Mamas, Don’t Let Your Babies Grow Up to Be Pension Fund Managers

-

John Mauldin

John Mauldin

- |

- February 15, 2015

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinMamas, Don’t Let Your Babies Grow Up to Be Pension Fund Managers

Expected Returns, Realistic Expectations

Dude, Where’s My $4 Trillion?

Where Can You Find Yield?

A High-Order Problem

Dallas, Florida, Switzerland, and New York

We do not have to look to Greece to find massively underfunded obligations. Here in the US we can find hundreds of examples, willingly created by politicians and businessmen who proclaim they are working for the public good. We call them pension funds, but they’re just another form of unfunded debt. A sovereign bond is a promise to pay a certain amount of money over time. A defined-benefit pension fund is a promise to pay a certain amount of income over time. The value of either is determined by the ability of the government or the pension fund (or its sponsor) to pay.

I am in the Cayman Islands as I write this letter, to speak at an alternative investment conference attended by the management of some of the largest pension funds in the US and Europe, both public and private. Being here has motivated me to write this week’s letter on the problems that pension funds face. The pension fund managers I have talked with take their fiduciary obligations seriously, and they face some serious challenges.

I was on the stage with Nouriel Roubini (who makes me come off as the optimist), and we were talking about macroeconomic risks. I was asked what other sorts of risks people should be thinking about, and I cited a recent report about how pension fund obligations had dramatically increased because of a small change in mortality tables. There has been a very steady increase in life expectancy over the last almost 100 years. It is a fairly well-defined trend. The actuarial accountants whose responsibility it is to track these things updated the life expectancy tables for a 65-year-old male, who can now expect to live an additional 21.6 years, two years longer than in the old table. I pointed out that this trend toward longevity is very well established and is likely to accelerate as new technologies and medicines become available, which means that underfunded pension plans are even more underfunded than we think.

I pointed out that while living longer is a very high-quality personal problem to deal with, if your pension plan doesn’t live as long as you do, that could be an issue. Some pension plan managers approached me afterwards to talk about this issue, and it is apparent that others are confronting it head on. Matt Botein, global co-head and CIO, BlackRock Alternative Investors, later talked about how he helped pension funds to hedge their “mortality risk” (the odds that pensioners will live longer) by buying a large life insurance company. The value and profits of a life insurance company will rise if the people they have insured live longer. That is a very creative way to deal with the exposure that pension funds have to the obligations imposed by longer lifespans.

Mamas, Don’t Let Your Babies Grow Up to Be Pension Fund Managers

Today we briefly look at four very large problems facing pension funds. With a nod to Willie Nelson, I’m not sure I want my babies to grow up to be pension fund managers. It’s going to be a very challenging occupation, given all the headwinds they face. Not that the ones I know don’t seem relatively happy and well-adjusted, but they do face a Sisyphean task.

Expected Returns, Realistic Expectations

Most public and private pension funds project returns of between 7½ and 8% on their investment portfolios. Let’s analyze how realistic that is.

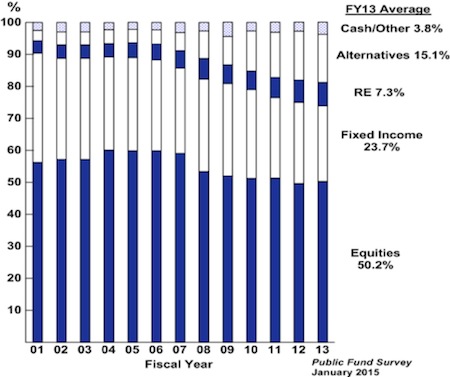

First, if you look back over the last six years, pension funds actually returned 6.8%. Not bad until you consider that we’ve been in a roaring bull market for the entirety of those six years. The average return for the largest public pension funds in the US in the recent decade was closer to 3.2%. Pension fund returns are highly correlated to stock market indexes, which is not surprising when you look at the typical allocation pattern of pension funds. This survey is from publicfundsurvey.org.

Note that hedge funds have recently underperformed equities; but on average they do somewhat better over the long term, depending, of course, upon which funds you are in. Accounting for the equity-like returns that many hedge funds achieve and the fixed-income returns that many real estate portfolios yield, the typical public pension fund portfolio looks like 55 to 60% equities, 30% fixed-income, and 10 to 15% alternatives.

