Living in a Free-Lunch World

-

John Mauldin

John Mauldin

- |

- March 28, 2015

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinNobody Understands Debt

Foundational Presuppositions

Debt Is Money We Owe to Ourselves – Sort of

There Ain’t No Such Thing as a Free Lunch

Mrs. Watanabe’s Bonds

Home Gearing Up for SIC

“Everyone is a prisoner of his own experiences. No one can eliminate prejudices – just recognize them.”

– Edward R. Murrow, US broadcast journalist & newscaster (1908 – 1965), television broadcast, December 31, 1955

“High debt levels, whether in the public or private sector, have historically placed a drag on growth and raised the risk of financial crises that spark deep economic recessions.”

– The McKinsey Institute, “Debt and (not much) Deleveraging”

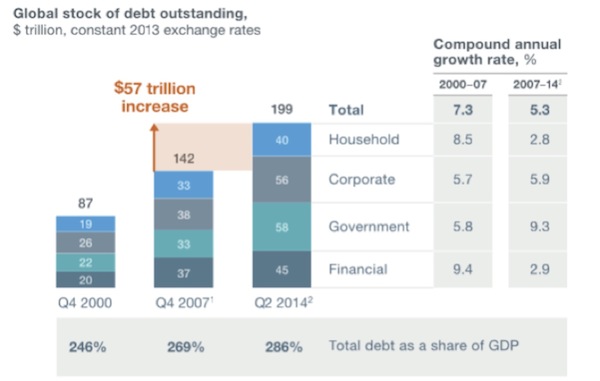

The world has been on a debt binge, increasing total global debt more in the last seven years following the financial crisis than in the remarkable global boom of the previous seven years (2000-2007)! This explosion of debt has occurred in all 22 “advanced” economies, often increasing the debt level by more than 50% of GDP. Consumer debt has increased in all but four countries: the US, the UK, Spain, and Ireland (what these four have in common: housing bubbles). Alarmingly, China’s debt has quadrupled since 2007. The recent report from the McKinsey Institute, cited above, says that six countries have reached levels of unsustainable debt that will require nonconventional methods to reduce it (methods otherwise known as defaulting, monetization; whatever you want to call those measures, they amount to real pain for the debtors, who are in many cases those least able to bear that pain). It’s not just Greece anymore. Quoting from the report:

Seven years after the bursting of a global credit bubble resulted in the worst financial crisis since the Great Depression, debt continues to grow. In fact, rather than reducing indebtedness, or deleveraging, all major economies today have higher levels of borrowing relative to GDP than they did in 2007. Global debt in these years has grown by $57 trillion, raising the ratio of debt to GDP by 17 percentage points (see chart below). That poses new risks to financial stability and may undermine global economic growth.

This report was underscored by a rather alarming, academically oriented paper from the Bank for International Settlements (BIS), “Global dollar credit: links to US monetary policy and leverage.” Long story short, emerging markets have borrowed $9 trillion in dollar-denominated debt, up from $2 trillion a mere 14 years ago. Ambrose Evans-Pritchard did an excellent and thoroughly readable review of the paper a few weeks ago for the Telegraph, summing up its import:

Sitting on the desks of central bank governors and regulators across the world is a scholarly report that spells out the vertiginous scale of global debt in US dollars, and gently hints at the horrors in store as the US Federal Reserve turns off the liquidity spigot….

“It shows how the Fed's zero rates and quantitative easing flooded the emerging world with dollar liquidity in the boom years, overwhelming all defences. This abundance enticed Asian and Latin American companies to borrow like never before in dollars – at real rates near 1pc – storing up a reckoning for the day when the US monetary cycle should turn, as it is now doing with a vengeance.”

Ambrose’s parting takeaway?

[T]he message from a string of Fed governors over recent days is that rate rises cannot be put off much longer, the Atlanta Fed's own Dennis Lockhart among them. ‘All meetings from June onwards should be on the table,’ he said. [This is from a regional president whose own research suggests GDP growth in the first quarter of 1%! – JM]

The most recent Fed minutes cited worries that the flood of capital coming into the US on the back of the stronger dollar is holding down long-term borrowing rates in the US and effectively loosening monetary policy. This makes Fed tightening even more urgent, in their view, implying a ‘higher path’ for coming rate rises.

