What I Learned at Camp Kotok

-

John Mauldin

John Mauldin

- |

- August 16, 2019

- |

- Comments

- |

- View PDF

John Mauldin

John Mauldin“Don’t Look Back. Something Might Be Gaining on You.”

MMT or the Magic Money Tree

A Fundamental Change in the US/China Relationship

Bone-Penetrating Exhaustion

Montana and Back to Puerto Rico

I am back from my 14th annual Maine fishing camp and the mood was decidedly different this year. The private event at Leen’s Lodge is generally called Camp Kotok in honor of David Kotok of Cumberland Advisors who started these outings many years ago. CNBC and others began calling it the “Shadow Fed” but it is really just a meeting of wickedly smart people focused on economics and markets. (I am allowed to attend for comic relief.) Throw in a little fishing, more fabulous food and wine than anyone should consume, formal debates and informal Q&A, and it really is one of the highlights of my year.

All this happens at a fishing lodge without many luxuries except for the food which is off the charts in the evenings. For lunch, all the boats meet at one spot and the guides cook what we catch in a 2+ hour experience. (Only the hardcore go out fishing afterwards.) The lunch conversations are simply fascinating.

I am still absorbing what I learned, but for me the general mood stood out more. We will get to that below. First, a point of personal privilege.

I first started writing Thoughts from the Frontline in August 2000. That makes this the beginning of my 20th year. I started with 2,000 email addresses from an earlier writing incarnation. I was still writing a print publication which I sold through the mail and thought I would just stick my letter on the internet for free and see what happened. Within two years I had canceled the print letter as the free publication’s growth went through the roof. Even now, I meet people all the time who say they read it from the beginning (or shortly thereafter).

Words cannot express my genuine gratitude that so many of you have read these letters for so long and continue doing so. Simply saying “thank you” doesn’t adequately express how truly, profoundly thankful I am you give me the single most important part of your life—your attention—when we are all so inundated with emails, TV, podcasts, Twitter, Facebook, and other ways to spend our time. The fact that you give some of that precious time to me and my humble musings is emotionally overwhelming.

I sometimes humorously say that each reader is one of my million closest friends, but it’s the truth. I feel you are indeed my friend as you spend your time with me. And my pledge for the next 20 years is the same as the last 20: to give you my unvarnished and true opinion, whatever it may be, as we try to make our way in an ever more volatile, changing world. And while it can’t fully express my feelings, still I say with a full heart (and maybe some moist eyes), “Thank you.”

“Don’t Look Back. Something Might Be Gaining on You.”

That quote is from Satchel Paige (whom my dad played against in Paige’s barnstorming days in the 1930s). It expresses how I felt as I left Leen’s Lodge on Sunday. We discussed the world’s problems and the general mood was that many of those problems are beginning to catch up. Looking back at them simply underscored the frustration and dread.

I missed the Thursday night discussions due to travel “inconveniences,” but thankfully you can read three exceptionally well done takeaways from the meetings, which I shamelessly borrow from David Kotok, Brent Donnelly and Dave Nadig.

This year’s conversations focused on three key long-term themes which were discussed one by one.

- A future where global interest rates remain permanently near zero

- Modern Monetary Theory (MMT) and US fiscal strategy

- A fundamental change in the US/China relationship

Kotok offers a quick introduction:

The 50-person gathering at Leen’s Lodge encompassed diverse political views, financial and economic specialties, and asset classes focused from cannabis to currency trading, real estate to debt of all types, stock markets and ETFs, derivatives and futures, and more. Over $1 trillion in managed assets was represented as we gathered for each informal meal. No lectern, no PowerPoint. The China Panel and the MMT panel are public and in the social media domain and the press and public are free to use the video footage and quote the speakers. Other discussions were conducted under the Chatham House Rule.

Photo: David Kotok

I was not around for the Thursday night survey, when 40 people were asked their opinion of Peter Navarro. One person supported him, three had no opinion, and 36 disapproved. It would have been 37 had I been there. I have said many times that Peter Navarro is the single most dangerous man in the Trump administration. He understands neither trade policy nor trade deficits and yet seems to have a Svengali relationship with the president. I missed that part of the discussion but Kotok summarized:

The damage incurred by Navarro’s advice and Trump’s policy was cataloged in detail, and it is ugly. It is spreading and appearing in more and more evidence and anecdotes.

