Europe’s Pension Funds Are Running Low as Boomers Retire

- John Mauldin

- |

- July 3, 2018

- |

- Comments

BY JOHN MAULDIN

I recently looked at the situation of US public pension funds. Many of them are woefully underfunded and will likely never pay workers the promised benefits—at least without dumping a huge and unwelcome bill on taxpayers.

Non-US readers might have felt a little satisfaction at that. There go those crazy Americans again, spending wildly beyond their means.

You are partly correct; we aren’t exactly the thriftiest people on earth. However, your country may be more like the US than you think.

Let’s look at the pension situation in some of the biggest economic powers in Europe.

The United Kingdom

We’ll start with our closest European ally, the United Kingdom.

The WEF study shows the UK had a $4 trillion retirement savings shortfall as of 2015. It’s projected to rise 4% a year and reach $33 trillion by 2050.

In a country whose total GDP is around $2.6 trillion, the shortfall is already bigger than the entire economy. And with even modest inflation, it will get worse.

And this was calculated before the UK decided to leave the European Union. That major economic realignment could certainly change the outlook.

A 2015 OECD study said developed-country workers could on average expect governmental programs to replace 63% of their working-age income. Not so bad. But in the UK, that figure is only 38%, the lowest of all OECD countries.

This means UK workers must either save more personally or severely cut spending when they retire.

UK retirees have had a kind of safety valve: the ability to retire in EU countries with lower living costs. That option may disappear after Brexit.

A report last year from the International Longevity Centre suggested younger workers in the UK need to save 18% of their annual earnings in order to have an “adequate” retirement income, which it defines as less than today’s retirees enjoy. That’s just fantasy.

No such thing will happen, so the UK is heading toward a retirement implosion that could be at least as chaotic as in the US.

Switzerland

Next on our list is Switzerland.

It is certainly one of my favorite countries. We think it’s the land of fiscal discipline and rugged independence. To some degree it is, but Switzerland has its share of problems, too.

The national pension plan has been running deficits as the population grows older.

Last summer, Swiss voters rejected a pension reform plan that would have strengthened the system by raising the women’s retirement age from 64 to 65 and raising taxes and required worker contributions.

These mild changes still went down in flames as 52.7% of voters said no.

Voters around the globe usually want to have their cake and eat it, too. We demand generous benefits but don’t like the price. The Swiss, despite their reputation, appear not so different. Consider this from the Financial Times.

Alain Berset, interior minister, said the No vote was “not easy to interpret” but was “not so far from a majority” and work would begin soon on revised reform proposals.

Bern had sought to spread the burden of changes to the pension system, said Daniel Kalt, chief economist for UBS in Switzerland. “But it’s difficult to find a compromise to which everyone can say Yes.” The pressure for reform was “not yet high enough,” he argued. “Awareness that something has to be done will now increase.”

That describes most of the world’s attitude. Both politicians and voters ignore the long-term problems they know are coming and think no further ahead than the next election.

Spain

Spain bounced back from recent crises much better than some of its Mediterranean peers like Greece. That’s also true of its national pension plan, which actually had a surplus until recently.

Unfortunately, the government “borrowed” some of that surplus for other purposes and it will soon become a sizable deficit.

Spain has 1.1 million more pensioners than just 10 years ago, and as the Baby Boom generation retires, it will have even more. Unemployment as high as 25% among younger workers doesn’t help, either.

The US is in “better” shape, mainly because we control our own currency and can debase it as necessary to keep the government afloat. US Social Security checks will always clear even if they don’t buy as much.

Spain doesn’t have that advantage if it stays tied to the euro currency. That’s one reason the eurozone could eventually spin apart.

This Is Not a North-South Problem

Worse, some European governments pay retirees more than they made while actually working. It is more than 100% in Croatia, Turkey, and the Netherlands, and above 90% in Italy and Portugal.

I am sorry, but there is simply no way this can continue. These governments have legislated rainbows and unicorns. They will not deliver such benefits, unless it is because wages and benefit payments crash to unimaginably low levels.

