Hormuz: The $200 Crude Question

Add paragraph text. Click “Edit Text” to update the font, size and more. To change and reuse text themes, go to Site Styles.

The World Isn’t Ending opens mid-conflict, as the US-Israel “military operation” against Iran drags on despite Trump’s repeated promises that it will end “very soon.”

Humans have an evolutionary penchant for focusing on the negative, and our newsfeeds and algorithms feed that. But I am here to say, it is in many ways the best of times, and that controversial lens defines this letter.

My mission here is to describe the world as it is, not as I would wish it to be—and to do so without being boring. I want to challenge you to think differently about the world, using the tools of geopolitical analysis to your advantage. I’m grateful you’re along for the ride.

With that, let’s discuss the war because the simple truth is that nothing happening in the world is as important.

The Situation:

Militarily, Iran is a much weaker country than the US and even Israel. Iran’s top leaders have been assassinated, its air force and navy are decimated, its missile launching capacity is significantly curtailed, and its infrastructure is damaged and vulnerable to further attack. But Iran has not been cowed.

Iran’s Asymmetric Advantage

Now, Iran’s asymmetric strengths assert themselves. The most critical is Iran’s de facto control of the Strait of Hormuz, the world’s preeminent maritime chokepoint through which passes ~20% of the world’s total oil supply and global liquefied natural gas. Most of that oil and LNG go to Asia, but the Strait of Hormuz is also a transit artery for industrial molecules—naphtha, LPG/ethane, methanol, ammonia, urea, sulfur, etc.—that sit upstream of entire value chains for fertilizers, mining, and chemical manufacturing.

This creates a paradox. The short term (i.e., the next 3–6 months) is very uncertain. The medium to long term (i.e., the next 2–5 years) is predictable.

Short-Term Uncertainty

To an analyst sitting in New Orleans, both sides appear to be acting against their own interests. Iran’s rational play is to trade its nuclear program for sanctions relief and reintegration into the global economy. But Iran is run by a thuggish, theocratic bunch of ghouls whose entire philosophy of resistance was just proved by the US attack on its regime. This is an existential conflict for Iran. Absent regime collapse, which at this point seems unlikely, Iran must either secure nuclear weapons or acceptance of its extractive toll on all ships passing through the Strait of Hormuz, these being Iran’s only guarantees that the US or Israel will not attack them again in 12 months.

It is in the US’s, and especially the Trump administration’s, interest not to further upset global energy markets. President Trump’s approval ratings on the economy were nose-diving to Joe Biden levels before the war started. By initiating a war of choice against Iran, the White House has sent energy prices upward, and the March CPI print showed what is coming for headline inflation figures in the coming months.

It appears likely that the Trump administration mistook Iran, a civilizational nation-state with millennia of history, for the kind of state where pressure produces quick concessions (e.g., Venezuela).

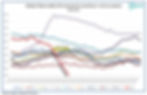

The key uncertainty is how these two entrenched positions resolve—and this is where objective reality matters less than the Trump administration’s perception of it. When I speak to energy analysts, it seems we are on the precipice of disaster, or perhaps already flung over the side and just waiting to realize it. The math, according to my friend Rory Johnston, is simple: Of the ~20 million bpd of oil that flowed through Hormuz pre-war, roughly 7 million has been rerouted (mostly via the Saudi East-West Pipeline and the UAE’s Habshan-Fujairah pipeline), leaving a 13 million bpd deficit—accumulating since mid-March at roughly 400 million barrels per month.

The cushion is thin: Commercial inventories have maybe 1–2 billion barrels of working capacity, and while the record Strategic Petroleum Reserve (SPR) release and drawdowns in oil on water can absorb much of that, a second SPR release of the same size is basically required to avoid a real crunch. If Hormuz stays closed long enough that you need to destroy 10+ million bpd of demand, you’re looking at $200+ crude. The market isn’t pricing that in because it’s trading the “geopolitics” (i.e., assuming either President Trump or Iran will concede), not the barrel math.

The $200 crude question is “When is long enough?” One concerning report from The New York Times cites administration officials as believing “that continuing the blockade for two more months would cause significant long-term damage to Tehran’s energy industry.” It would indeed, but it would also mean the Strait of Hormuz is effectively closed until June 28. Either the Trump administration is looking at different math than the energy experts I respect or it is underestimating Iran’s willingness to endure pain. Worth remembering: In the 1950s, Iran’s oil exports almost went to zero for years so that the Iranian government’s nationalization of the Anglo Iranian Oil Company could happen.

The Medium- to Long-Term Picture

Here, it’s more predictable…

Food and energy prices will stay elevated for 6–9+ months, with emerging markets bearing the greatest stress. Developed markets will feel it; developing ones could destabilize—recall that the 2007/08 food price spike helped trigger the Arab Spring. Early warning signs are already visible (e.g., Philippines protests around the rising cost of food).

Rising prices heading into the US midterms spell trouble for Republicans. Expect at least a Democratic House, maybe the Senate too, and resulting gridlock. Boxed in domestically, the Trump administration may double down on foreign policy, where Congress has less leverage. Looking ahead, the question is whether a centrist candidate emerges or the 2028 election shapes up as populist vs. populist (AOC-style left vs. Vance-style right). The implications for the world’s largest economy are hard to overstate.

