Year of the Bookends

-

John Mauldin

John Mauldin

- |

- January 14, 2022

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinIf you are a booklover like me, you probably have many shelves. On some of those shelves you probably have bookends holding the books in place. They come in opposing pairs—similar but reversed.

What if the COVID-era economy has bookends?

I think that may be what’s happening. If you think of 2020 as the left bookend, at some point we’ll have a period when equally significant economic forces push the other direction. The time in between? A bunch of books telling this crazy era’s many different stories. Maybe someday we’ll read them all.

Today I’ll continue the annual forecast I began last week. New COVID developments are unfolding rapidly. If we’re lucky, they may carve out a nice bookend for us. But my worry is that rather than bookends it could be economicus interruptus. 2019 was not portending the most robust of economies. What if, in Groundhog Day fashion, we end up back where we were?

And as much as I like my bookends analogy, maybe the COVID period is more like brackets: 2018, 2019, [2020, 2021] 2022, … A break in the normal where extraordinary measures were applied and are now being removed. Let’s explore the implications.

Labor Shortage x 2

Of course, any analogy is flawed. We had a clear beginning of the Covid era but the ending is going to be cloudy at best. But we’re at least closer to the end.

A couple of weeks ago I saw someone on Twitter predict that by March, every American would be either triple-vaccinated, or have been an Omicron case, or possibly both. My research and my high-level healthcare contacts suggest that looks like a better guess with every passing day. Having circled the globe in barely a month, this variant is arguably the fastest-spreading virus in human history, replacing measles.

The good news is that most Omicron cases have fairly mild symptoms. Many people feel nothing at all, and for others the mRNA vaccines usually reduce it to a short, flu-like illness. Previous infection with other COVID-19 variants seems to offer some protection as well. It can still be very dangerous in those with no defenses or comorbidities and older. (I am glad to be vaccinated as well as boosted, and I urge everyone to get their shots. Yes, I know all the anti-vax arguments but I also understand odds. I’ll take my multiple-thousand-to-one risk and go home.)

Back to the main business point, the prime economic problem is a large number of people having simultaneous minor but highly contagious illness. Many can’t go to work, even if they feel fine, until they get a negative test. Simply getting the test can be difficult. Back in 2020 we were (correctly) concerned this virus would kill many people. Fast forward two years and we’re still concerned about the virus, but now because it is an inconvenience instead of a deadly threat. (Though, as noted, it still can be deadly.)

The inconvenience adds up to an economic problem. We already have a severe worker shortage hobbling the recovery. Omicron is making the shortage worse even though most people will only miss a few days of work. The numbers are stark, too.

In February 2020 the US civilian labor force was 164.6 million. In December 2021 it was 162.3 million (and had been much lower). So the loss of “only” 2.3 million available workers has been a big deal.

Enter Omicron. My associate Patrick Watson estimated the numbers last week. If we conservatively assume 20 million Americans will get Omicron in January/February, and 60% of those are employed, and each misses five days of work on average, it adds up to 60 million lost work-days. That’s like losing almost 3 million workers for a month, roughly 2% of an already smaller labor force.

In other words, Omicron will, for a short time in little bits and pieces, more than double our labor shortage. It may have an extended effect, too, if some of those people develop “long COVID” disabilities. But just the immediate problem is bad enough.

GDP is, at the most basic level, the number of workers times their output per hour worked. Reducing the first part of that equation for a couple of months will certainly affect quarterly GDP, even if all those workers quickly return.

Economists are starting to slash their growth estimates. Mark Zandi of Moody’s now expects 2.2% annualized Q1 growth, down from his previous 5.2%, mainly due to Omicron’s impact. Others are doing the same or will soon.

Now, that’s just for the quarter. We’ll certainly make up some of the lost output after Omicron blows through, kind of like we made up the 2020 downturn in 2021. That doesn’t mean it will have been costless. Nor is there any certainty we will avoid another variant the rest of the year.