Nobody should count on a Fed reprieve this time. The world must take its punishment.

Ouch! Please sir, may I have another? Punishment indeed. Ask the Greeks. Or the Spanish. Or… perhaps there is punishment coming soon to a country near you!

I began a series on debt a few weeks ago, and we return to that topic today. I believe the fundamental imbalances we are seeing in the world (highlighted in the two papers mentioned above) are the result of the massive increases in global debt and misunderstandings about the use and consequences of debt. Too much of the wrong kind of debt is going to be the central cause of the next investment crisis. As I highlighted in my February 24 letter, the right type of debt can be beneficial. However, as the McKinsey Report emphasizes,

High debt levels, whether in the public or private sector, have historically placed a drag on growth and raised the risk of financial crises that spark deep economic recessions.

Read that again. This isn’t the Mises Institute. This is #$%%*# McKinsey. As establishment as it gets. And they are clearly echoed by the BIS, the central banker’s central bank. Unless this time is different, they are saying, the high levels of debt are the reason for slowed growth in the developed world, a point we have highlighted for years in our research. There is a point at which too much debt simply sucks the life out of an economy.

A useful starting point for today’s letter is Paul Krugman’s lament that “Nobody understands debt.” But to borrow a phrase from Bill Clinton, it really depends on what your definition of “debt” is.

Paul Krugman has actually written two New York Times columns entitled “Nobody Understands Debt.” The first, and more nuanced, one was published on January 1, 2012; and the second one appeared last month (on February 9). It is a constant theme for him. If you want a short take on what at an uber-Keynesian believes on debt, these columns are a good place to start. (Paul [may I call him Paul?] is as good a representative of the neo-Keynesian species – Homo neo-keynesianis – as there is, an interesting subset of the human genus.) In our musings on debt, we are going to look at these two essays in the effort to understand the differences between those who want more government spending and increases in debt and those who favor what is now disparagingly referred to as austerity.

I choose Krugman not because of any need to disparage him (he does write some rather good essays) but because he writes remarkably clearly for an economist, he has an extensive body of public work to choose from, and he says many things about debt that I think everyone can agree with. The differences between his positions and mine can, however, be pronounced; and I have spent some time trying to discern why reasonably intelligent people can have such significant disagreements. My goal here is to be respectful and gentlemanly while trying to expose the foundations (there is a pun here, soon to be revealed) of our disagreement.

To do this, we are now going to step out of the economic realm and move a little farther afield. Some readers may wonder at the journey I am am about to take you on, but this diversion will be helpful in explaining Paul’s and my different approaches to debt. We’ll return to our central theme by and by. Stick with me.

One of the things I learned in my religious studies (yes, I did attend – and graduate from – seminary as penance for what must have been multiple heinous sins in my past lives) is that disagreements are often driven not by the “logic path” of an individual’s thoughts but instead by their core presuppositions. Presuppositions are often more akin to tenets of faith and insight than they are to actual, provable observations or facts. They are things assumed to be true beforehand, ideas taken for granted. Sometimes our presuppositions are rooted in prejudice, but more often than not they just arise from normal human behavior. Often, presuppositions are formed because of beliefs stemming from other areas of our lives or imposed by society. Your basic presuppositions, what “everyone” knows to be true, can lead to absurd conclusions. If you believe, as people did in Galileo’s day believed, that the Bible teaches the earth is flat and that the Bible is the authoritative source for understanding physical geography along with everything else, then it is logical to believe you can sail off the end of the Earth.

We are, as the great journalist Edward R. Murrow said, “prisoners of our own experiences.”

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Presuppositions (we all have them) are at the heart of all sorts of irrational behavior that we are learning about from the growing understanding of behavioral economics. Not only can we demonstrate that humans are irrational, we are predictably irrational. That irrationality was actually bred into us when we were a young species, dodging lions and chasing antelopes on the African savanna. But what were useful survival traits two million years ago can now be problematic in modern society. Our presuppositions can lead us to errors in investing and cause all sorts of societal problems. Bluntly put, presuppositions can come seemingly out of nowhere and bite you on the ass.