Now that the Strait of Hormuz card has been played, there will be a swell of global capex to avoid future dependence on this chokepoint. It will take years to build the necessary infrastructure to limit the importance of Hormuz to the global economy, but it will happen. The world needs Middle Eastern oil, so pipelines will be built. Meanwhile, a huge wave of LNG is coming online by 2030.

Also, the UAE announced its decision to leave OPEC effective May 1, a leading indicator of exactly this dynamic. Abu Dhabi has chafed for years—nay, decades—under OPEC quotas that capped production at 3.4 million bpd, roughly 30% below capacity, while it invested billions in the Habshan-Fujairah pipeline specifically to bypass Hormuz. Now, with the chokepoint closed and the pipeline operational, the UAE is breaking free of Saudi-led production discipline to pursue its 5 million bpd capacity target by 2027. In effect, the Hormuz crisis has already fractured the institutional architecture that managed Gulf oil supply: OPEC’s ability to manage the market just lost its second-largest source of spare capacity.

China is positioned to win. Yes, it imports through Hormuz, but it holds larger reserves than regional peers, dominates renewables manufacturing, and is rapidly expanding nuclear capacity. Crucially, China controls the hardest-to-replicate layers of global industrial supply chains. Under geopolitical stress, buyers revert to China for reliability and scale. Watch Chinese industrials, chemicals, and logistics firms embedded in upstream supply chain layers that Vietnam and India can’t yet replicate.

The US could be a long-term winner if the shock finally forces a Western Hemisphere supply chain—Mexico nearshoring, deeper Canada integration, Latin American industrial ties. That’s bullish for US infrastructure, energy, and industrial capacity. The catch: It requires massive investment, meaning more debt and a weaker dollar. And short term, the inflationary hit lands squarely in a volatile political cycle likely to empower the populist politics that make executing any of it hard.

That’s the macro picture: uncertain in the short term, more predictable over the horizon, and full of second-order consequences most aren’t thinking about yet.

Map/chart of the week:

Blind Spot (or: What’s Not on People’s Radar but Should Be):

Peru held the first round of its presidential election on April 13. Keiko Fujimori, daughter of deceased former president Alberto Fujimori, came in first with 17% of the vote. She’ll face leftist Roberto Sánchez, a former cabinet minister under Pedro Castillo (currently in prison for trying to engineer a coup), in a June 7 runoff. The country has had eight presidents in 10 years, and yet its macroeconomic performance has been remarkably resilient: steady growth, low inflation, and a strong central bank.

Former finance minister Luis Miguel Castilla has warned that this decoupling of politics from economics is “increasingly fragile.” He’s right to worry. Sánchez wants a constitutional assembly, renegotiation of natural resource contracts, and changes to the central bank’s mandate, the very institutions that have kept Peru stable. Fujimori could actually govern (she has enough congressional seats to form a coalition), but has shown an authoritarian appetite, and thus far has destabilized the system every time she loses. Meanwhile, real problems go unaddressed by either candidate. Homicides have doubled since 2019. Reported extortions are up sixfold in five years.

Peru is a case study for US-China competition in the region. The previous president had to step down because of controversy around his dealings with Chinese business. China also just built a mega-port at Chancay and is buying up mining concessions across Peru. Classic resource extraction, but at least it comes with capital. When Peruvian diplomats have asked the State Department what the US is offering as an alternative to Chinese investment, the answer has been: Get rid of the Chinese first, and then we’ll talk. Unsurprisingly, it has not been well received.

Latin America’s story since the Europeans arrived has been resource extraction on someone else’s terms. There’s little in Peru’s first round of elections to suggest that is changing, or that Peru will succeed in pushing back the building crime wave.

What I’m watching: Unfamiliar (Netflix)

What I’m reading: Breakneck: China’s Quest to Engineer the Future, Dan Wang

What I’m listening to: Dark Side of the Moon, Pink Floyd

Jacob Shapiro

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

New from Jacob Shapiro × Mauldin Economics…

The World Isn't Ending

Geopolitics, translated for investors

The headlines say the world is going to hell in a handbasket. The reality is that it’s just being rearranged —and that there is opportunity amid the chaos. Join Jacob Shapiro every Thursday as he translates complex global power shifts into actionable intelligence for your portfolio.

Join thousands of investors who refuse to watch the world from a fetal position.

By opting in you are also consenting to receive Mauldin Economics' marketing emails. You can opt-out from these at any time. Privacy Policy

No mention of the US Navy opening the straight? Seems inevitable if Iran does not make a deal. Would not allow as many boats as before, but would certainly ease some supply.

The redrawing of voting boundaries in the US could have significant effects on the upcoming mid-terms. The SCOTUS rulings regarding Gerrymandering are significant.

Glad to see you here Jacob! Been following your stuff since Stratfor and your Latin American side project. Look forward to seeing your future articles!

The darkside of the moon, March 1973. a reflection to the changes that happend back 50 years ago.

We only can hope a 200$ price tag will transfer the energy consumption from fossile to alternativ, nuclear, photovoltaic, wind and thermal energy and make US(A) independant. And strong become a leader of a new 20first century.

2nd level impacts are hard to predict. Oil price increases are a tax that can lead to recession. The path of oil prices could be up sharply, then economic hardship from high prices may drive oil down-hard. The cure for high prices is high prices.

Current reserves are about 4,700 MM. Deficit is 8MM per day. If it is acceptable to reduce reserves by 1,200MM (about 25% drawdown), there is about 150 days of cushion. What would be the driver to push oil up to $200 in the next 3 to 4 months?