Like what you’re reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

But good things are happening, too. New treatments (including some older, well-tested drugs that seem to help COVID symptoms) combined with Omicron generating additional immunity in the population may reduce COVID-19 to a manageable nuisance by mid-year. Like a normal flu season, which is back, by the way. That would be a nice bookend for this pandemic.

Unfortunately, our library has another shelf, with another set of bookends.

Policy Shift

When COVID hit the US, the Federal Reserve responded by firing liquidity in all directions to protect the financial system. Given what was known and feared at the time, I think the Fed’s initial moves were appropriate. Continuing them for almost two more years was not. They should have ended QE a year ago. It had significant side effects for little clear benefit, except to the value of assets held by those with investable assets, clearly not the majority of the population.

The Fed is finally starting to wind down this extraordinary activity. This gives us another pair of bookends. Launching these programs was a shock and ending them will be another shock, with different particulars but no less shocking.

It’s easy to forget how disorienting that launch period was. You can go back and look at the near-daily stream of Fed news releases as it announced new programs in March/April 2020. No one outside the Fed (and maybe inside it) knew what was coming next. Reversing that whole process is not likely to be a simple, quick, straightforward process. The closest analogue we have was the 2017–2018 attempt to taper off previous QE rounds. That did not go well.

To get policy back where it should be, the Fed has to do three things, either in succession or concurrently:

-

Stop buying more Treasury and mortgage bonds;

-

Allow the bonds it already owns to mature without replacing them;

-

Raise policy rates (Federal Funds) at least back to “neutral.”

There’s actually quite a bit more but these are the big ones. The current plan, at least as revealed publicly, is to reduce the bond purchases to zero by spring and then start raising rates. Some officials have talked about actually reducing the balance sheet soon but as yet there’s no schedule for that. The plans they’ve revealed are all subject to change, and indeed did change just last month. They could easily change again.

The next three scheduled FOMC meetings are January 25–26, March 15–16, and May 3–4. Each is a chance for Fed officials to change their minds, which we know they can do quickly. But we also know they don’t like surprising the markets. They will likely signal any changes in speeches and media interviews.

They could get cold feet. Even without Omicron, some may see the unexpectedly weak December jobs and retail sales data as signs the recovery is faltering. The Omicron impact will be clearer by the late January FOMC meeting, and certainly by March as more data comes in. My best guess is they will stay on course unless the inflation numbers weaken dramatically in the next two months, which I highly doubt.

Could it happen? Omicron labor shortages, while temporary, will hit both supply and demand. Production will fall as workers are out sick, and the sick workers (plus their families) will reduce or at least change their spending.

In some respects it may be like 2020, but with a twist. Back then, a combination of virus fear and government-ordered restrictions suppressed economic activity. This time around we don’t have the same fear level—nor should we, at least in the US. We have vaccines and well-tested treatments that didn’t exist then. We also don’t have widespread lockdowns. Some things are closing but not because they were ordered to. It’s because they don’t have enough workers to operate normally. For instance, Alaska Airlines canceled 10% of their flights simply due to not enough workers. I could spend an entire letter citing similar circumstances. The economic effect is similar to 2020.

Even if, as seems likely, Omicron peaks soon and we emerge from winter with a much better COVID situation, the Fed has a giant complication. They’re in the middle of a policy shift that was already at high risk of error. Now the FOMC members have to consider Omicron’s economic effects, which could linger for some time after the virus itself fades. This greatly increases the odds something will go wrong at some point in the process.

So COVID monetary policy will go out like it came in: with a flurry of uncertainty and confusion. Not the kind of bookend anyone wants on their shelf, but it’s probably what we’ll get.

Transition Year

Like what you’re reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

For the 10 years preceding 2020, US real GDP growth averaged about 2.2%. The best year in that period was also the first one, 2010, when the economy grew by 2.79%. The worst year was the following one, 2011, with 1.57% growth. The next eight years were all between those two extremes.

But note, the extremes weren’t very extreme. Growth stayed in a fairly tight 1.22 percentage point range for a full decade. It was followed by two years with GDP well below that zone (-2.26% in 2020) and above it (4.9% in 2021 through Q3).

