These New “Utility” Stocks Are Heating Up

- Robert Ross

- |

- The Weekly Profit

- |

- July 1, 2020

The US economy is in a recession. In the past, this would have led to reduced energy use. But this year’s extended coronavirus-induced shutdowns are producing the opposite effect.

This summer, one-third of Americans can expect to see a 10% to 15% jump in their utility bills. That works out to about $2 to $37 a month, according to energy analytics company Arcadia.

I’ve always been a big fan of betting on utilities. They provide the services we need—keeping the lights on, the water flowing, and the trash picked up—no matter what’s happening in the economy.

They can also provide a reliable, and oftentimes reliably market-beating, income stream for investors. For example, the Vanguard Utilities ETF (VPU) offers a nice 3.3% payout. That’s more than double the S&P 500’s 1.9% yield.

That’s because they hold companies people will use—and pay—no matter what.

There’s Another Type of Utility That’s Heating Up

There are many ways to invest in utilities. ETFs like the Vanguard Utilities ETF (VPU), the Invesco Water Resources ETF (PHO), and the VanEck Vectors Environmental Services ETF (EVX) provide steady (but slow) growth.

There are also high-growth companies… which can sound like an oxymoron if you’re only thinking about the stalwarts that provide water, electricity, gas, and trash/recycling pickup services.

I’m talking about high-growth utility-like companies that also provide a service people need, no matter what.

And one that is seeing the fastest growth is payment processors.

The Fastest-Growing Utility on the Planet

Payment processors are extremely similar to utility companies.

Just like someone who will turn on their lights no matter what, businesses will always pay tiny transaction fees to smooth the payment process.

That’s truer today than ever. One of the major themes at Mauldin Economics’ recent Strategic Investment Conference was trend acceleration. This includes everything from telemedicine and e-commerce to—you guessed it—payment processing.

Last week we dove deep into the exploding e-commerce industry. US online spending increased 49% in April alone. And going forward, four out of 10 shoppers say they will spend more money online because of COVID-19.

Payment processors like PayPal (PYPL) and Square (SQ) are well-positioned to benefit. Their platforms help you move money from your online account to businesses’ accounts… seamlessly and securely.

As a reward for making it easier for you to spend money, businesses pay a small fee to these processors.

Just like an electric utility is the backbone of the energy grid, online payments are the backbone of the e-commerce market.

That’s why…

Online Payment Growth Has a Ton of Room to Run

There are two major trends fueling online payments. First, e-commerce spending is still only 10% of all US retail sales. Considering that COVID-19 is pushing more people to buy goods online, this trend shows no signs of slowing.

But the second is less obvious. For instance, a recent report from management consulting firm McKinsey showed that 71% of global transactions are still done with cash. That’s down from 86% in 2015. And with the coronavirus creating an urgent need for easy, contactless, and secure payments, that figure is only going to keep dropping.

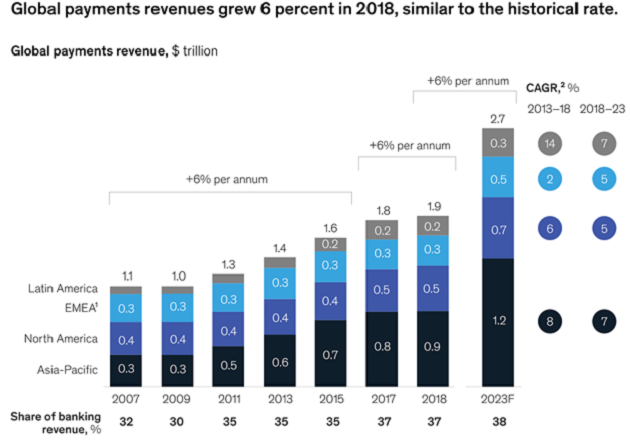

This sector was surging long before COVID-19. Online payments saw double-digit global revenue growth (11%) for the first time in 2017. That figure grew another 6% in 2018 to hit $1.9 trillion in global revenue and should keep growing 6% annually.

At that rate, this market is expected to surge to $2.7 trillion by 2023:

Source: McKinsey & Co.

And thanks to more customers shopping at home—and using online payment systems to do it—we could see even bigger growth, and a lot sooner than anyone could have imagined.

Clearly, there is a lot more room for growth. With long-term e-commerce growth plus the transition from cash to payment processors continuing, the future is bright for this sector… and for investors.

Two Ways to Profit from Online Payment Systems

Online payment processors have those two key trends working in their favor. But PayPal and Square are far from the only players in this increasingly lucrative space. And my Equity Evaluation System (EES) tells me they may not even be the best ones.

This model uses 100+ criteria to find the best opportunities in US stocks. Not only does my EES system get my readers into the best stocks, but also shows which “dogs” to stay away from.

Right now, it’s telling me that one of the top ways to profit from the explosion in online payments is American Express (AXP).

Amex has 114 million cards circulating worldwide. But those are mainly geared toward travelers, so the stock has taken a hit in 2020. However, the company gets paid every time a cardmember pays a bill or makes a purchase, so the long-term picture remains bright. And with a 1.8% dividend yield on a low payout ratio of 25%, it’s perfect for an income investor’s portfolio.

Next on my EES ranking is Mastercard (MA). As the world’s third-largest payments company, Mastercard processed $4.8 trillion worth of transactions in 2019. And while the company offers a mere 0.6% dividend yield, the long-term growth for the firm can outweigh anything lost in dividend income.

While both Amex and Mastercard scored well on the EES, there’s one company that was far above its peers. I’m sending this trade out to my subscribers as early as this week. Click here to see how you can be among the first to find out what it is.

Robert Ross