You Have to Unlearn This Thing to be a Good Investor

- Jared Dillian

- |

- April 12, 2016

- |

- Comments

BY JARED DILLIAN

I have a very good friend who is a real estate agent (prior to that, he was a public school teacher in a very impoverished area). When he became a real estate agent, he needed to choose a mentor who would guide him through his first five transactions.

Early on, my friend would often complain about his mentor. He didn’t have his act together, he was often late, he wasn’t that smart, etc.

Finally I asked him: “If this guy is such a loser, why did you pick him as your mentor?”

He said, “I felt sorry for him.”

That was when I sat him down. “This is the business world. You don’t pick the worst guy, you pick the best guy. Got it?”

Ever been to a pro tennis match? The crowd typically goes with whoever is losing. Or look at the UConn women’s basketball team. They are so dominant that they have generated a huge backlash.

And outside of sports, we’re always rooting for “the little guy,” “Main Street,” the disenfranchised, the underprivileged.

Screw the moral superiority of the underdog.

In the public sphere, you divert resources where there is need. The more need, the more resources. In the private sphere, you invest—in people, places, things. You allocate resources to things that are good. If somebody is winning, you bet on them to win more.

This is true for people, and it is true for departments and divisions, and it is true for entire companies, even countries.

Why is the underdog, the underdog? Why do we never carefully examine the actions of the underdog or assign any responsibility for his behavior? Can you imagine what the financial markets would be like if we tried to invest in the worst companies, instead of the best?

People Are Mentally Ill

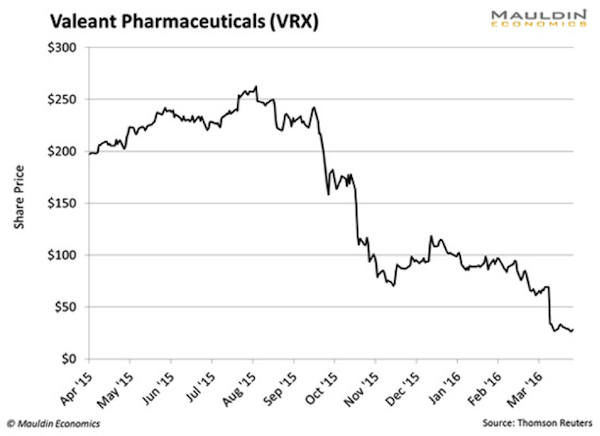

So why is it that whenever people see a chart like this…

…they feel compelled to try and pick a bottom?

It’s betting on the underdog.

Valeant Pharmaceuticals is a loser company. It has a track record of losing.

Do you want to know why stocks trend? There are a lot of great reasons why it is difficult for trends to reverse.

A successful company runs into trouble, demand for its products falls, this news hits the media and causes people to sell their stock, which causes analysts to ask questions about what is really going on and publish negative reports, which causes more selling.

Pretty soon the rating agencies get involved and downgrade the debt, which causes forced selling, and so on.

It is a self-reinforcing process. It is also a self-reinforcing process on the way up.

You don’t bet on the worst company. You bet on the best company.

You buy the chart that is going from the lower left to the upper right. You root for the Yankees. You root for them to win over and over and over again… and keep winning in an orgy of winning.

Turnarounds are rare—like, very rare

This is the most important thing I have learned in all my years in capital markets.

When a company is going bad, it seldom gets better. And when I say rare, I mean extremely rare. That dog in your portfolio is very likely going to remain a dog. Or get worse.

It is different when you are talking about commodities, or countries, or commodity-related stocks. Turnarounds in commodities are more frequent because low prices stimulate demand and high prices stimulate supply.

Also, in countries where things get really bad, people will get fed up and vote the bastards out, provided the political process still works. We are seeing this in Brazil and South Africa. It already happened in Argentina.

But when you talk about corporates, the idea that you can bring in some rock star CEO to turn it around… almost never happens.

A Universal Takeaway

The moral superiority of the underdog is deeply ingrained in our culture. So ingrained that we have to unlearn everything we have learned in order to be good investors.

The guy that’s winning usually keeps winning. The guy that’s losing usually keeps losing. The serial correlation exists because the winning guy is taking right actions and the losing guy is taking wrong actions and generally will never figure it out.

The way you get the losing guy to figure it out is to cut off the flow of money. Works for companies. Works for people, too.

Subscribe to Jared’s insights into behavioral economics

Click here to subscribe to Jared’s free weekly newsletter, The 10th Man, so you won’t fall prey to the herd mentality that so often causes mainstream investors to make the wrong decision.