Ray Dalio – John Mauldin Conversation, Part 6

-

John Mauldin

John Mauldin

- |

- July 12, 2019

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinNo Easy Solutions

A Radical Restructuring of the Economy and Tax Code

MP3?

A Brief Commercial

New York, Maine, and Montana

This is the final letter of the six-part series of my reply to Ray Dalio’s essays. Here are some links to help you wrap it all together.

- Ray’s original letter: Why and How Capitalism Needs to Be Reformed, Parts 1 and 2

- His follow-up: It’s Time to Look More Carefully at ‘Monetary Policy 3 (MP3)’ and ‘Modern Monetary Theory (MMT)’

- A generous and gentlemanly reply from Ray in Forbes

As Ray notes, the problems he describes really are existential. He and I agree more than we disagree, but our responses differ.

I think that we both agree that the wrong answers will cause much angst and pain for most of our fellow citizens (and that is a severe understatement). And given his reply to me in Forbes, I think Ray would agree with me there are no easy solutions, only very difficult choices vs. disastrous ones. The longer we wait to deal with the problems, the more painful resolving them will be.

And make no mistake, the existential problems we are talking about (and neither of us use the word “existential” lightly) will resolve themselves in a highly tumultuous manner if we as a society don’t face them directly and soon. They are mostly problems of our own making, and since there are no time machines, we must deal with the reality which we created.

Today in my final reply to Ray I sum up my previous letters and describe one possible path for dealing with these problems. My idea will be controversial for most people. I am totally open to another, better solution if anybody knows one.

Ray started his letter as an invitation to a dialogue/conversation. I hope we can continue our conversation and others will join in. And with that, let’s finish my open letter to Ray…

No Easy Solutions

Dear Ray,

Let me see if I can summarize my writing so far and what I believe to be your main concerns, which I share. I do welcome a response.

Last week I focused primarily on the US deficit and debt situation. Total federal debt is now $22.5 trillion plus another $3 trillion of state and local debt. Annual deficits are running at an average of $1.2 trillion and growing. As I demonstrated, in a recession the annual deficits will likely rise to $2.5 trillion, and certainly no less than $2 trillion, simply using CBO projections and assuming that revenues would drop and then slowly recover similarly to the last recession. I think that is a more-than-reasonable forecast.

That means total US government debt will be at $44 trillion plus maybe $6 trillion of state and local debt by the end of the 2020s, just a decade from now. Not to mention unfunded liabilities, corporate debt, etc. Of course, that assumes no tax increases and no budget cuts. Significant spending cuts are unlikely as the deficits are mostly entitlements, interest, and defense spending. So-called “non-defense discretionary” spending is actually a small part of the total budget. And while deficit hawks might find $100 billion to cut here and there, that wouldn’t affect the grand scheme of things. There is little political will to cut entitlement spending, and to your point, Ray, we may actually need more spending in order to solve the growing wealth and income disparity problem.

That brings us to taxes. Most tax increase proposals would raise rates on “the rich.” Using government data, I showed that a 25% increase on the top 10% of US income earners (roughly those making $120,000+) would produce only $250 billion per year. Ray, I am not certain what you think it will cost to reduce income disparity, but it would certainly eat up a good portion of that $250 billion, leaving little for deficit reduction.

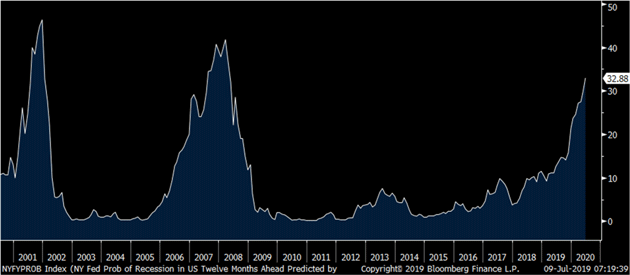

Any such tax increase will be even more difficult if we enter recession within the next few years, which the New York Fed’s forecast shows is not far-fetched. Here is their latest data showing a roughly 33% probability of recession within 12 months.

Source: Peter Boockvar

The longer the yield curve stays inverted and the more it inverts the more probable a recession is. We have now had an inverted yield curve for three+ months and as I write are still in that situation. The New York Fed’s model has never reached a probability of 100% prior to any recession. But if memory serves, there has always been a recession anywhere from nine to 18 months after the model reaches its current level. The timing isn’t precise, but it’s close enough for our discussion.

[Sidebar: To my regular readers, I will further discuss this and other recession indicators next week, plus the political and economic ramifications. Please be patient.]

In any case, at some point there will be a recession, the Fed’s rate cut plans notwithstanding. I think they will keep cutting at least back to the zero bound. You indicate that you believe, and I agree, that it won’t put the economy back on track. Then they will start with quantitative easing.