I said pre-COVID I thought growth would average 2% in the 2020s, and later lowered that to ~1%+. The first two years of this decade average to 1.32%. I know, it’s only two years, and two unusual ones at that. But so far, not too far off.

If (knocking on wood) 2022 sees us get the virus back under control and the Fed manages to normalize policy without sparking another crisis (both far from certain), we face another important question. Will the forces that kept the economy rangebound before this terrible two years reassert themselves, putting growth back in the old range? Or will the changes COVID wrought bring a new era, either better or worse?

There’s no question much will be different. Under pressure to survive, businesses have learned new ways to operate. Consumer preferences have changed. Far-flung, just-in-time supply chains failed, affecting inventory levels. We all have a new awareness of risks to our health. These could all be positive or negative, depending on how they develop.

An Actual Honest-to-God Forecast

Making forecasts about the future is silly. You normally wind up with mud on you face, a big disgrace… But my economicus interruptus comment makes me throw caution to the wind.

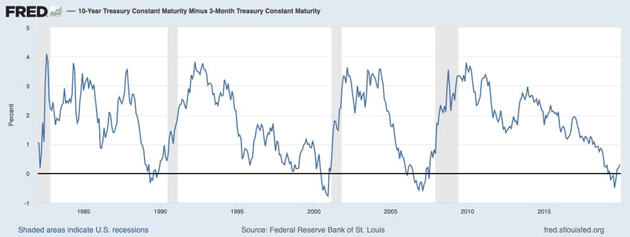

Rewind the tape to 2019. The economy was clearly slowing down. We even had the dreaded inverted yield curve.

Source: FRED

Inverted yield curves don’t cause recessions. They’re more like a fever telling you something is wrong. They typically precede recessions by 12–18 months. COVID interrupted that cycle with a recession unrelated to prior economic problems.

At some point later this year we should resume what will be—and I hate to use this phrase because it is so trite—a post-COVID, post-snarled supply chain, new normal. We’ll face many of the same issues we had in 2019 plus a whole host of new ones. Some will be positive, some negative. For example, bringing back certain critical parts of the supply chain will be long-term positive for the economy, but also inflationary as it will increase prices. And it will take time.

Many employees now want to work from home. That means they will have lower commuting costs, etc., and their companies won’t need as much office space. It also means that where you live may no longer need to be near where you work. That means disruption.

Further, repeating what I have said for months, Congress under Trump threw trillions of dollars in stimulus money to help maintain the economy in 2020, then another $1.9 trillion in early 2021 which while possibly useful also ignited inflation and exacerbated supply chain issues. Now we have removed that stimulus from the economy, which has to stand on its own. We are back to late 2019.

Further, the Federal Reserve is (finally!) moving to eliminate QE and theoretically will raise rates after that. I don’t want to get complicated here, but these two actions combined will further slow the velocity of money. Combined with the massive US debt, it is a recipe for economic slowdown.

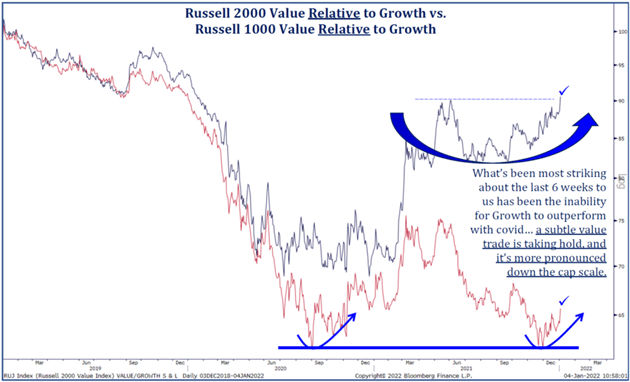

Will markets shrug off the removal of QE? If they do, it’s smooth sailing. But seeing how valuations are stretched and there appears to be a rotation into value stocks…

Source: David Bahnsen

…AND insider buying has fallen to a recent low and the ratio of insider sellers risen to a recent all-time high, it calls the smooth sailing hypothesis into question.

Look at this witch’s brew: a slowing economy due to Omicron, the Fed tightening which in the past has always been a problem for the markets, no fiscal stimulus cavalry to the rescue, inflation at 40-year highs.