Presumably, if two people start with the same presuppositions, then logic and reasoning should allow them to come to agreement about their conclusions. (Yes, I know, it’s not quite that simple, but I don’t want to write a book on presuppositionalism here. Van Til did that, and it is unreadable. So work with me.)

Long-time readers know that I also send out a weekly letter called Outside the Box. It features the work of other writers I find interesting. I often send out material that I don’t necessarily agree with but that makes us think. If you can’t read something you disagree with and know why you logically disagree, then maybe you need to examine your own presuppositions and possibly arrive at different conclusions.

I think the difference that Mr. Krugman and I have on debt basically comes down to our presuppositions. I suspect they impact other aspects of our lives similarly. Like me, Mr. Krugman grew up on science fiction and still keeps up. He credits reading science fiction as a youth with his ultimate choice of economics as a career. In a very real sense, so do I. But I was more influenced by Lazarus Long (a recurring character in the books of Robert Heinlein) than Hari Selden (the genius who saves the galaxy in Isaac Asimov’s brilliant Foundation series.) The former is distrustful of government, while the latter assumes that humanity is better off with a few brilliant people running the show, if behind the scenes. (I say “people,” but after following the exploits of Hari Selden for a few decades, we learn that the real masters are technocratic robots.)

While I agree with Krugman that the Foundation trilogy may be the finest science fiction books ever written (and still highly recommend them to anyone wanting to jump into science fiction), they are a poor manual for the organization of government.

Two years ago Krugman wrote this about Asimov’s trilogy: “My Book – the one that has stayed with me for four-and-a-half decades – is Isaac Asimov's Foundation Trilogy, written when Asimov was barely out of his teens himself. I didn't grow up wanting to be a square-jawed individualist or join a heroic quest; I grew up wanting to be Hari Seldon, using my understanding of the mathematics of human behaviour to save civilisation.” (This is an excellent review, by the way, and I encourage those who are interested to read it.)

Am I cooking up a simplistic analogy? Perhaps not, since our presuppositions actually show up in our views on economics. It is Hayek versus Keynes (though admittedly you get better writing and plot lines when you read Asimov and Heinlein than you do when you peruse our economic giants). Asimov, as my friend (and Science Fiction Hall of Fame writer) David Brin wrote,

… was quite liberal and progressive. His Robots universe, however, kept toying with notions of technocracy – a concept of his youth – in which the best and brightest over-rule the hot-tempered and irrational masses…. [H]is fiction cycled around an ambivalence about humans’ ability to govern themselves with foresight and wisdom.

Heinlein, on the other hand, would be called a libertarian in today’s world. He was committed to absolute freedom and individual responsibility mixed in with patriotism, mixed in with some personal eccentricity.

(David Brin is one of the world’s true experts on Heinlein and Asimov and knew them both well. He told me in a recent conversation that they each recognized the weaknesses in the philosophies that underpinned their created worlds, if those worlds are taken to their logical conclusion. Ironically, in their novels, both authors end up espousing a sort of neofeudalism. Asimov, however, became very uncomfortable later in life with the technocratic, omnipresent government that dominated the Foundation Trilogy.)

The fundamental difference in Asimov’s and Heinlein’s views, and in the views of Keynes and Hayek, is the power of individuals and markets versus the power and influence of government. So let’s take a look at some of Mr. Krugman’s views on debt; and then you can see whether you agree with his assumptions and in general with Keynes and much of academic economics today, or with Hayek. This topic may take a few weeks to cover fully, but it’s important. Your assumptions about how the world works will translate into investment decisions. Ideas have consequences, and nothing is more fundamental to the way you interface with the world of macroeconomics today than your views on debt.

Debt Is Money We Owe to Ourselves – Sort of

“High debt levels, whether in the public or private sector, have historically placed a drag on growth and raised the risk of financial crises that spark deep economic recessions.”

– The McKinsey Institute, “Debt and (not much) deleveraging”

I rather suspect that Paul Krugman would take issue with the statement above, given his column of February 6, 2015, entitled “Debt Is Money We Owe To Ourselves.” Let’s look at his first couple of paragraphs:

Antonio Fatas, commenting on recent work on deleveraging or the lack thereof, emphasizes one of my favorite points: no, debt does not mean that we’re stealing from future generations. Globally, and for the most part even within countries, a rise in debt isn’t an indication that we’re living beyond our means, because as Fatas puts it, one person’s debt is another person’s asset; or as I equivalently put it, debt is money we owe to ourselves – an obviously true statement that, I have discovered, has the power to induce blinding rage in many people.

