Dalio’s Analogue and Mauldin’s Commentary

-

John Mauldin

John Mauldin

- |

- September 6, 2019

- |

- Comments

- |

- View PDF

John Mauldin

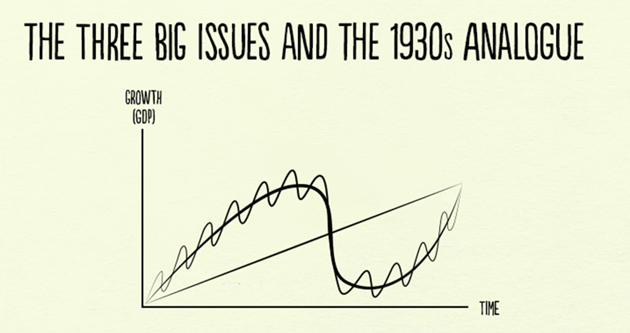

John MauldinThe Three Big Issues and the 1930s Analogue

Survival Advice

A Preview of Next Week

New York and Houston

“The best way out is always through.”

—Robert Frost

“History doesn't repeat itself, but it does rhyme.”

―Mark Twain

It will not shock you when I say we live in confusing times. Odd, seemingly inconsistent events and decisions don’t bring the expected results. Once-reliable rules don’t work. This makes it hard to chart a personal and business path forward.

At the same time, truly nothing is new under the sun. Almost everything we see happened before at some point in human history, though of course with different details and magnitude. So we can’t throw out precedent completely. Well, except for negative interest rates. That really is something new under the sun.

Negative rates are like the event horizon around a black hole. Once you cross the event horizon, all known mathematical models and descriptions of the universe change. Negative interest rates are creating the same chaos in the world as black holes do in space.

That’s why I admire and pay attention to clear, systematic thinkers like Ray Dalio. I don’t agree with everything he says, as you saw a few months ago in my open letters to Ray about his Modern Monetary Theory (MMT) comments. He still observes many of the same problems I do, and is likewise wrestling with how to address them.

Ray’s latest comments, which he posted here on August 28, are critically important to all investors. Everyone should read them. Today I will help by doing something I rarely do: reprint someone else’s entire commentary verbatim.

Below you’ll find Ray’s entire article and I want you to read it all. At the end I’ll add some comments of my own that will extend into next week. Please note, I don’t see a “but” in my comments, but more of an “and” plus a few additional side thoughts.

(Note: I’ve added bold print to highlight some of Ray’s key points. I also broke up some long paragraphs to make it a little more readable, though Ray is admirably clear already.)

As you will see, Ray says our current situation is essentially the reciprocal of the 1970s inflationary blow-off. The last historical parallel to what we now face was the 1930s. Both those analogues, while not perfect, carry valuable lessons we should consider.

As Mark Twain supposedly said, history may not repeat but it does rhyme. The fundamental economic conditions, and especially technology, have changed significantly since the 1930s but human reactions and motivations are still pretty much the same. Which is what worries me…

I’ll stop there before I steal too much of Ray’s thunder. Read on and I’ll see you below.

The Three Big Issues and the 1930s Analogue

By Ray Dalio, Bridgewater Associates, August 28, 2019

The most important forces that now exist are:

1) The End of the Long-Term Debt Cycle (When Central Banks Are No Longer Effective)

+

2) The Large Wealth Gap and Political Polarity

+

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

3) A Rising World Power Challenging an Existing World Power

=

The Bond Blow-Off, Rising Gold Prices, and the Late 1930s Analogue

In other words now 1) central banks have limited ability to stimulate, 2) there is large wealth and political polarity and 3) there is a conflict between China as a rising power and the US as an existing world power. If/when there is an economic downturn, that will produce serious problems in ways that are analogous to the ways that the confluence of those three influences produced serious problems in the late 1930s.

Before I get into the meat of what I hope to convey, I will repeat my simple timeless and universal template for understanding and anticipating what is happening in the economy and markets.

My Template

There are four important influences that drive economies and markets:

- Productivity

- The short-term debt/business cycle

- The long-term debt cycle

- Politics (within countries and between countries).

There are three equilibriums:

- Debt growth is in line with the income growth required to service the debt,

- The economy’s operating rate is neither too high (because that will produce unacceptable inflation and inefficiencies) nor too low (because economically depressed levels of activity will produce unacceptable pain and political changes), and

- The projected returns of cash are below the projected returns of bonds, which are below the projected returns of equities and the projected returns of other “risky assets.”