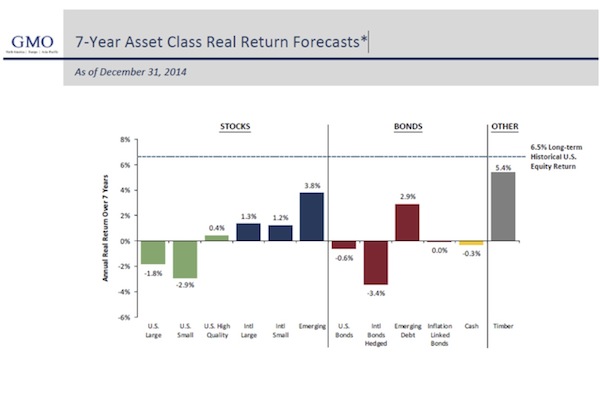

As every prospectus states, and as I remind readers all the time, past performance is not indicative of future results. Jeremy Grantham at GMO has given us a forecast for seven-year real returns of various asset classes. This chart is as of December 31, 2014. Note that the long-term real return for US equities has been 6.5% (for newbies, when we say “real” return we mean net adjusted for inflation. Got it?)

Such forecasts are made in various ways but are generally based on how a particular asset class performed at a given level of valuation. It is well understood that if stocks at the beginning of a period have a lower valuation (there are several different ways to measure valuation, but generally we think of the price-to-earnings ratio), then their longer-term returns are going to be higher, often significantly higher, than the returns when equity valuations are high at the beginning of a period. Equity valuations are generally in the high range today (though not in historical nosebleed range – there is room for them to go higher).

Thus GMO’s forecasts are not very optimistic in terms of equity returns. And neither do they expect much from bonds.

This does not bode well for pension funds, which are heavily weighted to US equities. Given that the 10-year US Treasury is yielding under 2% and that some of us feel it may approach 1% before the end of the decade, the probability that any fund will be able to obtain 7-8% total returns over the next seven years doesn’t seem very high. Even hoping to get 4% might be stretching it.

Like what you’re reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

If this all sounds pessimistic, I suggest you go to www.CrestmontResearch.com and look at historical returns on the equity and bond markets for the last 100 years. There were periods when US equity returns were negative for 20 years.

Further, it has been almost seven years since the last recession. Given that the longest we’ve gone without a recession is close to 10 years, it seems likely that we will see a recession within the next five years. The average stock market correction in a recession is in the 40% range, and recessions almost always mean that interest rates go even lower, which makes the challenge of achieving even 4% over the next seven years even more daunting.

The difference between compounding at 4% and 8% is huge. You can go to various websites that will help you calculate compound interest rates on your assets over time. I went to money-rates.com. The difference between compounding at 4% and 8% for 10 years is impressive: $1,000 grows to $1,480 at 4% and to $2,159 at 8%.

$1000 grows to $2,191 at 4% in 20 years and to $4,661 at 8%. At 4% you barely double your money in 20 years, but at 8% you double and then more than double again.

Okay, we all know the power of compounding. And it stands to reason that if a pension fund compounds at half the rate they expect to, they’ll have a problem in the future. But it’s actually worse than that, because some pension funds are not adequately funded today. Obviously, if a pension fund doesn’t have the money in its fund that it should have, then that money is not available to compound.

As it turns out, the largest portion of future assets from which pension funds will be able to pay out future benefits comes from the magic of compounding. If a government or company fails to fund its pension plan today, then either more money will have to be provided in the future, or there will be fewer benefits.

Pension funds, and especially public pension funds, are massively underfunded. How much is a matter for debate, but it’s a debate we should briefly look at. Since the level of future assets depends on the rate at which the portfolio will increase, a pension fund’s projection of that potential growth will determine whether the fund is overfunded or underfunded today. That projected growth rate is called the cap rate.