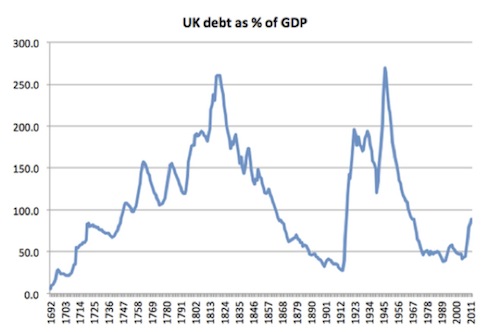

Think about the history shown in the chart above. Britain did not emerge impoverished from the Napoleonic Wars; the government ended up with a lot of debt, but the counterpart of this debt was that the British propertied classes owned a lot of consols.

Consols are a type of British government bond that are perpetual in nature, in that they are interest-only bonds. They were first issued in 1751 and eventually financed the Napoleonic wars. There are multiple other instances where governments amassed large amounts of debt to finance wars and were able to pay the debt down over time. Think the US after the Civil War and World War II. Proponents of such massive government debt issuance will point out that growth was not constrained in 19th century Britain or after the Civil War or World War II in the US.

Krugman contends that “the problems with public debt are also mainly about possible instability rather than ‘borrowing from our children’.” He completely dismisses this latter idea as nonsensical rhetoric (his words).

So, do historically high levels of debt drag down growth, as McKinsey and the Bank of International Settlements assert, or do they not? In general, I think they do, but I would agree that sometimes it depends on the type of debt and the situation. Certainly you can find examples where nations took on huge debts and there was still adequate growth in the wake of doing so. But in the overwhelming preponderance of cases, when governments and/or the private sector have taken on too much debt, there has not only been a drag on growth, there have also been devastating financial crises and deep recessions or depressions.

As I tried to make clear in the last letter, not all debt is bad. There are times when debt can be actually quite productive, whether it is personal or governmental debt. But the issue hinges on the difference between good debt and bad debt and on who owes debt to whom.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Very simply, “bad debt” is debt, whether private or public, that cannot be repaid from current cash flows. All debt is “good” until the moment it is defaulted upon (both legally and realistically).

Further, it is intuitively obvious that if a country or company is using current cash flows to repay debt that was incurred for nonproductive purposes, that limits its ability to use that cash for other purposes. Assuming the other purposes are important to further growth, then growth is constrained, and options are reduced.

If taxes must be increased to pay off the debt, that limits the cash available to finance further private-sector growth, which is far and away the largest source of growth for the economy. Only if you contend that government spending per se and in general is an engine of growth can you argue that it makes no difference whether spending is public or private.

While certain types of government spending are conducive to growth (think infrastructure development, education, scientific research, and law enforcement as examples), only a small portion of US federal government spending falls into those categories; so the preponderance of federal spending does not enhance productivity. I think the bulk of academic research supports that conclusion. That is not to say that some government expenditures for nonproductive uses are not proper or necessary, but that’s a different argument for a different day. (A social safety net comes to mind.)

You can’t contend that there is not a cost, in terms of private-sector productivity, incurred by taxes. That is not saying that a particular tax expenditure may not be worth the cost. Some government expenses are vital to public well-being and to a stable, properly functioning economy. Just be clear that there is always a cost. The negative slope of the curve when growth is plotted against taxation rates is quite clear. At some point, high overall taxes and high debt become a drag on growth (in terms of GDP, not effects on individuals, although you can make that argument). Think Europe. And Japan.

Most periods of high government debt that were not a drag on growth followed wars, when previously massive defense spending was radically decreased and the resulting extra income was then used to reduce the debt. Further, wars are the epitome of nonproductive spending, even when they are necessary for survival. A cessation of hostilities and the returning of soldiers to productive activities will in and of itself increase productivity and GDP, and that growth in turn increases the ability of an economy to pay back debt! That scenario is significantly different from a period where government debt, incurred to fund current consumption, is allowed to increase beyond the ability of cash flows to pay off the debt.