And there are two levers that the government has to try to bring things into equilibrium:

- Monetary policy

- Fiscal policy

The equilibriums move around in relation to each other to produce changes in each like a perpetual motion machine, simultaneously trying to find their equilibrium level. When there are big deviations from one or more of the equilibriums, the forces and policy levers react in ways that one can pretty much expect in order to move them toward their equilibriums.

For example, when growth and inflation fall to lower than the desired equilibrium levels, central banks will ease monetary policies which lowers the short-term interest rate relative to expected bond returns, expected returns on equities, and expected inflation. Expected bond returns, equity returns, and inflation themselves change in response to changes in expected conditions (e.g. if expected growth is falling, bond yields will fall and stock prices will fall).

These price changes happen until debt and spending growth pick up to shift growth and inflation back toward inflation. And of course all this affects politics (because political changes will happen if the equilibriums get too far out of line), which affects fiscal and monetary policy. More simply and most importantly said, the central bank has the stimulant which can be injected or withdrawn and cause these things to change most quickly.

Fiscal policy, which changes taxes and spending in politically motivated ways, can also be changed to be more stimulative or less stimulative in response to what is needed but that happens in lagging and highly inefficient ways.

For a simpler explanation of this template see my 30-minute animated video “How the Economic Machine Works” and for a more comprehensive explanation see my book Understanding the Principles of Big Debt Crises, which is available free as a PDF here or in print on Amazon. Also, to learn more about our extensive debt cycle research, please visit our debt crises research library on Bridgewater.com.

Looking at What Is Happening Now in the Context of That Template

Regarding the above template and where we are now, in my opinion, the most important things that are happening (which last happened in the late 1930s) are

a) we are approaching the ends of both the short-term and long-term debt cycles in the world’s three major reserve currencies, while

b) the debt and non-debt obligations (e.g. healthcare and pensions) that are coming at us are larger than the incomes that are required to fund them,

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

c) large wealth and political gaps are producing political conflicts within countries that are characterized by larger and more extreme levels of internal conflicts between the rich and the poor and between capitalists and socialists,

d) external politics is driven by the rising of an emerging power (China) to challenge the existing world power (the US), which is leading to a more extreme external conflict and will eventually lead to a change in the world order, and [Ian Bremmer calls this the return of a bi-polar world but with significant differences in the goals of the powers—JM]

e) the excess expected returns of bonds is compressing relative to the returns on the cash rates central banks are providing.

As for monetary policy and fiscal policy responses, it seems to me that we are classically in the late stages of the long-term debt cycle when central banks’ power to ease in order to reverse an economic downturn is coming to an end because:

- Monetary Policy 1 (i.e. the ability to lower interest rates) doesn’t work effectively because interest rates get so low that lowering them enough to stimulate growth doesn’t work well,

- Monetary Policy 2 (i.e. printing money and buying financial assets) doesn’t work well because that doesn’t produce adequate credit in the real economy (as distinct from credit growth to leverage up investment assets), so there is “pushing on a string.” That creates the need for…

- Monetary Policy 3 (large budget deficits and monetizing of them) which is problematic especially in this highly politicized and undisciplined environment.

More specifically, central bank policies will push short-term and long-term real and nominal interest rates very low and print money to buy financial assets because they will need to set short-term interest rates as low as possible due to the large debt and other obligations (e.g. pensions and healthcare obligations) that are coming due and because of weakness in the economy and low inflation.

Their hope will be that doing so will drive the expected returns of cash below the expected returns of bonds, but that won’t work well because:

a) these rates are too close to their floors,

b) there is a weakening in growth and inflation expectations which is also lowering the expected returns of equities,

c) real rates need to go very low because of the large debt and other obligations coming due, and

d) the purchases of financial assets by central banks stays in the hands of investors rather than trickles down to most of the economy (which worsens the wealth gap and the populist political responses).

This has happened at a time when investors have become increasingly leveraged long due to the low interest rates and their increased liquidity. As a result we see the market driving down short-term rates while central banks are also turning more toward long-term interest rate and yield curve controls, just as they did from the late 1930s through most of the 1940s.

