Are You Falling Victim to This Simple Investing “Rule”?

-

Thompson Clark

Thompson Clark

- |

- Smart Money Monday

- |

- October 24, 2022

Thompson Clark

Thompson ClarkInvestors love easy-to-follow “rules.” The simpler, the better.

In the ’70s, they latched onto the Nifty Fifty. These were 50 stocks you could seemingly buy at any price and be guaranteed a solid return. They were described as “one-decision”—buy them and watch them climb. Of course, it didn’t work out that way.

In the late ’90s, anything with “dot-com” was all the rage, price and valuation be damned. Just buy the story and it’ll work out… or so the rule went.

Over the last 100 years, however, one rule has reigned supreme: the 60/40 portfolio.

As you probably know, the 60/40 portfolio is comprised of 60% stocks and 40% bonds.

It’s the most common, simplest investing rule on the planet. And for most of the past century, it’s been a smart and safe “hedge.”

But in 2022?

The 60/40 stock and bond portfolio is having its worst year in a century...

Down 21.5%+ year to date.

Today, I’ll explain why I don’t personally use the 60/40 approach. Plus, a much better option for those looking for a fixed income alternative.

|

Bear Market Rally, Or Bull Market Kick-Off? 23-year market veteran Jared Dillian says, “the market is turning around with a vengeance.” Thousands will miss out on this once-in-a-20-year opportunity. Do not be one of them.

|

The Problem with the 60/40 Theory

The theory goes that in a bull market, the stock portion of your portfolio appreciates, while your bond portion remains flat but pays out cash interest.

In bear markets, like we’re experiencing now, your stock portion falls… but your bond portion rises. So, historically speaking, your all-in results wouldn’t be dire. The stock market may be down 20%, but a 60/40 portfolio might be down only a few percentage points.

Like what you're reading?

Get this free newsletter in your inbox every Monday! Read our privacy policy here.

-

Stocks in the red = recession;

-

Recession = rate cuts from the Fed;

-

Lower rates = higher prices for bonds.

For the most part, the 60/40 rule has worked for investors… that is, until now.

And instead of blindly following the rule like most folks, you should ask yourself this critical question:

What About Interest Rates?

During COVID mania in the summer of 2020, the 10-year US Treasury sank as low as 0.5%.

All other bonds are priced in relation to this key benchmark. So, with Treasuries at 0.5%, other corporate bonds had extremely low yields as well. That means sky-high prices.

And after the massive amount of stimulus pumped into the economy, inflation predictably rose.

Inflation today is still sky-high. But the Fed is responding as they should: by raising interest rates.

Now, back to our formula for bonds:

-

Rates down, bonds up;

-

Rates up, bonds down.

With interest rates skyrocketing, the “40” in the 60/40 rule has gotten smoked.

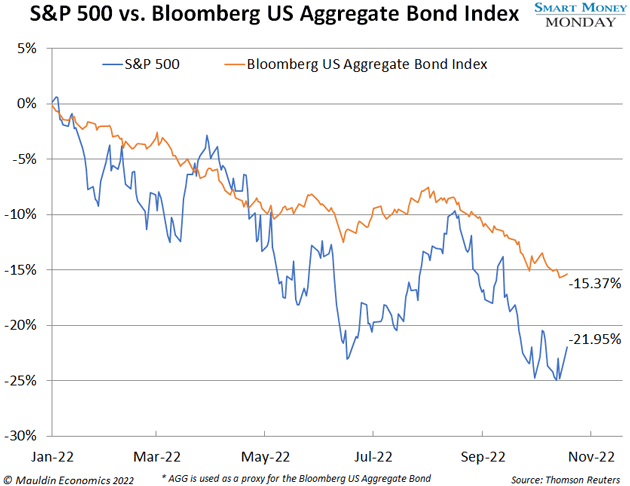

And on the ”60” side, inflation, geopolitical issues, and fears of a recession have sent stocks tumbling as well. You can see stocks (blue line) are down 22% this year while bonds (orange line) have fallen 15%:

Nobody Has Been Spared

The point is: Beware of simple rules of thumb in investing.

Like what you're reading?

Get this free newsletter in your inbox every Monday! Read our privacy policy here.

Does it make sense to buy bonds with interest rates hovering around 0%? Or to hold on to a bond and generate a meager 1% return?

Of course not. But that’s what 60/40 practitioners did, and they’ve been punished for it.

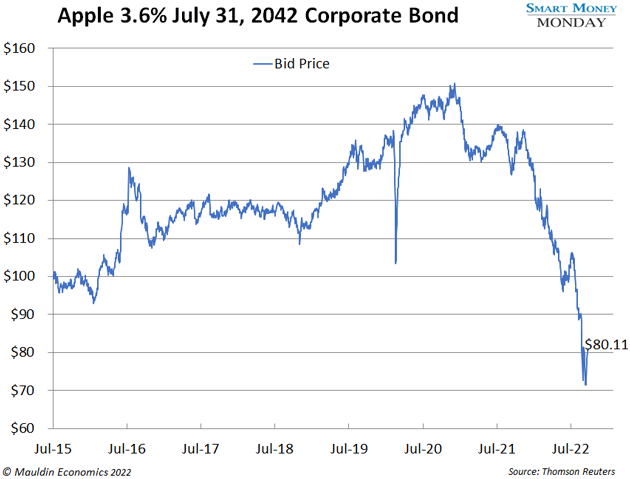

Equities are down big this year. So are bonds. Even tech giant Apple Inc. (AAPL) hasn’t been spared.

Apple stock investors are down 20% this year.

But Apple bond investors—specifically those who own the 3.6% 2042 bonds—are down over 25% year to date:

The Only Fixed-Income Instruments I’d Buy

With bonds so blown out, the 60/40 portfolio may work from here.

However, that’s not a chance I’m willing to take—not with the way it’s trending.

For a better allocation to fixed income, I like simple, plain-vanilla US Treasuries.

The key is to stick to a short duration. Going out further on the maturity date creates more risk for little, if any, benefit.

Right now, you can buy 1-year Treasuries that yield 4%. If you hold to maturity, you’ll generate a 4% return—which is great in today’s market.

You can also look at two exchange-traded fund (ETF) options on the short end of the curve: the iShares Short Treasury Bond ETF (SHV) and the iShares 1–3 Year Treasury Bond ETF (SHY).

SHV is yielding 3.15%, while SHY is yielding 4.24%. It’s important to note that SHV is less sensitive to interest rate risk than SHY.

Thanks for reading,

—Thompson Clark

Editor, Smart Money Monday