Even assuming the 7-8% returns that most pension funds use to calculate the contributions required to fund promised benefits, the funding shortfall is still in the high hundreds of billions of dollars nationwide. But what if you assume a cap rate similar to the return on the 15-year bond? That return was about 3.25% a couple of years ago when a group called State Budget Solutions did a study on the underfunding of public pensions. Using that 3.25% cap rate, they estimate that public pension funds are underfunded to the tune of $4.1 trillion. I should point out that their study included just 250 state-level defined-benefit plans and omitted many smaller county and municipal plans, so the shortfall across all plans is in all likelihood much worse.

I should note that you can find other studies that will say the underfunding is “only” $890 billion or $1.5 trillion or – pick a number. But I have not found one study that says there is not an underfunding problem.

You can click on the link above to see how your state is doing, but let’s pick on California. Back in 2013 their state pension plans had $459 billion in assets and a projected liability of $1.1 trillion (at the lower, 3.25% cap rate), for a funding shortfall of $640 billion.

The State of California itself assumes a higher cap rate, but even then the state admits it will need to inject $5 billion a year annually into the state’s second-largest pension fund, the California State Teachers’ Retirement System, or CalSTRS. For complex statutory reasons, CalSTRS is dependent on the legislature to backfill any losses, while CalPERS (California’s largest fund) can simply raise its contribution rates for participating cities.

Let’s look at the situation as described by Steven Greenhut in an article called “California Faces Death by Pension”:

It became clear that CalSTRS would go belly up in thirty years if the legislature didn’t start sending another $5 billion or so its way annually. So [Governor Jerry] Brown and company concocted another plan to ratchet up state contributions. But it, too, was largely phony. Under the plan, the state sends a pittance extra each year to CalSTRS, with the really large bumps in contributions pledged to take place years from now when it will be someone else’s problem.

This offers a teaching moment. The annual $5 billion (which the state is apparently not actually funding) would get the pension plan back into compliance, but only if you accept the validity of CalSTRS’ assumed return of 7½%. If you take the far more conservative (and maybe too conservative) estimate of State Budget Solutions, California would need to invest roughly $30 billion annually. That would obviously eat up a huge chunk of the $100 billion state budget and is politically impossible.

That leaves the poor pension fund manager with a political dilemma. If he lowers his projected rate of returns, then the people (teachers, firemen etc.) covered by the plan will have to make higher annual contributions. Given how tight budgets are, no politician or union leader wants to be forced to allocate more money to current pension funding, no matter how wise it might be to do so. It would mean cutting somebody else’s budget or raising taxes, and neither are easy tasks.

Yet setting a higher goal for returns almost forces pension fund managers to move out the risk curve in the search for yield. But pension funds are supposed to be conservative money. Balancing that mandate is not easy.

Like what you’re reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

And that brings up a third challenge that pension fund managers face: yields all across the board, almost everywhere in the world, are down because of monetary policy. It is not just yields on corporate bonds that are down. Returns from private equity are also down, as more money chases fewer deals. The prices for the better-rated opportunities rise because of the lower interest rates. And deals get done that shouldn’t because money is almost free.

This is the inverse problem of the cap-rate issue. Because interest rates are so low, the same dollar amount of leverage provides a larger potential return. And the larger potential return increases the price, bringing returns back to whatever is normal for the time. And in today’s environment, returns are low.

I talk with hedge fund managers and fixed-income managers all the time. If you are willing to take a nontraditional approach to fixed-income investing, you can find yields in the high single digits and even the low double digits. But the emphasis here is on “nontraditional.” And there are certainly not enough deals to go around for all of the tens of trillions of dollars of investment funds around the world that are looking for such deals.

A pension fund manager has to deal with his board of trustees. That’s something they constantly talk about: “the governance issue.” Some boards have very sophisticated members, and others, well, not so much. In fact, my experience with boards of trustees is not very heartening. What often happens is that they look for advice from outside consultants. These consultants come in and tell them how much return they can expect to get and give them “political cover” for making decisions, when the suggested decision is pretty much the same old same old. Which is why pension fund returns tend not to vary that much across the spectrum of funds.

(Please note there are some very real exceptions to that generalized statement I just made. There are some boards composed of such experienced investors that I would feel uncomfortable sitting at the same table. Why would they need my advice?)

