5 Investments to Volatility-Proof Your Portfolio

-

Jared Dillian

Jared Dillian

- |

- December 3, 2020

- |

- Comments

Jared Dillian

Jared DillianAsset allocation is the most important thing in the world. Yet, most investors spend zero time thinking about it.

Maybe they have a brokerage account with 10 tech stocks in it and think they are diversified. Or they have an S&P 500 index fund and they think they are diversified… even though 50 million other people are in the same trade.

I’ve read a lot of really bad literature on asset allocation that encourages people to put their entire portfolio in stocks—even just growth stocks—simply because they return the most.

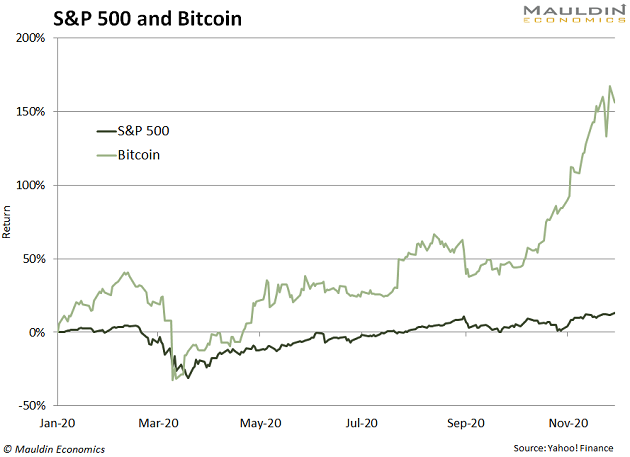

It’s not hard to poke holes in that argument. If you want to invest in the thing that returns the most, then why not put all your money into bitcoin?

Too risky! But if bitcoin is too risky, why are stocks safe? There are lots of stocks that are more volatile than bitcoin.

What People Get Wrong about the Right Risk-Reward Balance

People target returns in their portfolio without putting any thought into risk. They get an idea in their heads of what they want their portfolios to return, so that’s what they target.

I think people have it completely backward.

- Instead of targeting returns in their portfolios, they should target risk—with returns being a secondary concern.

The whole idea of investing is that you construct a portfolio that you can hold through the ups and downs, and there will inevitably be downs.

Here’s what happens—people have a risky portfolio consisting of only growth stocks, they sustain a 40% drawdown, and it causes them so much stress that they are forced to liquidate it—and then the returns stop compounding.

- Your goal is to build a portfolio that will help you stay invested.

You could achieve this by constructing a portfolio with less risky stocks. But they’re still stocks, and subject to the same macro factors that affect all stocks.

You need exposure to different asset classes that are less correlated or negatively correlated. That's what reduces your risk.

It may also reduce your returns. But if you’re creative about it, it doesn’t have to.

It Pays to Understand These Five Investments

One main reason that people don’t diversify into other asset classes is that they don’t understand other asset classes.

Stocks are easy to understand. Stocks go up, stocks go down—not too hard. It’s a little more complicated than that, but for the time being, let’s assume that stocks are linear instruments.

Bonds are more complex. People don’t like to invest in things they don’t understand. When I was learning to invest, all I knew was that I had to have an allocation to bonds for diversification purposes and that bonds went down when interest rates went up.

Like what you're reading?

Get this free newsletter in your inbox every Thursday! Read our privacy policy here.

Most people don’t spend much time thinking about getting exposure to commodities, but it’s not that hard. You don’t have to open a futures account. Gold is one-stop shopping—an allocation to gold gives you your commodity exposure. But if you’re dissatisfied with that, one of the nice things about the growth of the ETF industry is that you can invest in pretty much any single commodity or basket of commodities in ETF form.

And of course, no asset allocation discussion would be complete without a discussion of cash. Cash is many things. Cash is optionality—it is the option to buy something cheaper in the future. Cash is an asset class in and of itself—it doesn’t return very much, but it is an asset class. And even in a zero-rate environment, there is a pretty strong argument for having it.

Put Them Together and You Get the “Awesome Portfolio”

What I’ve just described is the Awesome Portfolio, an asset allocation model I developed last year.

Over the last 50-odd years, the Awesome Portfolio has pretty much returned the same as stocks—but with just half the volatility.

I was speaking with a friend from Lehman a few months ago, telling him about my Awesome Portfolio idea. He said, “Yeah, that’s pretty much my allocation, and it meant that I was down only about 5% percent during the crisis in March.”

It works because it targets risk instead of returns. In fact, it doesn’t promise returns at all. What it does promise—and deliver—is a manageable level of risk.

In fact, it's designed to let you stay invested and keep compounding in any kind of environment. Click here to discover how.

Investing is all about psychology. If you can defeat your instinct to focus on returns over risk, you will succeed in boosting the former with far less of the latter.

Jared Dillian

subscribers@mauldineconomics.com