You also feel that QE won’t help and will likely cause even greater income and wealth disparity. I agree. But I have sat in meetings with participants in the Fed thought process. Confronted with the probability that their actions won’t deliver the desired results, they simply reply that we have to “do something.” I’m sure you’ve had that experience more times than I.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

No matter how ineffective we might believe it to be, they are going to keep rates at or below the zero bound and ratchet up quantitative easing, building the Fed’s balance sheet up to levels that today would seem mind-numbing.

I think Japan is the model here. Like the BOJ, the Fed will keep rates ultra-low and buy bonds until there are no more bonds to buy. The government will run massive deficits as long as the market lets them get away with it. And in Japan and apparently Europe, at least, the market seems to have quite a deal of tolerance in that regard. I call it Japanification and it will have roughly the same results here: extremely low growth, if any growth at all, tending towards deflation. Except that the deflation, at least in the price of things government doesn’t affect like healthcare, will likely be worse in the 2020s because of technology.

That’s not the end of the world, but it is certainly not a world that compares favorably to the 1950s, 1980s, or 1990s. You argue that we need to engage in a new combination of fiscal and monetary policy, something you called Monetary Policy 3, or MP3. Modern Monetary Theory (MMT) may or may not be part of that, and you caution that MMT has significant negative consequences and that you are not endorsing it. Again, I would totally agree. I want to come back to MP3 a little later…

A Radical Restructuring of the Economy and Tax Code

You’ve laid out what you believe to be the basis for how the economy and markets work. Let me offer a few simple assumptions of my own.

- There is no political will in either the Republican or Democratic party to reduce entitlement spending, and entitlement spending is on an ever-increasing path.

- There is simply no way that we can raise income taxes enough to close the deficit to within striking distance of nominal GDP growth (where debt relative to GDP growth is equal).

- As long as debt is expanding as it is now, we will stay in a slow-growth economy at best, if not in recession. Much research shows that increasing debt beyond today’s level will reduce GDP growth.

- What we need to do is very difficult: balance the budget, bring deficits and debt under control, so that we can begin to grow our way out of the crisis. But we can’t do that while thinking about revenues as we do now.

So what can we do? The first step toward getting yourself out of a hole is to stop digging.

I would suggest that the US adopt a Value Added Tax or VAT, excluding food and certain other basic necessary items. I would make the VAT high enough to completely eliminate Social Security taxes on both the individual and businesses, giving lower income earners a significant tax break. We could also compensate those below the poverty line for their VAT costs.

Ironically, you and I will both qualify for Social Security benefits soon. I daresay you need it even less than I do. We aren’t the only ones. I think we should consider means-testing Social Security, and the same for all entitlements.

Consumption taxes like the VAT are the least economically damaging of all taxes, at least according to most of the research that I have read. While I personally (or at least the economist in me) would like a VAT high enough to get rid of all other taxes, I just don’t know if it would be politically possible.

One attraction should be that, if the VAT is high enough, say in the 17 or 18% range, we could have much lower income taxes. Just for illustration, maybe there could be…

- No income tax below $50,000,

- A 10% income tax on incomes from $50,000–$100,000,

- A 20% tax on all income between $100,000 and $1 million,

- A 25% tax on incomes between $1 million and $10 million,

- and a 30% tax on incomes over $10 million.

… all with no personal deductions for anything. Period. That should certainly produce enough total revenue (along with corporate taxes) to fund the government as currently configured. It might even allow a little bit more for important needs we have deferred (like infrastructure) as well as medical and scientific research.

I totally understand that conservatives are uncomfortable opening the door to a VAT when a future majority might raise income taxes on top of it. I would be among them. In the spirit of compromise, we could amend the Constitution to require 60% majorities in both House and Senate to pass any tax increases. Of course, that would have to be passed by 37 states in order to become part of the Constitution, but that can be part of the negotiation process. Perhaps the new tax regime’s launch could be contingent on adoption by 37 states, which would encourage a more rapid adoption process.

I would also suggest that the tax changes be phased in over three or four years to allow for individuals and businesses to adjust.

This plan would eliminate the need for higher debts and quantitative easing, and would let the Fed keep interest rates at a more normal level. Retirees could once again look for an actual return on their savings, instead of the brutal punishment of financial repression. (We can have a whole separate conversation on allowing the market to set interest rates rather than 12 individuals sitting around a table.)

MP3?

I would welcome a further explanation of what you mean by Monetary Policy 3. I agree we need to do something far different than we are now. If we continue down this same path, at some point a more left-wing government will come to power, raise taxes and increase spending, but not really deal with deficits or the burden of ever-increasing entitlement spending. That will not work as well as they hope. I can totally foresee a movement back to the right, which would want to repeal those same policies. Neither side would actually come close to dealing with the real problems. We would remain in a regime of ever-increasing deficits, accompanied by growing debt and quantitative easing.