So in addition to the problems of potentially lower market returns, a pension fund manager may have to deal with an inexperienced board that looks to consultants to tell it what to do and looks over the shoulder of the pension fund manager, keeping him from taking advantage of his experience. But the board of trustees needs to make sure it has some way to protect itself from liability if things don’t work out as planned. And being able to point the finger at consultants and outside counsel is one way to mitigate risk exposure.

And then there is the problem that I mentioned at the beginning of the letter: people are living longer, which means pensions are even more seriously underfunded. But that is a very high-order problem. I don’t think my generation is going to volunteer to die “on time” just to make pension managers happy. The Society of Actuaries started with actual data from numerous pension plans and looked at 220,000 deaths from 2000 until 2009 (involving 10½ million life-years). What they found out was that during that period people were living two years longer than they had been in the past. This corresponds to the roughly one year of increased life expectancy for every passing four years of the last century.

This has real-world implications. As Bloomberg Business reports:

If retirees on average live three years longer than expected – a typical margin of error in the past – a global pension bill estimated at up to $25 trillion could swell by $3 trillion, according to a 2013 report by the Bank for International Settlements’ Joint Forum, a global body of insurance, banking and securities regulators….

The typical corporate pension plan already is underfunded. In aggregate, plans maintained by the 411 companies in the Fortune 1000 that sponsor defined-benefit plans – where retirees receive a guaranteed payout depending upon years of service – are 80 percent funded, according to Towers Watson. [I note that this is a much higher funding level than public pension plans achieve, but it can be a drain on profits for corporations.]

That extra $3 trillion that will have to be found because people are living longer? In another eight years it will be additional $3 trillion, as actuaries are surprised to find that people keep insisting on living longer. And inflation and underfunding problems will make the number still larger.

There are those who argue that longevity is not going to continue to increase as it has over the last century, because we have found all the “low-hanging fruit.” Basic hygiene, antibiotics, modern medicine, and so on have taken us about as far as we are going to go, they say.

And while I would agree that we have harvested the low-hanging fruit, I think the biotech revolution is creating fruit ladders that will let us reach far higher.

The baby boomer generation is going to be the first generation in the last 150 years that will break the deal that is implicitly made with previous generations. Each generation heretofore has agreed of die in an actuarially definable period of time. That way pensions get funded and wealth is transferred on.

I think there is every likelihood that it won’t happen this time. The boomer generation is going to live far longer and use more resources in doing so than any previous generation has done.

Patrick Cox, my colleague over at Transformational Technologies, has been documenting the rapid evolution of age-extending medicines and therapies for some time now. He and I are both taking some rather new nutraceuticals that seem to be having positive effects. While I can’t say for sure whether it is any one of them or a combination of several that is improving my physical well-being, something has me feeling better than I have in a very long time. Perhaps it is just a different trainer who pushes me more than anyone in the past 40 years has (though I don’t think so), but I am setting lifetime highs in bench presses and other measures of strength. Both Pat and I are in our 60s (I’m 65), and we are both experiencing these lifetime highs in our physical activity. People don’t typically expect to do that in their 60s.

Like what you’re reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

There are technologies and therapies that are just around the corner that, I promise you, I will be close to the front of the line to participate in. And a bit further down the road, but no more than 10 years out, we’re going to see cures for most major diseases. That seems a radical statement, I know, but I’m talking to the doctors and scientists who are doing it.

Healthcare as we know it is changing. I talked to two healthcare executives here in the Cayman Islands. A doctor from India has built a very modern hospital here in Cayman that is doing open-heart surgery for a flat $22,000 per surgery (25% of US costs), inclusive of any complications that you might have. That is an all-in price. Their hospital infection rate, a big problem in the US, is a small fraction of what we see in the US. Their success rate is higher. They are simply using different procedures and controls than we find in the US. The doctors are actually far more skilled than most, as together they do dozens more surgeries per week than similar groups of US doctors do. And they are doing this across multiple disciplines, like orthopedic surgery, cancer treatment, etc. Their vision is to drive the cost of healthcare down and improve outcomes in doing so. As costs come down, more of us will be able to afford access to healthcare and thus extend our lives.

