Have a Coke and a Smile

-

Jared Dillian

Jared Dillian

- |

- May 5, 2016

- |

- Comments

Jared Dillian

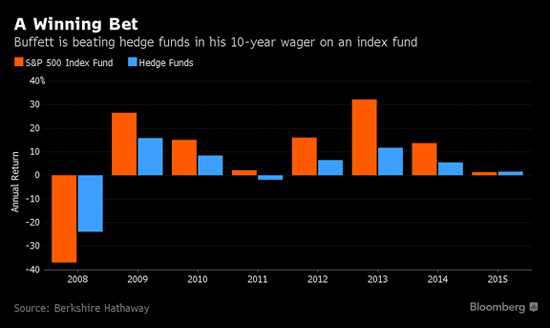

Jared DillianBack in 2008, Buffett made a very loud, annoying bet that the Vanguard S&P 500 index fund would outperform a basket of hedge funds over 10 years. Eight years into the 10-year period, Buffett is winning pretty handily. In the classic understatement we have come to expect from a former Business Insider editor, Joe Wiesenthal said that Buffett is “absolutely crushing it” on his trade.

Indeed he is. Here is the chart.

So a few things here. Buffett is very cynical and likes to take advantage of people’s stupidity. He also famously bet a billion dollars that nobody would pick a perfect NCAA tournament bracket, which he was mathematically certain to win.

This bet was a no-brainer from the start. Everyone knows that active managers underperform passive managers in the long run—this is not new. It’s been around since Malkiel and his random walk theory decades ago. Buffett is feeding the prevailing sentiment, which is that Wall Street people are corrupt and dishonest and charge lots of fees and add no value. People believe this because Buffett says it and he has credibility (hopefully they do not take his advice about drinking five Cokes a day).

But I’m going to ask you the same question I asked myself when I read A Random Walk Down Wall Street almost 20 years ago: If it were really true that active management was a fool’s errand, and that the hundreds of thousands of people who work in the money management business add no value, then why does it exist?

Because they do add value.

Minimizing Volatility

Go back to the chart above—what is the first thing you notice? I hope you notice that while actively managed funds underperform in up years, they outperform in down years.

There are many reasons for this, the first being that a hedge fund manager can go to cash. He can also short things, or even just go outright short. But even Buffett knows that the point of professional money management is not to simply beat the S&P 500.

The point is also to minimize volatility. Because if you can’t handle the volatility, then you’re likely to vomit out of your investment at the worst possible time—on the lows.

This is very important. Vanguard offers a whole slate of very low-fee index funds. You can sign up at Vanguard.com and send them some money and get started. You can look at the 1/3/5/10-year performance of these funds.

Now, here is the $24,000 question: Do you think people really realize the performance in these funds, or maybe do a bit worse?

They definitely do worse, because human beings are human beings, and if you are long the Vanguard Energy Fund, and it goes down 40%, you are going to barf it, and then you are going to buy it back when it goes up 40%. If you instead invested in a hedge fund, which was rolling around with 20% cash and shorted stuff on the way down, maybe you would only lose 15%—and make it all back, and then some, on the way up.

But guess what—minimizing volatility enabled you to stay in the trade and continue to compound returns over time. If you barf, the compounding comes to an end.

Buffett likes to say that you should buy and hold stuff forever, like he does, but not everyone is Buffett. Not everyone has permanent capital, not everyone has godlike status among his shareholders, and quite frankly, not everyone has the constitution Buffett has.

When things go down, Buffett buys more, which is what you are supposed to do (if you are a value investor). He says you are supposed to have a really long time horizon, like, forever. He is right. But most people can’t do that.

Like what you're reading?

Get this free newsletter in your inbox every Thursday! Read our privacy policy here.

But at least the fees are low…

The Brokerage Industry

In addition to active management, the other class of people on Wall Street who get beat up pretty consistently are the brokers. The conventional wisdom is that these guys add no value and get paid to churn your account and jam you into mutual funds with fees so they get kickbacks. Some or all of that may be true. But you know what else they do? They talk you out of selling on the lows.

The most important function of a broker or investment advisor is to save you from your own worst instincts. They are amateur psychologists—when the market goes down 10-15%, they get calls from all the widows and orphans who want to sell their XYZ utility stock. The broker talks them out of it. He is acting in his own self-interest because he doesn’t want to lose assets, but temporarily, the interests of the broker and his customers are aligned. The broker is actually doing right by the investing public, by keeping them invested.

Of course, every 50 years we have this extinction-level event like the financial crisis, but even then, you would have been much better off holding on to your hat (just like Buffett).

The Conventional Wisdom Is (Almost) Always Wrong

The conventional wisdom is that:

- Active management is dumb, you just need to be in index funds

- Hedge funds add no value, considering how much they charge

- Brokers are fools

All wrong. If hedge funds really added no value, then why would the richest people in the world invest in them? Are they all stupid?

Professional money management is first and foremost about minimizing losses, which is something you don’t get from an index fund. That takes talent, and costs money. An individual hedge fund can blow up from time to time, but the industry, by and large, does a pretty good job of conserving capital and—more importantly—giving you exposure to uncorrelated strategies that you can’t get at Vanguard.com.

Buffett knows all this, but ironically, it is Berkshire that has been doing a good job of closet indexing of late.

There are legitimate criticisms of active management (like closet indexing, for one) and there are legitimate criticisms of brokers, but to say that both industries shouldn’t exist is just moronic.

Let me put it this way. If you won the $350 million Powerball, would you put it all in the Vanguard S&P 500 Index Fund?

I didn’t think so.

* * * *

If you’ve been reading The 10th Man for a while and enjoying it for the infotainment, you might have missed that there have been a few pretty great calls in here.

Back in February, I noticed that base metals and industrial commodities were starting to turn, and I predicted that the inflation trade would be back.

Boy, is it ever.

By the way, if you ever wondered what my “other” newsletter for sophisticated investors, The Daily Dirtnap, is like, wonder no more. From May 9–13, you have the opportunity to experience it completely free for one week—no strings attached. Sign up here for your free 1-week trial.

subscribers@mauldineconomics.com