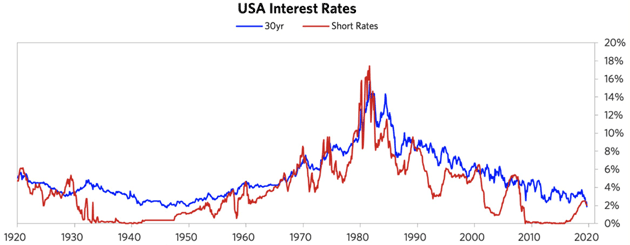

To put this interest rate situation in perspective, see the long-term debt/interest rate wave in the following chart. As shown below, there was a big inflationary blow-off that drove interest rates into a blow-off in 1980–82. During that period, Paul Volcker raised real and nominal interest rates to what were called the highest levels “since the birth of Jesus Christ,” which caused the reversal.

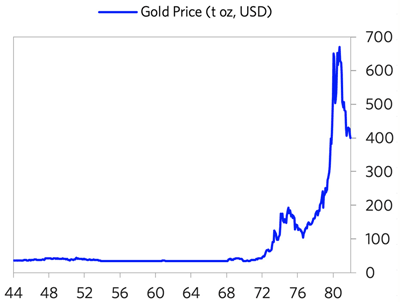

During the period leading into the 1980–82 peak, we saw the blow-off in gold. The below chart shows the gold price from 1944 (near the end of the war and the beginning of the Bretton Woods monetary system) into the 1980–82 period (the end of the inflationary blow-off). Note that the bull move in gold began in 1971, when the Bretton Woods monetary system that linked the dollar to gold broke down and was replaced by the current fiat monetary system. The de-linking of the dollar from gold set off that big move. During the resulting inflationary/gold blow-off, there was the big bear move in bonds that reversed with the extremely tight monetary policies of 1979–82.

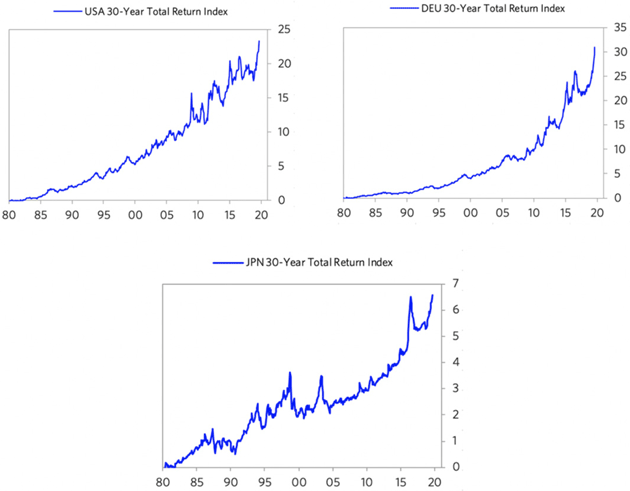

Since then, we have had a mirror-like symmetrical reversal (a dis/deflationary blow-off). Look at the current inflation rates at the current cyclical peaks (i.e. not much inflation despite the world economy and financial markets being near a peak and despite all the central banks’ money printing) and imagine what they will be at the next cyclical lows. That is because there are strong deflationary forces at work as productive capacity has increased greatly. These forces are creating the need for extremely loose monetary policies that are forcing central banks to drive interest rates to such low levels and will lead to enormous deficits that are monetized, which is creating the blow-off in bonds that is the reciprocal of the 1980–82 blow-off in gold. The charts below show the 30-year T-bond returns from that 1980–82 period until now, which highlight the blow-off in bonds.

To understand the current period, I recommend that you understand the workings of the 1935–45 period closely, which is the last time similar forces were at work to produce a similar dynamic.

Please understand that I’m not saying that the past is prologue in an identical way. What I am saying that the basic cause/effect relationships are analogous:

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

a) approaching the ends of the short-term and long-term debt cycles, while

b) the internal politics is driven by large wealth and political gaps, which are producing large internal conflicts between the rich and the poor and between capitalists and socialists, and

c) the external political conflict that is driven by the rising of an emerging power to challenge the existing world power, leading to significant external conflict that eventually leads to a change in the world order.

As a result, there is a lot to be learned by understanding the mechanics of what happened then (and in other analogous times before then) in order to understand the mechanics of what is happening now. It is also worth understanding how paradigm shifts work and how to diversify well to protect oneself against them.

(End Dalio quote)

Survival Advice

John here again. I’ll have more to say on Ray’s analogies next week. First, I want to draw your attention to his last sentence.

