell them apart. But just for a second. I have learned to discern that each of them is slightly prettier than the other one, so that makes it easy to tell them apart now.

Trust me, it's not any harder than figuring out Europe. And certainly not as hard as it will be to get out of bed in a few hours. So enjoy your week, and over the next few months we will look at some deflation trades that might work for you.

Your learning to enjoy the ride analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Tags

Suggested Reading...

|

|

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.