Border and immigration policies were discussed in detail and with data. The group’s outlook is bleak. Nearly all fault a dysfunctional Congress for its repeated failures. Here the group leaps over partisanship. Democrats and Republicans are guilty.

Mauldin observation: A big majority of a diverse group generally agreed the tariffs were having a global impact, slowing growth elsewhere in ways that will come back to haunt our own shores. Nearly everyone was glad Trump is pushing back on China, but most thought he should do it in another way. (As my friend Gary Halbert asks, why does China still have Most Favored Nation status?) Tariffs hurt Americans. If you want to draw a line, get together with our allies and tell Beijing it needs to stop the intellectual property theft and allow competitors a level playing field or the rest of the world will move on without them. Now that’s getting tough. Hardball? Yes, but I think we are all beginning to realize Chinese leaders are not our friends.

MMT or the Magic Money Tree

There was an open “debate” about MMT or Modern Monetary Theory. Brilliant young man economist Sam Rines took the difficult position of being pro-MMT for the sake of debate. He thinks it would be a disaster but is truly afraid we will actually pursue such a policy. There was the usual pushback, which I’ve written about more than once, but I have to admit that I was struck by the private conversations after the debate. Many smart, well-informed thinkers were almost resigned to seeing MMT actually attempted in the next decade.

Mauldin take away: If we attempt MMT it will end the US dollar’s reserve currency status, produce out-of-control inflation that will essentially destroy the Boomer generation’s ability to retire with anything like most envision today. I can’t say it any stronger. If I really see MMT coming I will reposition my portfolio to heavily weight gold, real estate, and a few biotech companies. I simply can’t imagine a more dire economic scenario.

Honestly, though, I don’t think we will go there. Are there politicians that would like to do it? Absolutely, and they have less economic understanding than God gave a goose. Even economists with whom I strongly disagree on many topics think MMT is not something to be trifled with.

Many participants had read my analysis of the potential for $45 trillion worth of US debt by the end of the 2020s. When I started talking about the potential for $20 trillion of additional quantitative easing, it was clear the question made some uncomfortable.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

There was general agreement that neither political party can balance the budget. The latest “deal” between Trump and Congress raised spending $320 billion over the next two years. The previous “sequester” deal that at least tried to limit spending is out the window. With it will go any control on the spending process. Current deficit projections will seem mild compared to what we actually get.

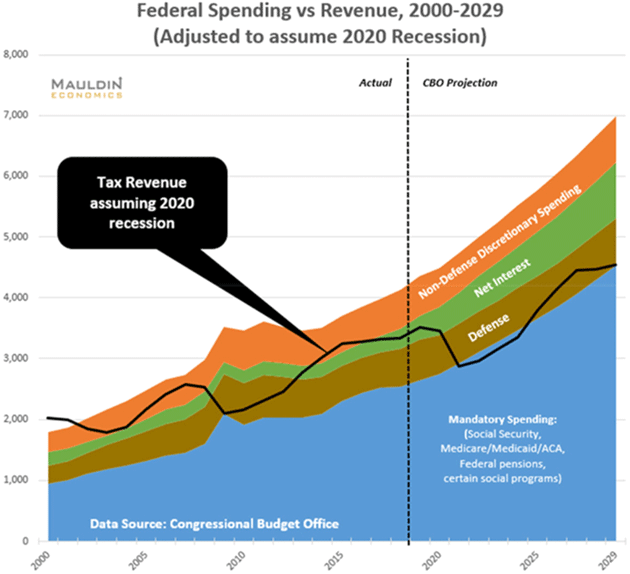

As I said a few weeks ago, using CBO projections from earlier this year and assuming one recession, the national debt would rise to almost $45 trillion by the end of the 2020s. This new deal will add at least another $1.5 to $2 trillion to that amount. If there is a second recession, we would be looking at north of $50 trillion.

