The Silver Lining to Investment Losses in 2022

-

Thompson Clark

Thompson Clark

- |

- Smart Money Monday

- |

- November 21, 2022

Thompson Clark

Thompson ClarkBelieve it or not, 2022 is almost over.

That means it’s time to start thinking about end-of-year tax planning strategies…

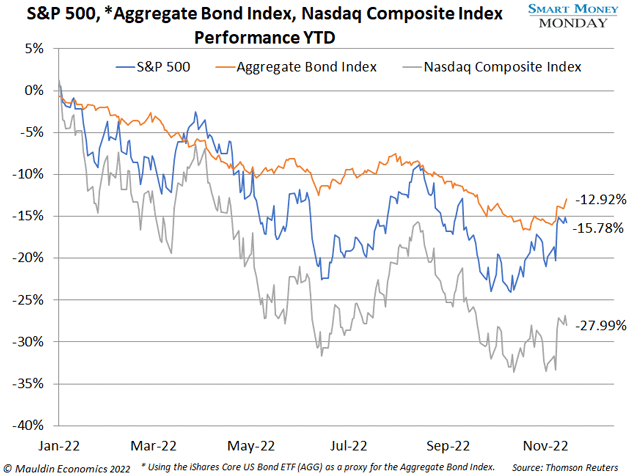

Especially since it’s been such a painful year for the markets, with most stocks slipping into the red. As you can see below, at the time of this writing, the S&P 500 and the Nasdaq are down 15.78% and 27.99%, respectively. Even the Aggregate Bond Index has fallen 12.92%.

Now, depending on when you bought in, you might have some losers in your portfolio. But even though the current bear market has been challenging (to say the least), it’s not all bad news because there’s a silver lining to lagging investments—one that can help you save some money this upcoming tax season.

I’m talking about tax loss harvesting. It’s something you should be considering this time of year. I know I am.

How Does Tax Loss Harvesting Work?

Tax loss harvesting is a straightforward concept. It’s the process of strategically realizing capital gains and losses to minimize your tax liability.

In the US, individuals owe taxes only on realized capital gains. You must sell a stock to realize a capital gain or loss. Unrealized capital gains are not taxed.

Obviously, no one likes to take a loss. But if you have other realized gains, it’s often a smart idea to sell a “loser” to realize the tax savings.

Say you have unrealized long-term gains of $15,000 on a stock you really like. Then let’s say you have unrealized losses of $20,000 on a stock you still like, but it’s currently down.

With some planning, you could sell both this year and realize the gains and losses. In this instance, you’d generate a $5,000 capital loss.

Assuming you’re married, $3,000 of that loss could offset any ordinary income you generated during the year. And the remaining $2,000 would be carried forward to future years to offset future realized capital gains.

|

[Join John Mauldin's Inner Circle] With the economic crisis hitting both here and abroad, many are wondering... How are the top economists, political strategists, and financial thinkers preparing and positioning themselves today? Click here now to find out how 10,000+ readers are following their guidance. |

Can You Buy Back the Stocks You Sold?

That’s the harvesting aspect.

Can you still own them? Yes, but with a caveat…

The IRS lets you buy stocks back, but you must wait 30 days. If you buy within 30 days of selling a stock, you fall into the “wash-sale” rule.

Like what you're reading?

Get this free newsletter in your inbox every Monday! Read our privacy policy here.

So, if you plan on buying back a stock you sold, keep it simple: Wait a full 30 days so you can claim your initial loss.

Now, if you’re a long-term investor like me, tax loss harvesting is still worth consideration. That’s because 30 days later, when you repurchase a stock, you’ve locked in a new basis. And hopefully by then the stock will have started to move higher.

On the other hand, if you don’t expect a sold stock to ever recover, well… there’s no obligation to buy it back!

Only in Taxable Accounts

Note that tax loss harvesting does not work for retirement accounts such as a Roth IRA or 401(k). These accounts are non-taxable, so the gains and losses you realize inside of them do not create tax liability.

The only types of brokerage accounts that matter for tax loss harvesting are taxable brokerage accounts. That is, accounts you open in your own name and fund with after-tax cash contributions.

This is extremely important, so make sure you bear this in mind to avoid making a mistake.

Final Word

Before making any major moves with your investments, be sure to confirm the tax treatment with your accountant.

Please note that this is not tax advice. Rather, it’s a strategy that can help you save some money on your taxes.

If you’re interested in going this route, take a good look at your portfolio and identify any opportunities before the end of the calendar year.

Every dollar saved counts, especially when that tax bill comes due on April 15.

With that, I’m curious: Have you had success in the past with tax loss harvesting? Do you plan on using this strategy? Do you have any other questions about it? Let’s keep the conversation going—just drop me a line at subscribers@mauldineconomics.com.

Thanks for reading,

—Thompson Clark

Editor, Smart Money Monday