$2 Million Starter Homes - Bubble?

-

Thompson Clark

Thompson Clark

- |

- Smart Money Monday

- |

- March 21, 2022

Thompson Clark

Thompson ClarkWhen you imagine a $2 million house, it’s probably big and fancy.

Well, here’s what that kind of money gets you in a “middle class” suburb in the San Francisco Bay Area:

Source: Zillow

The house is just what it looks like: An ordinary 3-bedroom home. And it sold for $2.23 million in December 2021. This is the sort of astronomical price that has investors wondering if housing prices will crash like they did in 2007/2008.

We are certainly hearing echoes of the housing bubble. In the five years before the housing crash, US homes prices soared 60%, according to the S&P/Case-Schiller Home Price Index. In the past five years, housing prices have soared 51%.

The key difference is: This time there is no concrete catalyst to push housing prices lower.

-

There’s nothing like the catalyst famed investor Michael Burry pinpointed before his legendary housing short…

You probably know Burry, founder of hedge fund Scion Capital, from Michael Lewis’s New York Times bestseller The Big Short (or the movie by the same name).

Scion Capital was short housing right before the market collapsed in 2007/2008. Burry’s thesis for the trade was a hard event: the repricing of subprime, adjustable-rate mortgages.

Here was the setup…

During the housing bubble, a bunch of low-credit (subprime) borrowers purchased homes. Lenders lured them in with dreams of ultra-low payments (made possible by introductory or “teaser” mortgage rates), continually appreciating home values, and a chance to refinance when their mortgage rates increased.

The mess didn’t end there. Banks bought and packaged up those subprime loans as securities. Then the rating agencies slapped AAA ratings (the best possible) on those securities. And the banks sold the securities to institutions and other investors.

-

Burry predicted this house of cards would collapse when the teaser mortgage rates ended.

He said that would be the catalyst. From there, borrowers would see their payments skyrocket. They wouldn’t be able to make the payments. And a wave of defaults would come crashing down.

|

EARLY OPEN: SIC 2022: Pre-Order Your Virtual Pass Today! “Goodbye Normal” is the fitting theme for the 5+1 action-packed days of this year’s Strategic Investment Conference. Watch and interact with over 40 world-class speakers in 35 live sessions. What will happen in the economy and markets over the next 12 months? What is the future of energy? How can you protect your assets and find the best undervalued companies for outsized profits? Click here for more details and to pre-order your Virtual Pass at a 44% discount. |

Burry’s “big short” thesis proved correct. He personally made $100 million on the trade—and a lot of investors fantasize about recreating that windfall.

Like what you're reading?

Get this free newsletter in your inbox every Monday! Read our privacy policy here.

-

But home prices didn’t crash in 2007/2008 because they had climbed so high.

Home prices crashed because, among other things, borrowers couldn’t make their mortgage payments.

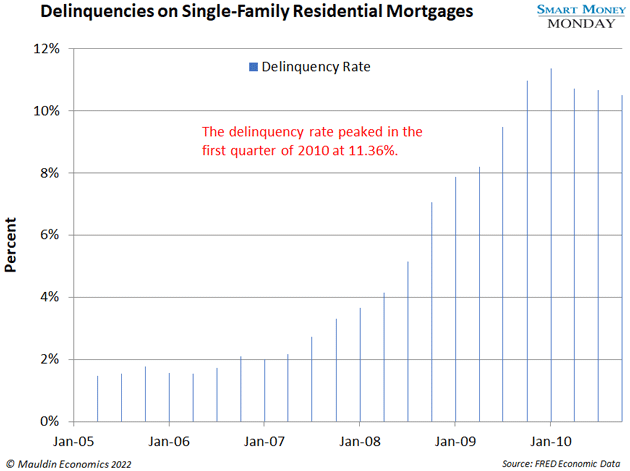

If you’ll recall, the Federal Reserve ratcheted up the fed funds rate from 1% in May 2004 to 5.25% in July 2006. That led to higher mortgage payments for all those subprime borrowers when their teaser periods ended. And boom! Delinquencies and defaults began to spike.

As you’ll see in the chart below, the delinquency rate peaked in 2010 at 11%.

-

We have one element from the housing crash today: rising rates.

Last week the Fed announced a 0.25% rate increase. The consensus view is that we should expect seven or so rate hikes this year. But that alone isn’t enough to trigger a housing crash. And the other elements of the pre-2007 housing bubble are missing.

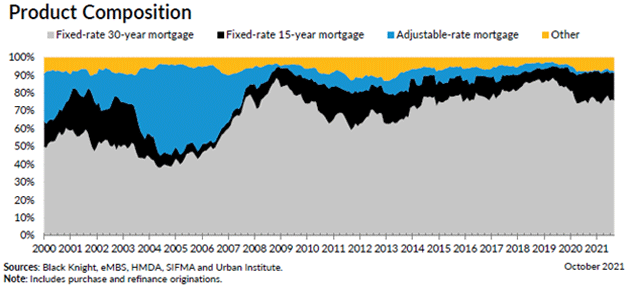

As I mentioned earlier, adjustable-rate mortgages were a key feature in the housing bubble. From 2004 to 2006, around 45% of new mortgages originated had adjustable rates. However, for the past 10 years, that figure has hovered under 10%. That is critical. It means rising interest rates won’t increase most mortgage payments.

Source: Housing Finance Policy Center

Also, mortgage lenders have tightened standards since the housing crash. For instance, Fannie Mae, the largest mortgage purchaser in the US, has stopped purchasing mortgages with low- and no-credit documentation. It’s also stopped purchasing interest-only loans.

Higher quality loans and the ultra-low percentage of adjustable-rate mortgages means that even if home values correct a bit, we’d have no reason to expect another wave of defaults. Sure, you would see a smaller number if you plugged your address into Zillow. But unless you lost your job or needed to sell your house fast, a correction would have little consequence. You’d just keep making your mortgage payments and wait for prices to recover.

-

So, how could we play the continued strength in the housing market?

For starters, home builders look cheap. So do mortgage originators. I’ve been looking at Rocket Companies (RKT), the owner of Rocket Mortgage. Its share of the mortgage origination market grew from 1.3% in 2009 to 8.8% in 2021. That is still a small slice of the pie, which bodes well for future growth.

2020 and 2021 were record years for mortgage originations, with over $4 trillion in new mortgages originated (both purchases and refinances). New mortgage originations should slow as interest rates rise. But that may give Rocket a chance to gobble up market share as the weaker players fall.

Analysts are forecasting a little over $1 per share in earnings for 2022. So, the stock is trading at 10X earnings—not terribly compelling. I’m putting it on the watchlist for now.

Thanks for reading,

Like what you're reading?

Get this free newsletter in your inbox every Monday! Read our privacy policy here.

Editor, Smart Money Monday