We don’t have $40 trillion, let alone $50 trillion, to put into federal debt. It would crowd out all funding for productive private enterprises and sharply reduce GDP growth. Which is why I expect to see massive, currently inconceivable amounts of quantitative easing.

The 2020s will force us to continually think the unthinkable. No, that is probably too mild. We are going to find ourselves having to continually DO the unthinkable.

Doom and gloom? Not really. The math is from the Congressional Budget Office. It is politically impossible for them to project a recession, so they don’t. I would also admit that it is also statistically impossible to predict a recession so they don’t. I don’t have such a restriction.

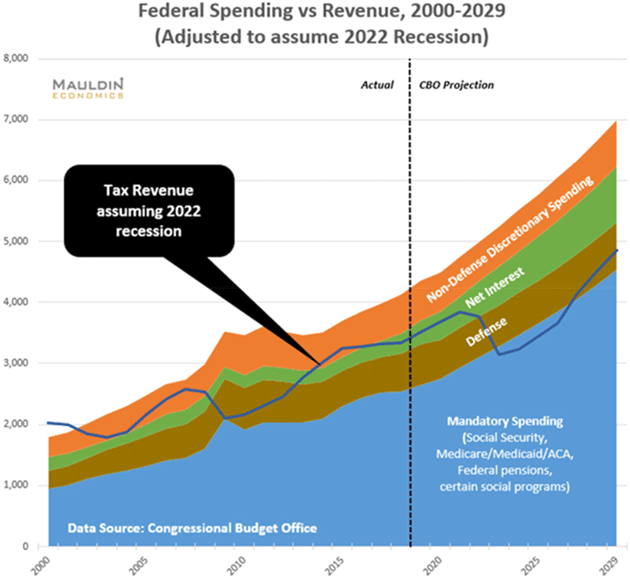

These are the charts that I’ve printed in part four of the discussion with Ray Dalio a few weeks back, assuming recession in either 2020 or 2022. You can see what happens to the deficits and revenues.

This first graph assumes a recession in 2020. Note that revenues fall below mandatory spending by the middle of the decade, then never get back above mandatory spending plus defense spending. Then by the end of the 2020s mandatory spending will again rise to consume all tax revenue. And again, these don’t include significant off-budget spending.

This next graph assumes recession in 2022 instead of 2020. The pattern is basically the same, except that the $2-trillion deficits don’t begin until 2023. Again, this uses actual CBO projections and adjusts revenues by the same percentage they fell in 2008–2009, and recovered thereafter.

I asked one person after another what they thought would happen. How can we avoid this? I got no good answers. Others were clearly just as frustrated as I am. Let me tell you, I am way past frustration. I am seriously worried for the future of the Republic and our children and retirees.

I asked at least a dozen attendees (and maybe more) this question: If we introduce MMT and the result is what we all think it will be, I think there is a 50–50 chance some states will want to secede from the union. Do you agree or disagree?

I got literally no pushback on that admittedly outrageous idea. When you undertake policies that will destroy the very fabric of society in the name of “justice and equality for all,” those damaged in the process will push back.

The debate on MMT had some lighter moments. Everyone chuckled when one panelist called MMT the “Magic Money Tree.” After someone said MMT could be used to fund universal health care and Space Force investments, Jim Bianco (channeling John F. Kennedy) said: “We choose to go to Mars, not because it’s easy, but because it’s free.”

A Fundamental Change in the US/China Relationship

We talked quite a lot about China. Brent Donnelly said this in his Camp Kotok wrap-up:

It was interesting to hear how it now seems to be almost universally accepted that the United States is in a multi-year, multi-front (so far, non-military) war for global supremacy against China. No trade agreement is going to change that. The first challenge to US hegemony since the USSR. Attendees at Camp Kotok run the entire political spectrum but this issue seems almost totally non-partisan.

It was notable how even while many did not agree with the US escalation strategy against China, there was broad agreement that China should be challenged. The China/US long-term decoupling is an issue that will continue post 2020, whoever wins. A rare bipartisan issue.