The simple fact of the matter: We don’t know how much debt the markets will be willing to give to the United States. As in actually having the cash, not to mention the willingness, to buy government debt. $44 trillion is a lot of money, which is why I think we will be encumbered with quantitative easing and zero interest rates until there is a significant structural change in how we manage revenue and spending.

We simply don’t want to know what the limit is on the amount of debt the United States can sustain. If we ever find out, it will be too late. We will be in a crisis.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Unfortunately, I think my proposal or any other compromise solution is simply not possible in today’s partisan world. That being said, I think this is an important conversation to have. When that crisis does happen, maybe somebody will pull one of the compromise plans off the shelf and say, “Let’s try this.”

What I don’t want to see is a repeat of what happened at the beginning of the Great Recession. When the powers that be finally realized the financial world was collapsing down around our ears, they had no plan. They were making it up as they went along. While they put out the fire, they also did a great deal of damage. This was not the best way to deal with the problem. But it was probably the best they could do at that moment, given the realities on the ground.

That’s why it is important to make this discussion become both public and national. I would hope that others will join us in thinking about how to restructure the US economy into a more self-sustaining and hopefully more equitable system. Having plans available for consideration in the next crisis will help create a willingness to compromise.

I think this may be the most important decision that our nation makes in my lifetime. If we continue down this path, at best we are consigning ourselves to more of the same meager growth. At worst, we will have a crisis that ends with what I call The Great Reset, where the world has to radically restructure its debt in ways that will not be pleasant. (That is an understatement along the lines of calling the Great Depression merely “unpleasant.”)

All this will be happening as technology improves our lives but also slowly eliminates higher-paying jobs, causing many people to earn less than they thought their education would justify. We will see more become “underemployed,” creating a great deal of political and social frustration. I hope we can avoid this type of Blade Runner outcome. There is the potential for a far more abundant and pleasant future for everyone, if we can reconcile these economic conundrums.

This has been a conversation well worth having. Ray, I want to sincerely thank you for starting what could be a very, very important national engagement. And politely ask for a little bit more elucidation on what you mean by MP3. Seriously… I really want to know.

A Brief Commercial

I know that many readers are small business owners, especially investment advisor/broker-dealer firms. One of the problems in the investment advisor business (as well as others) is that many of us are getting older and need to transition our businesses to younger successors who need financing. One of the partners in my network of recommended services is a national bank called T-Bank, which specializes in SBA (Small Business Administration) loans. They have done numerous SBA loans for small businesses that are transitioning to the next generation.

SBA loans also have other purposes and T-Bank is an excellent source. T-Bank also develops cash balance retirement plans that let owners save more tax deferred income (I have a cash balance plan and it indeed works!). You can learn more by listening to a podcast (or reading the transcript) I did on the SBA process by clicking here. There is also a direct number at the end of the transcript/podcast. I hope you find it helpful. (Note: I receive a standard referral fee from T-Bank as part of my business income.)

New York, Maine, and Montana

Early August sees me in New York for a few days before the annual economic fishing event, Camp Kotok. Then maybe another day in New York before I meet Shane in Montana to spend a few days with Darrell Cain on Flathead Lake.

I met with my partners Olivier Garret and Ed D’Agostino in Boston two weeks ago. We were making longer-term plans for Mauldin Economics, as we do from time to time. They have done a very good job of growing the business and I am happy with it. But they also expressed very clearly that I need to stop talking about writing a book about the future and actually begin writing. I am mentally ready, but structurally I am not always the most organized.

Writing a book is simply a massive undertaking, especially when it is as all-encompassing as “the future,” whatever that is. But to underline their insistence, they laid out a plan and offered help. It made sense and I am now actually beginning to write. The goal is to have a book in our hands sometime in the spring.

Much of the writing has already been done in one form or another; the problem is pulling it together, not to mention sorting through the thousands of pages of research on my computer and in links that I have saved, and much that has been sent to me by teams of my readers (thank you!). The good news is my travel schedule is not all that demanding over the next five to six months. And if Puerto Rico can avoid another debilitating hurricane, this is a great place to write.

Years ago, I took my family to Venice where a reader graciously offered to be our guide for a few days. He took us out to one of the small islands nearby where Ernest Hemingway actually wrote some of his novels. It was quite the idyllic location. I can’t complain in the least about my own location and circumstances, so I simply need to get on with it and crank out a chapter or two a week for the next five months. Plus my regular letters.

As my dad would say when we started a big project, “Son, that’s no hill for a stepper.” And with that, it is time to hit the send button. Let me wish you a great week.

Your getting ready to step up analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.