Greece is now in the latter situation. Rogoff and Reinhart detail over 260 other such episodes in history, where countries incurred insupportable debt and were forced to default in one manner or another. Default can take several different forms: deferral, restructuring of the terms to the detriment of the creditor, outright refusal or the inability to pay, etc. Monetization is a form of default that we will deal with shortly. From the point of view of the creditor, if you have to change the terms in such a way that you get less than you originally bargained for, even if that is the best outcome under the current circumstances, you will now have less money than you expected to have. You can call it what you like, give it all sorts of pretty names, but it means that a debtor did not live up to the terms originally agreed upon.

It is time to take up the question of whether government debt is just money we owe to ourselves. Let’s take a real-world example of a nation that has incurred a very large debt that it increasingly struggles to make payments on and yet essentially owes the money to itself. I refer to Japan.

Japan has amassed a debt that is roughly 250% of GDP, far higher than that of any other country. The government has been able to grow such an outsized debt precisely because its citizens have, either directly or indirectly through their pension funds, been willing to purchase that debt. It is estimated that up to 95% of Japanese bonds are owned by the Japanese themselves (directly or through institutions). The rest is primarily in the steady hands of other central banks and a few funds with position mandates.

There is no country anywhere that can truly be said to owe more “to themselves” than Japan does. To sort out whether debt that we owe to ourselves is truly not a problem, let’s drop in at the home of the proverbial Mrs. Watanabe, who, it just so happens, is being paid a courtesy visit by Prime Minister Shinzo Abe and Bank of Japan Governor Haruhiko Kuroda. Let’s listen in:

Kuroda [bowing]: Mrs. Watanabe, we are here today because we have a national crisis. Previous Japanese governments have run up a rather large debt, and we find ourselves in the unfortunate position of not being able to repay that debt unless we monetize it. But since we owe that money to ourselves, and since you are us, we thought we might ask if you, along with all your neighbors and friends, would be willing to forgo payment so that we can reduce the national debt. We realize this will make things more difficult for you in your remaining years, but it really is for the good of the nation.

Abe: Can we count on your support? And of course we would like you to vote for us in the next election.

Mrs. Watanabe: Honorable Prime Minister, my husband and I have worked very hard all our lives. We have done exactly as good Japanese citizens should do. We saved our money, invested in government bonds, and now we’re depending on them for our retirement. We need those bonds to be paid in full in order to have enough to buy our rice and miso soup and sake. In fact, listening to what you say, I think I need a cup of sake to calm me down. Pardon me for a moment.

[Mrs. Watanabe serves sake to her esteemed guests, takes a stiff gulp herself, then stands and draws a deep breath, bows, and looks the Prime Minister in the eye.] Let me be very clear. I fully expect to be able to cash in my bonds when I need the money. Further, I expect my pension to be paid in full in exactly the manner I was promised. If your administration cannot fulfill those promises without endangering my life, then I and my many friends will make sure that you are not allowed to continue in public office. Good day, gentlemen.

Now I know that is not the way the conversation would actually go. Mrs. Watanabe is a very polite Japanese lady who would never speak so directly to her Prime Minister. Nevertheless, I suspect my version of the conversation has captured the gist of what she was actually thinking.

And of course Abe-sama and Kuroda-sama know better than to ever have that conversation, because that is essentially the reaction they would expect to get from their citizens. In fact, a survey conducted a few years ago confirmed that less than 13% of Japanese citizens would be willing to sacrifice for the good of the nation when it came to their government bonds. So much for Japanese solidarity.

So Abe has had to choose between Disaster A and Disaster B. Rather than suffer a deflationary collapse, Disaster A, he has chosen Disaster B, the monetization of his debt. Which is precisely what Professors Krugman and Bernanke have suggested that Japan should do, although under the guise of quantitative easing, with the aim of creating inflation. So now Japan is experimenting with the most monumental quantitative easing ever undertaken by any developed country in the history of the world.

So how’s that quantitative easing thingy working out for Japan? Inflation should be going through the roof by now, right? Well, not so much.

Japan's annual core consumer inflation ground to a halt in February, the first time it has stopped rising in nearly two years, keeping the central bank under pressure to expand monetary stimulus later this year. Other data published on Friday didn't offer much solace with household spending slumping [2.9% y-o-y, for 11 straight months of decline] even as job markets improved, underscoring the challenges premier Shinzo Abe faces in steering the economy toward a solid recovery.

