From Theory to Reality

-

Ed D'Agostino

Ed D'Agostino

- |

- April 14, 2023

- |

- Comments

Ed D'Agostino

Ed D'AgostinoA stress test is exactly that: a test. It is a mix of assumptions about adverse events and their theoretical outcomes. Ironically, the Fed released its 2023 bank stress test scenarios just weeks before the latest banking crisis erupted.

The Fed’s scenarios included just about every severe event that seemed likely to happen—including a 40% drop in commercial real estate values, a 45% stock market crash, a deep recession, and even inflation.

But it missed the obvious catalyst for today’s brewing liquidity crunch: rising interest rates.

Not so obvious is another factor that might be a threat to the stability of the financial system: shadow banking. I say “might” because it’s hard to know—and that’s the problem.

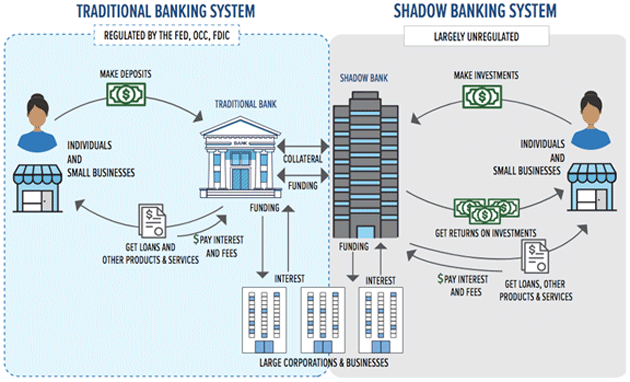

Only the Shadow Knows

Despite the nefarious-sounding name, shadow banking is completely legal and a necessary element of the economy. The label is widely used to describe non-bank institutions that act as lenders or as intermediaries between borrowers and lenders.

Source: Better Markets

Hedge funds, private equity groups, insurance companies, mortgage lenders, pension funds, money market funds, and investment funds are all examples of shadow banks.

The formal name for a shadow bank is “non-bank financial institution,” or NBFI.

The outsized risk posed by NBFIs became apparent during the 2008 financial crisis. The imminent collapse of insurance giant AIG forced the Fed to intervene and bail out the company. A company that would normally fall outside the Fed’s purview.

AIG was part of the shadow banking system. Although not a bank, the consequences of its failure would have been as catastrophic as a big bank going under.

The “shadow” part comes from the unregulated and complex nature of the system. Shadow banking companies are not subject to the same regulations—such as reserve requirements—that commercial banks must comply with. Because of that, they can operate with higher levels of risk than traditional bank lenders.

On the flip side, shadow banks can offer a broader range of borrowing options. And many industries now rely on this system for financing. That includes the commercial real estate industry that I wrote about last week.

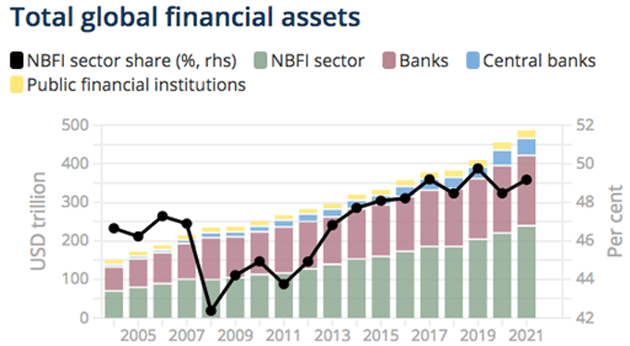

The number and penetration of NBFIs have grown rapidly over the past decade, as seen in the chart below:

Source: Financial Stability Board

According to a December 2022 Financial Stability Board report, the NBFI sector grew 8.9% in 2021 to $239.3 trillion (the latest full-year numbers). And its share of total global financial assets grew from 48.6% to 49.2% in 2021.

S&P Global Ratings reports that investment funds were the fastest-growing segment over the past decade, with nearly 80% of all shadow banks’ assets.

An Opaque System with Clear Hazards

S&P Global sees another hazard: contagion. The failure of a large shadow bank—or a reduction in its willingness to extend financing—would have an impact on the traditional banking sector.

There would be contagion via shared exposure to the same client base and financial market losses. The full picture is unclear as it’s hard to identify and quantify sources of systemic risk.

Of particular concern is the behavior of non-banks during financial market stress.

A February 2023 working paper from the Bank for International Settlements (BIS) notes that “non-banks contract their syndicated lending by significantly more than banks during shocks … [and] lending relationships with non-banks do not improve borrower’s access to credit during crises.”

If that holds true today, we will soon relearn how the shadow banking sector can act as both the trigger and amplifier of market stress.

There has been speculation about how the shadow banking system can work at odds with the Fed’s monetary policy tightening. But the opposite can also be true.

As the Fed works to smash liquidity—and thus slow the economy and, hopefully, inflation—a pullback in lending from shadow banks could magnify its efforts.

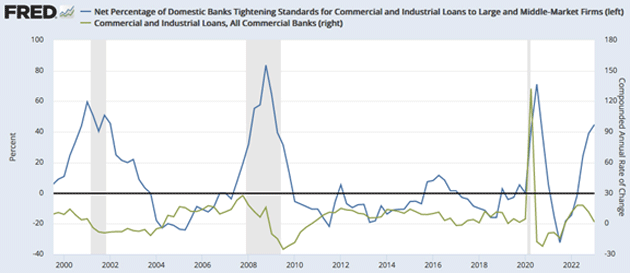

And we now have hard data showing banks are doing just that—tightening their purse strings.

Source: St. Louis FRED

The above chart shows the latest data from the Fed through Q1 2023, and the trends are not encouraging.

Loan standards have been tightened by 44.8% of banks (blue line), and loan growth (green line) has stalled and looks headed toward zero, and likely worse.

Just as telling is the gap that has opened up between these two metrics. Excluding the 2020 pandemic recession—a statistical outlier—similar gaps appeared just prior to or at the start of the 2001 and 2008 recessions. More evidence of an impending economic downturn.

The Fed’s H.8 report—a snapshot of US commercial bank’s assets and liabilities published every Friday—gives a more granular picture of lending.

The report tells us that bank credit contracted $311 billion—or 1.77% in just two weeks—from the implosion of Silicon Valley Bank to the end of March. The evidence suggests we should expect the shadow banking sector is making similar adjustments in its lending.

I will dig deeper into the risks posed by shadow banks in my upcoming discussions with Felix Zulauf, Louis Gave, Peter Boockvar, Lacy Hunt, Jim Bianco, and others at next month’s Strategic Investment Conference. The conference is 100% online but live, kicking off on Monday, May 1. You won’t want to miss it—over 50 speakers are bringing their best ideas to the table. From geopolitics to economics to investing, there is something for every Mauldin Economics reader. I hope to see you there.

You can see the full list of speakers and the agenda by clicking here.

Best regards,

Ed D’Agostino

Publisher & COO