It is also worth understanding how paradigm shifts work and how to diversify well to protect oneself against them.

Reading such articles can leave you gloomy and maybe even in despair. Knowing with the benefit of hindsight how bad the 1930s were, the prospect of re-living them is discouraging.

To that, I have two responses.

First, those who went through the Great Depression and World War II didn’t know the whole story as we do now. They faced those challenges one day at a time, and (mostly) made it through.

Second, we know the stories precisely because people lived to recount them. They were bad, yes. They were not universally fatal or irreversibly destructive. People and businesses got back on their feet. Nations and economies recovered, and ultimately built the world we now fear will disappear. It won’t. We will get through this time, just as our ancestors made it through their own challenges.

The coming difficult times will be somewhat less difficult if we recognize them for what they are, and prepare accordingly. That is what I’m trying to do, I suggest you do likewise.

I headed this letter with a quote from Robert Frost: “The best way out is always through.” It comes from his 1915 poem A Servant to Servants. It describes the loneliness of a woman burdened with menial tasks, unable to reach her dreams.

We all have tasks that may seem menial, and we all have dreams, too. They are on the other side of our present challenges. To reach them, we have to go through. That’s easier when you aren’t alone… and as long as I can write, you won’t be.

A Preview of Next Week

Because I really do try to keep a fairly strict word count for each letter, and because we are closing in on it, I won’t try to make a full commentary yet. But next week we will look at:

- I think an additional force will gain importance in the next decade: the spread of new technologies. Ray similarly talks about technology, but I think what I call “the Age of Transformation” will profoundly change how society organizes itself. Much of our identity is associated with what we do—our work and our roles in life. For many of us, that is going to change significantly.

- I agree with Ray that interest rates will drop very low. If I could somehow get the Fed’s attention, I would tell them to take short-term rates to 1% but no lower. The difference between 25 basis points and 1% is nil in the grand scheme of things, and that 1% is important to people who need income to live on. Interest-rate manipulation that pushes the lower bounds is every bit as debilitating as taxes and regulations. It reduces the income available to retirees and savers, and thereby reduces consumption and growth. I can make a long list of bad things interest rate manipulation does.

- Unlike our parents, the Boomer Generation will have to look beyond bonds and CDs to generate income. Fortunately there are ways to do that, which we will discuss next week. The sad news is many of my fellow Boomers will think they have to own stocks in order to get the returns they need to retire. They will buy at precisely the wrong time and see a large part of their retirement savings wiped out. Retirement is a time to invest conservatively, not seek risk and stretch for yield in ever-riskier bonds.

- The environment Ray describes will devastate the normal 60/40 investor. But those willing to think outside the box will have numerous opportunities that compare favorably with past equity returns. We will have to consider less traditional avenues.

New York and Houston

I had an extraordinarily interesting, profitable, and fun meeting with Jim Mellon of Juvenescence at the Miami airport, and then quickly traveled up to Fort Lauderdale to meet with fixed income genius Mark Grant, whom you can often see on Fox Business and CNBC. He was an extraordinary host and his “Three Fuzzballs” (rescued Australian collies) were extraordinarily intelligent and fun.

Mark had to call four restaurants to find one that was open, as many had closed in anticipation of Dorian. We had dinner at Morton’s, which would normally be packed to the gills, and almost had it to ourselves. We talked long into the night—which for Mark was about 9:30 pm as he begins his days around 3:30 am.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

We talked a lot about how to generate income in a very low-rate environment. I have had many such conversations lately with various experts. I’m quite encouraged about the potential for my readers and clients to earn reasonable returns in an otherwise difficult market. More later…

I will go to New York and Houston this month. I am having to learn that American Airlines is not the only way to fly. While American flies from Puerto Rico to many cities, they strangely don’t fly to New York. Given the large Puerto Rican population there, I can only assume it must be some legal difficulty.

And with that I will hit the send button. I know from reader comments that some people think I am all gloom and doom, but I think I’m the most optimistic man in the room. I believe the world will be massively better in the 2030s. I get why people are skeptical. I see it on their faces when I talk about the future. But I am telling you, it will be better than anything you can imagine. Of course, the 2020s are going to be more than a tad bumpy, but we can get through it together.

Have a great week, and find some friends that are part of your tribe so we can all get through it together.

Your thinking about the importance of tribes analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.