While the Bank of Japan has stressed it will look through the effect of slumping oil prices, the soft data will keep it under pressure to expand stimulus to jump-start inflation toward its 2 percent target.” (Reuters, March 27)

Aside from not being able to generate inflation, the Japanese economy is doing as well as can be expected and better than it has in most of the past 25 years. But the Japanese government desperately needs 2% inflation and 2% real growth in order to be able to deal with its debt, if it is not to be forced into outright monetization.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

So the economy is doing kind of all right, and Japanese quantitative easing has been a roaring success, right? Perhaps from the perspective of the Japanese elite, its politicians, and of course its economists, but not, perhaps, from the perspective of Mrs. Watanabe.

She has seen the purchasing power of her currency drop by 33% in the past few years. That massive hit on her spending power affects her directly when she goes to buy imported goods, and it affects her indirectly through the high cost of all the energy Japan must import. When your buying power is reduced in retirement – and Japan has a rapidly aging population – I don’t think you can call that a roaring success.

The truth is, the Japanese government is passing on the pain of 25 years of running up too much debt to Japanese savers and retirees. I think the value of the yen is likely to drop another 50% (at least) before Japan can allow the market to set interest rates. They are going to print more money than any of us can possibly imagine. (I have documented on numerous occasions why Japan cannot allow interest rates to rise. Higher rates would be an utter disaster for the country.)

Quantitative easing seems like a Free Lunch World to many politicians and even to many economists, who should know better. But it is not a free lunch for Mrs. Watanabe. It is her lunch, scarfed from her table. And it will not be a free lunch that’s served in Europe as Mario Draghi eases and European savers watch the yield of their bonds and the value of their currency erode.

There Ain’t No Such Thing as a Free Lunch

There ain’t no such thing as a free lunch (TANSTAAFL). Quantitative easing comes with a price. The question is, who will pay it? The unprecedented financial repression that we are seeing in the world has been foisting the cost of bailing out bankers and stock market investors onto the aching, sagging backs of savers and retirees. Some might consider that an acceptable outcome, given that the global financial system has recovered, after a fashion, from the Great Recession.

But Paul Krugman and his neo-Keynesian colleagues, including most central bankers, seem to think they’re living in a free-lunch world. They are either not aware or do not care who is picking up the check.

No matter how debt is reconciled, whether through the normal means of it being paid back or through some type of default, workout, or monetization, someone ends up paying. Oftentimes, there is simply no choice but to resort to some type of debt reconciliation. You can’t squeeze blood from a turnip, especially a Greek turnip. (Another pithy economic lesson I learned from my dad.)

Which leads us to a topic we will take up in a future letter if not next week: how much debt is too much, and how do we avoid getting to that point? Stay tuned.

(Trivia: The maxim “There ain’t no such thing as a free lunch” dates back to the 1930s. The phrase and its acronym are central to Robert Heinlein's 1966 science fiction novel The Moon Is a Harsh Mistress, which helped to popularize it. The free-market economist Milton Friedman also used the phrase as the title of a 1975 book, and it shows up in economics literature to describe opportunity cost.)

Surprisingly, other than a few personal day trips here and there, I am home for the next month until I leave for San Diego for my Strategic Investment Conference. You really should consider coming, as this is the single best macroeconomic conference in the country. I say that without reservation. Find me a conference lineup that it is better at any price. If I listed just the people we have lined up to moderate the question-and-answer sessions, they would constitute a fabulous conference in their own right. I am simply thrilled by the massive intellectual firepower that is going to be in the room. Plus, we just finalized Peter Diamandis to speak Thursday night. My friends and Hall of Fame science fiction writers David Brin and Vernor Vinge, two of the best futurists on the planet, will be there to ask Peter questions and to push back, and they will all mingle with you before dinner. You really don’t want to miss it. The conference is April 29 through May 2. There are just a few places left.

It’s time to hit the send button. I am truly interested in your comments, positive or negative, on this letter in particular, as I hope to develop it into a longer piece on debt. I always read the comments you post beneath the letter on our website. Have a great week!

Your admittedly eccentric analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.