Europe has the largest population of pensioners that continues to grow. Looking at Europeans 65 or older who aren’t working, there are 42 for every 100 workers. This will rise to 65 per 100 by 2060, the European Union’s data agency says.

Unlike most European financial stories, this isn’t a north-south problem. Austria and Slovenia face difficult demographic challenges right along with Greece

Across Europe, the birth rate has fallen 40% since the 1960s to around 1.5 children per woman, according to the United Nations. In that time, average life expectancies have risen from around 69 to roughly 80 years.

In Poland, birth rates are even lower, and there the demographic disconnect is compounded by emigration. Taking advantage of the EU’s freedom of movement, many working-age Polish youth leave for other countries in search of higher pay.

Worse Off than the United States

Everything I read about the pay-as-you-go countries in Europe suggests that they are in a far worse position than the United States. Plus, their economies are stagnant, and the tax burden is already near 50% of GDP.

Moreover, many private pensions are in seriously deep kimchee, too. Low and negative interest rates have devastated the ability to grow assets. Combined with public pension liabilities, the total cost of meeting the income and healthcare needs of retirees as a percentage of GDP is going to dramatically increase across Europe.

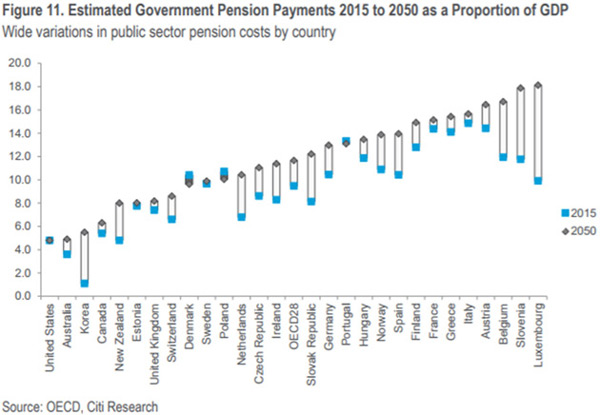

Think about that for a moment. I am not talking about as a percentage of tax revenues. I am talking about as a percentage of GDP that in Belgium will be 18% in about 30 years. Which would be 40–50% of total tax revenues.

That doesn’t leave much for other budgetary items. Greece, Italy, Spain? Not far behind…

Source: Citi GPS

Some research makes the above numbers seem optimistic. Most European economies are already massively in debt and have high tax rates. And those in the eurozone can’t print their own currency.

French President Emmanuel Macron and a few others seem to be laying the foundations for the mutualization of all eurozone debt, which I assume will end up on the ECB balance sheet. However, that still doesn’t deal with the unfunded liabilities. Do they just run up more debt? It seems like the plan is to kick the can down the road a little bit further, which Europe is becoming good at.

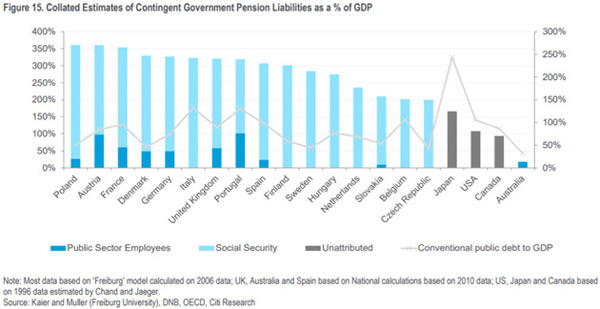

In this next chart, the line going through each of the countries shows their pension debt as a percentage of GDP. Italy is already over 150%. And this is an older chart. A newer chart would just be uglier.

Source: Citi GPS

This problem is far bigger than even the most disciplined, future-focused governments and businesses can easily handle. It is not limited to any one country or continent. The problem exists everywhere, differing only in severity and details.

Join hundreds of thousands of other readers of Thoughts from the Frontline

Sharp macroeconomic analysis, big market calls, and shrewd predictions are all in a week’s work for visionary thinker and acclaimed financial expert John Mauldin. Since 2001, investors have turned to his Thoughts from the Frontline to be informed about what’s really going on in the economy. Join hundreds of thousands of readers, and get it free in your inbox every week.