![A Tale of Two Banks [Interview]](https://images.mauldineconomics.com/uploads/newsletters/FEATURE_20230508_SMM.jpg)

A Tale of Two Banks [Interview]

-

Thompson Clark

Thompson Clark

- |

- Smart Money Monday

- |

- May 8, 2023

Thompson Clark

Thompson Clark| Editor’s Note: With another bank collapsing—i.e., the recent failure of First Republic Bank (FRC)—we wanted to grab another interview between Aaron Gentzler, associate publisher of Mauldin Economics, and Thompson Clark, editor of Smart Money Monday and High Conviction Investor, to get their thoughts on the developing crisis and how investors can position themselves. |

Aaron Gentzler: Thompson, you’ve been writing about the recent bank failures lately. First, it was Silicon Valley Bank. Then, last week, we saw the failure and subsequent takeover of First Republic Bank. What’s your take on where we stand now?

Thompson Clark: Aaron, great to talk to you again. The main reason for writing so much about banks is that I can’t help but look at beaten-up companies and sectors. There’s almost always money to be made when the market throws the baby out with the bathwater.

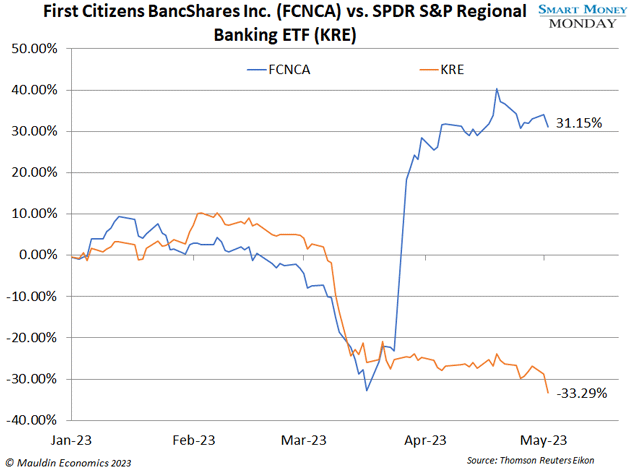

Aaron: Well, your recommendation of First Citizens BancShares Inc. (FCNCA) proved timely. But I’m curious… what are your latest thoughts on JPMorgan Chase & Co.’s (JPM) First Republic takeover?

Thompson: Right, I wrote about First Citizens Bank in February 2022, calling it “the only US bank stock I’m buying.” Its takeover of the loan book at Silicon Valley Bank doubled its assets, and it effectively paid almost nothing. It’s one of the wildest deals I’ve ever seen. First Citizens is the best-performing regional bank stock in the market this year because of this deal.

The company I spent quite a bit of time on (but ultimately passed on) was First Republic. First Republic didn’t fail fast… it took a few months. I even dug into the preferred stock of First Republic. But ultimately, I told readers to avoid it. It had too many problems. Now, JPMorgan is the new home for First Republic customers.

Aaron: And you like JPMorgan?

Thompson: Yes, I do. Well, more specifically, I like the preferred stock of JPM. It’s a safer way to beat the market—you get cash interest, plus upside if JPMorgan redeems the preferreds at par in 2024.

First Citizens vs. First Republic

Aaron: Got it. Now, for readers out there wondering why you targeted one bank over the other, can you help us understand why you were so bullish on First Citizens but so bearish on First Republic?

Thompson: There are two reasons, really. First, insider involvement. CEO Frank Holding, Jr. and his family own a massive percentage of stock in First Citizens. They own over 20% of the bank that’s currently worth $2.1 billion. Insiders, especially those at banks, tend to have a multidecade time horizon. This is especially true with the Holding family. Frank Holding, Jr.’s grandfather joined the bank in 1918, rose to president in 1935, and the Holding family has remained in leadership roles ever since.

This long-term view keeps them away from riskier lending. Riskier lending doesn’t just mean avoiding loans to profitless tech companies. It also means making loans at absurdly low interest rates. Or even buying long-duration bonds that get crushed when interest rates rise (which they have).

First Republic and Silicon Valley Bank got in trouble reaching for a few more basis points in yield by going out on the duration curve. First Citizens hasn’t chased this yield like others. And thus, they’re still standing while others are not.

“Sticky” Deposits Are Critical to a Bank’s Health

Aaron: Okay, so insider ownership is key. Anything else you’d say differentiates these two banking setups?

Thompson: Insider ownership is one. The other is more nuanced to banking: deposits. Banks need deposits to make loans. A bank with $1,000 in deposits can lend 10 times that amount—or $10,000 in loans. It’s critical for a bank to have sticky deposits. If those deposits leave, you can’t make any loans. Or, to be in regulatory compliance, you might even have to sell the loans you have.

One way to have stickiness is to have lots and lots of smaller customers. First Citizens has been a staple bank in its communities for more than 100 years. All the smaller customers are well under the $250,000 FDIC limit… so they don’t freak out and move their money thinking the bank will go under.

Contrast that with First Republic, which is—or was—the bank of the wealthy. As I wrote in the March 27 edition of Smart Money Monday, Mark Zuckerberg famously got a mortgage with First Republic.

Like what you're reading?

Get this free newsletter in your inbox every Monday! Read our privacy policy here.

This Bank Stock Shares Similarities with FCNCA

Aaron: Got it, so insider ownership and deposit mix. That makes sense. Are you finding any other opportunities in banks?

Thompson: There are a few spots that have piqued my interest. In my High Conviction Investor portfolio, we own one small bank. My thesis here is somewhat like First Citizens. This bank has a rock-solid balance sheet and is over-capitalized. In addition, it has a sticky, local deposit base.

In its recent quarterly earnings release, it announced that its deposits actually increased. This is a major difference when compared to First Republic, where deposits fled. Again, having sticky deposits is extraordinarily valuable. My thinking is that, at some point, this bank will get acquired.

Aaron: Very interesting. Any idea when it’ll get bought?

Thompson: Good question. It’s probably a 2024 event, but we will see. In the meantime, it’s doing the right thing by repurchasing shares at attractive prices.

Aaron: Great—for any readers who aren’t members of Thompson’s premium advisory and want to learn more, you can grab all the details here.

With that, any final thoughts on banks?

Thompson: So, we’ve already seen two of the largest bank failures in history this year. This is nearly a direct result of the Federal Reserve rapidly hiking interest rates over the past 12 months. The growth rate of inflation is slowing, which should lead the Fed to pause its hiking. In addition, we’re starting to see unemployment slowly begin to creep up. Those two factors are signals to me that the Fed will pause rate hikes.

On the loan side, there’s no question that some banks will run into trouble. The collateral underlying their loans, such as office buildings or apartments, may be impaired. That is, the assets may be worth significantly less than the loan outstanding against it. We haven’t seen that start to tick up yet in the numbers, but I suspect it’s coming.

For now, I’m sticking to my spots and continuing to hold on to my FCNCA stock.

Aaron: Thompson, thanks again for speaking with me on such short notice. I know readers find your take on banks valuable, and I hope we helped answer any questions they may have.

Thompson: You bet, Aaron. Thanks for chatting with me.

Thanks for reading,

—Thompson Clark

Editor, Smart Money Monday