A good part of the discussion centered around the book “China’s Vision of Victory,” written by Jonathan Ward, one of the attendees. Ward, a US citizen, told remarkable stories of boarding container ships, learning Cantonese and pidgin Indonesian, living in rural and urban China for several years and translating every document publicly released by the Chinese Communist Party to better understand China’s motivations as it rebounds from the Century of Humiliation.

(Sidebar: I personally invited Jonathan Ward at the last minute with Kotok’s permission. He was a big hit at the camp. Read his book.)

Dave Nadig wrote about his question-asking experience:

This year, my question was: "What’s one thing—a risk, a concern, a data point, a situation—that’s really important, that the rest of the econo-finance sphere isn’t paying attention to?”

The answers here were dizzying. While there were a few somewhat predictable answers like, “We’re in a corporate earnings recession and nobody’s talking about it,” there were also some big surprises for me, such as:

- The entire global maritime fleet has to change fuel types in five months, and it’s going to cost a ton.

- The New York PMI (producers manufacturing index) is flashing red lights about the service-based economy.

- Geopolitics is being swept under the rug, leaving us open to a “hot war” while we focus on all the economic wars.

- The risk from Chinese corporates like Huawei is enormous.

- The degradation of the National Weather Service is going to destroy US agriculture.

The list of terrifying one-liners goes on and on.

Nadig and I, along with others, noticed the, for lack of a better term, political fatigue in the room. Normally there would be some passionate discussion, especially when under Chatham House Rules you can’t be quoted. Here’s Nadig again:

This year, the political discussions petered out quite quickly. It wasn’t disinterest that defused things, it was bone-penetrating exhaustion. Even folks I would’ve pegged as the most die-hard partisans seemed to have a hard time mounting a fervent defense of any politician or appointee. The opinions were still there, but the will seemed to have faded.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

I feel the same way. Any thinking about policy for the last few years has been waylaid by a discussion of the people behind the policy.

Bone-Penetrating Exhaustion

That is as good a way as any to describe the mood in the room at the end of Saturday night. Bone-Penetrating Exhaustion. It is like we are staring into an abyss, it’s a long way down, and we simply don’t know what to do. Oh, there were ideas tossed around: infrastructure bonds to stimulate the economy funded by the Federal Reserve, different ways to fund the deficits that everybody can see coming. But we all agree that there is no political will to stop them.

I spent a long time talking with one of my favorite philosophical economists, Dr. Ben Hunt of Epsilon Theory fame. While we have some minor disagreements, we share the sheer frustration, the sheer worry about the policies our current government has been pursuing and what they will do to the retirement hopes of the Boomer generation, let alone the growth potential to fund the hopes and dreams of the Millennials. We talked about how to help people get through what is going to be a very volatile and difficult time. I will share more on that in future letters.

I know this has been a little bit of a Debbie Downer letter. When the consensus is that we are going back to the zero bound on interest rates, we’re literally screwing an entire generation. People who have saved and worked and bled will be rewarded with zero interest rates and the need to take more risk in retirement, exactly the wrong time in their lives to be taking risk.

I promise in future letters I will write more about how to avoid the consequences I’ve mentioned above. Stick with me, we’ll get through this together.

Montana and Back to Puerto Rico

Shane and I are in Montana staying with Darrell Cain at his compound. He graciously invited Pat and Cheryl Cox to join us. Pat and I are working on several of the chapters in my book on what the world will look like in 20 years, which are kind of the rainbow and unicorn chapters. The world really is going to be a better place. We just have to get there.

Last night Howie Long was sitting next to us at the restaurant and I asked to take a picture with him. I reminded him that he, Roger Staubach, and Walter Payton were in New York for a Super Bowl party hosted by Société Générale where I won first place for trading futures and options on the Super Bowl score during the game. I got all sorts of fabulous prizes, including a football signed by these three famous Hall of Famers. I told Howie I would put this picture next to the original. I swear, he doesn’t look any older today than he did 20+ years ago. What a gracious gentleman.

Speaking of winning, my prediction for the gold price from last year at Camp Kotok was literally pennies from the actual price. Talk about fooled by randomness. And with that I will hit the send button and wish you a great week.

Your working on a plan that gets us through the 20s together analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.