My doctor, Mike Roizen of the Cleveland Clinic, points to a study they did that estimates the US could save 20% of its healthcare costs if the American people just changed the way they behave. One of the primary reasons Europeans spend less on healthcare than Americans is that we’re just not as healthy. We eat a lot of bad food, smoke, don’t exercise, and even worse, don’t take prescribed medicines. Thirty percent of Americans are now defined as obese. The correlation between obesity and health is well known.

In less than 10 years therapies will exist to bring that obesity epidemic under control, which will extend both lifespans and healthspans. There are multiple paths that Patrick and I are watching today for the development of such therapies. It is a very interesting race to watch, and if you pick the right horse it could be very profitable.

Let me make a suggestion. You should go to http://www.mauldineconomics.com/tech and subscribe to Patrick’s free weekly letter, where he talks about a lot of the new advances being made in biotech and medicine each week. Whether or not you ever intend to subscribe to his investment letter, you should be aware of the breakthrough developments that are happening today. In his latest issue he talks in detail about the nutraceuticals that he and I are taking, so you and your healthcare team have a starting point for deciding whether you should consider taking them, too. We are not in the pill business, but I would really like my subscribers to live longer with me. We are not interested just in helping you have a longer life, but also in helping you have a healthier life, too.

Healthspans are more important than lifespans. I am watching my mother come to the end of her life. She was active up until a few years ago but has now become bedridden at 97; and frankly, it is not a very pleasant prospect that in 30 years’ time that person in the bed could be me unless there are some major advances in healthcare.

After that little walk down the rabbit trail, let’s come back to the original point. People who are counting on their pension funds for retirement are going to live longer than pension fund managers have been expecting them to. This reality is going to make it even more difficult to ensure that everybody has enough money to get them through to the end of their longer lives.

If you don’t have a pension but are going to have to live off your savings, then it is very important that you understand that you need add five to ten years – at least – to whatever you think your life expectancy is today. We need to rethink retirement and rethink Social Security. Because, yes, the additional costs for Social Security, the largest pension fund in the US, are going to be staggering.

For a start, we need to be aggressively increasing the retirement age for Social Security. When Social Security was introduced during the presidency of Franklin Roosevelt, the age at which you could claim benefits was 65. But the average lifespan for a male at that time was around 57. If lifespans and eligibility for Social Security had moved in lockstep, today eligibility for Social Security would be somewhere in the upper 80s. And while no one would suggest that should be the case, it does help frame the question of what the eligibility age for Social Security should be.

Dallas, Florida, Switzerland, and New York

I want to thank my hosts at the Cayman Alternative Investment Summit. They really went out of the way to make sure we had a good time and to make us feel special. And I actually did get a few hours here and there at the beach and in the gym. The Ritz Carlton resort here is very nice.

I am back in Dallas and will speak this Thursday at an open forum for financial advisors sponsored by S&P and called “Managing Risk and the Future of Factor-Based Strategies.” If you are an investment professional, you can register at this link.

At the beginning of March, I will be in Orlando to do a keynote presentation for the American Banking Association and to share a dinner with my old friend Greg Weldon. A few weeks later I fly to Geneva and Zürich, where I have a very packed schedule. In addition to speaking, I’m particularly looking forward to being with Dylan Grice, plus lots of other friends, and meeting Bill White for the first time. I’m sure I will be staggered by the cost of everything in Switzerland, but the train ride from Geneva to Zürich is worth every penny. On a side note, Bill White was smart enough to negotiate his speaking fee in Swiss francs, while I’m getting dollars for mine. That probably tells you all you need to know about whose advice you should listen to.

I have some other speeches in Dallas and will then head to New York at the end of March.

I’m finishing the letter while still in Cayman, and I think it’s time to hit the send button, because the beach is calling. And while I don’t sit in the direct sun very long, there are plenty of umbrellas under which to hang out with my iPad and finish a book or two. I will probably be a bit more casual than Al Pacino. The conference arranged for him speak on Thursday, and Friday morning he was out by the pool lying in a lounge chair, wearing his standard black long-sleeved shirt and pants. I’m thinking my swimsuit and an old T-shirt might be more appropriate. Hu-wa. You have a great week!

Your not even thinking of retiring analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Tags

Suggested Reading...

|

|

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.