Analysts that I greatly respect believe Jerome Powell will elect to “stabilize” the financial markets rather than fight inflation if there is a true bear market, which the data suggests is a real possibility.

Like what you’re reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

This is where I go out on a limb. I think there is a reasonable probability that Jerome Powell will look at history and not want to be seen as Fed chairs Burns or Miller. He has an opportunity to drive a stake in the heart of inflation while risking only a mild recession. If he kills inflation, he can then provide stimulus which will bring the markets back. All will be right with the world, from Wall Street’s perspective.

If Powell doesn’t kill inflation, he will go down as possibly the worst Fed chair in history, which is saying something. I think he’s made of sterner stuff. He doesn’t need the money being an ex-Fed chair. He is thankfully not an East Coast-trained economist. He is a businessman who recognizes the insidious nature of inflation.

The markets are projecting three rate increases this year. Let’s call that over/under line. Nobody would be really surprised if they only do two rate hikes because the economy is soft. The major surprise would be if they do four rate hikes, pounding that stake into the heart of inflation.

Note that many regional Fed presidents are also taking a harder inflation line, at least rhetorically, then they were a few months ago. Maybe they got religion in December.

So, a forecast? I think there is a 70–80% chance of a real bear market and a better than even chance of what I hope will be only a mild recession.

That is actually the good news. I am a long-term cheerleader of technology and the general rise of humanity. A bear market/mild recession would give us the buying opportunity of the decade. It would reset all of the recent excesses and let us move forward for the next few years relatively confident.

We will still have a hangover of massive federal debt, which will be a drag on growth. We are not going back to long-term 3% GDP growth. But we will be in an era where we can actually make investment decisions based on old-school valuations and projections on disruptive technologies. Investing in bonds will still be a chump’s game, so private credit and growing dividends will be where you want to focus your fixed income strategies. And we could be setting up for a once-in-a-generation high-yield investment opportunity. Getting in at the bottom is so damn much fun.

How Then Should We Invest?

I have written an update to my thoughts on The Great Reset (my version, not the Davos one). The closer we get, the more clarity we get, though I must admit we are looking through a glass darkly. It is the future after all. Nonetheless, we can begin to think about portfolios that will get us from where we are today to the other side of The Great Reset with as much buying power as possible. That looks like numerous trading strategies, lots of private credit, and very selected private technology companies (my personal biggest positions) that will be massively disruptive. And at some point, we are going to want to go all in on public technology companies with the right managers.

All of that and more is available via my friends at CMG who host the “Mauldin Kitchen.” (I also serve as their chief economist and co-portfolio manager, and am a registered investment advisor.) You can pick and choose off the menu or take the whole kitchen. You can get my update on The Great Reset and see what’s in the Mauldin Kitchen (I and my team are really able to source a few good ideas here and there) by clicking here. Your long-term investment portfolio will thank you for exploring the Mauldin Kitchen.

Washington, DC?

It seems there will be a snowstorm in Washington this weekend, making the board meeting I was going to attend somewhat questionable. I will know sometime later today. That’s my only scheduled travel. By past standards it seems rather pathetic, but I’m content to be stuck here in paradise with Shane.

My stock answer when people ask me how my kids are doing is, “five out of seven are doing great, it’s just never the same five at the same time.” With Shane I now have eight. Amanda is recovering nicely from her stroke. I’m so proud of her. She sent me pictures of her physical therapy that makes me tired just looking at them. Chad had hernia surgery and will soon be back to work. I don’t want to jinx anything, but someone asking how my kids are doing now? I would have to say all eight are on a good path and in a good place. I live in paradise. It’s a good time to be alive.

And with that I will hit the send button. Shane and I have started watching Yellowstone in the evenings due to the encouragement of many friends and reviews. So far, it is living up to the hype. Have a great week and if you haven’t already, go back and get that link to my update on The Great Reset and see what’s in our kitchen. All my best for 2022!

Your relatively optimistic about 2023 analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Tags

Suggested Reading...

|

|

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.