The Eurozone: Collateral Damage

-

John Mauldin

John Mauldin

- |

- February 8, 2015

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinGreece in a Nutshell

A Game of Chicken, European-Style

European Deflation

The 2015 Strategic Investment Conference

The Cayman Islands, Dallas, Florida, Switzerland, and New York

Collateral damage. Unintended consequences. Friendly fire. Certainly no one intended to have a global banking meltdown when they let Lehman Bros. go under.

Now we’re watching another Greek drama that could have significant unintended consequences – far beyond anything the market has priced in today. Then again, maybe not. Maybe the market is right this time. When we enter unknown territory, who knows what we will find? Fertile valleys and treasure, or deserts and devastation? Today we look at the situation in Europe and ponder what we don’t know. Greece provides a wonderful learning opportunity.

At the end of this letter I’ll mention our Strategic Investment Conference, which will be in San Diego, April 30–May 2. This week we have confirmations from George Friedman of Stratfor and Bill White, former chief economist at the Bank for International Settlements. The conference is shaping up to be the best ever. You can see the rest of the speakers at the end of the letter.

Let’s see if we can briefly summarize the situation in Greece. When Greece plunged into crisis three to four years ago, its debt-to-GDP ratio was about 120%. Greek interest rates rose precipitously as investors began to be concerned as to whether they would actually get their money back. The interest rate on the Greek 10-year bond went to 48.6%.

Everybody agreed that Greece couldn’t actually pay that debt; and since so much of it was owed to French and German banks (with not an insubstantial amount owed to Italian banks and those in other countries), the Eurozone decided to bail out Greece, which was a backdoor way of bailing out their own banks. (Seriously, you can go to the IMF minutes, in which they admit that the bailout was about saving the banks and the rest of Europe, not about Greece. Cyprus was cut loose when it would have been a rounding error for the EU to save it – but there were no European banks involved. (The lesson every politician should learn from this is that if you think you’re going to need a bailout someday, make sure your banks owe everybody else a lot of money.)

Everyone breathed a sigh of relief, and Greek interest rates fell to even lower levels than before the crisis, as you can see on the chart above. Meanwhile, because the solution forced Greece into a depression that reduced GDP by 25%, saw unemployment rise to 25% (nearly 60% among youth), forced Greeks (at least some of them) pay their taxes, and obliged the Greek government to try to balance its budget (kind of, sort of), the debt simply got worse. Now debt-to-GDP is 175%. If the Greeks couldn’t pay their debt at 120%, they have zero chance of paying it at 175%.

Eventually, Greek voters noticed that the agreement with the Troika (the ECB, the IMF, and the European Commission) didn’t seem to be working for them, so last month they voted in a new government that promised to change the agreement. The party that won the election, Syriza, had made lots and lots of promises about how they would make those mean old Germans back down and fork over the money. If we threaten to not pay the debt, the new government assured its citizens, the Europeans will give us more money, and we can even make them change the agreement. Of course, if the Greeks don’t get more money their system will be completely bankrupt, and their economy will collapse even further. (The technical economics term is that their economy will be screwed.)

This threat is somewhat like holding a gun to your own head and threatening to commit suicide if you don’t get your way. This is generally not a workable strategy when you are asking the politicians of other countries to pay a lot of money to keep you alive, especially when you are not very popular with the voters who elected those politicians. However, the new Greek government seems to think this is a perfectly reasonable bargaining tactic. Their new finance minister has written five books on game theory. It seems he has negotiating theory down pat, but in practice things are not working out according to his theory.

Because the Greeks agreed as a condition of their bailout to do something that is impossible – to pay off their debt – the rest of the Eurozone (led by Germany) actually wants them to continue to commit to doing the impossible in order that they might be given even more money, so that their debt, which they can’t possibly pay, can rise even further. (Yes, I know you may have to read that sentence three or four times to make sense out of it. That’s because the Eurozone’s position doesn’t make any sense.) The rest of Europe seems to be just fine with Greece’s going further into debt that it can’t pay, as long as they at least promise to pay it. The fact that their doing so will mean a permanent depression in Greece doesn’t really rank very high on their list of concerns.

Greek Finance Minister Yanis Varoufakis (until recently a professor at the University of Texas and as fine, or maybe more to the point, as typical a socialist as you will find at a US university) went on a tour of Europe to drum up support for the idea that, far from wanting more bailout money, Greece just wanted to buy time, via a “bridge agreement,” to work out a better plan. He came back home with a big fat nothing. He did elicit a little sympathy here and there, but no one offered any money or promises. And after he met with ECB President Mario Draghi, in what was at first thought to have been a cordial meeting, Draghi simply cut Greece off at the knees. From the Financial Times:

The French president said he supported the newly elected Syriza government in its efforts to secure a better deal from its international bailout creditors – possibly through an extension of debt maturities – as long as Greece committed to remaining in the euro, reforming its economy and honouring its debts.

Mr. Hollande also backed the European Central Bank’s surprise decision on Wednesday night to ban Greek lenders from using their country’s debt as collateral to access cheap liquidity. The move has been widely interpreted as a warning from the ECB to dissuade Athens from following through with a promise to abandon its EU bailout when it expires on February 28.

“The European Central Bank’s decision forces Greece and Europeans to sit at the same table to outline a new programme,” the French president said. “It’s legitimate.”

As the saying goes, with friends like this, who needs enemies? Greece is essentially isolated. As I understand it, the offer on the table is to extend the term of the debt, reduce the interest payments, and lighten up a little on austerity measures.

There is considerable debate as to whether the ECB actually had the authority to take the (highly political) action of declaring that Greek government debt is no longer acceptable collateral. The entire Greek finance program expires on February 28. Until that time, Greek banks can get Emergency Liquidity Assistance (ELA), which will cost them a great deal more. But ELA is available only to solvent banks with acceptable collateral. Further, the ECB has kept ELA for Greece limited to €60 billion. Ambrose Evans-Pritchard estimates that an amount closer to €100 billion will be needed, and very quickly. It is highly questionable whether the board of the ECB will grant any increase in the ELA program to Greece, absent an agreement. (You can find out more about Greece and the ELA here.)

Not only can Greek banks use only certain types of debt to access the ELA, that debt has to be free and unencumbered; and it’s not clear how much unencumbered collateral Greek banks actually have. Their consolidated balance sheet suggests they held close to €293 billion in loans and bonds as of the end of the December. Only €12.4 billion was actually Greek government debt. But €42 billion was in government-guaranteed bonds, which are not eligible to serve as collateral. Greek banks are already using €50 billion of ECB funding. Further, Greek banks had almost €40 billion in funding from non-Greek banks in the interbank market. It is highly likely that some of their assets, probably of the highest quality available, are pledged against that commercial paper. Further, 35% of Greek bank loans are nonperforming loans that are not eligible for ELA, and the rest would be subject to a severe haircut for collateral purposes (Davies).

The problem is compounded by the fact that money is beginning to leave Greek banks. “Flying out the door” might be a more accurate way to put it. Honestly, I can’t imagine leaving any significant assets in a Greek bank beyond what I would need for basic business transactions. Almost €14 billion were withdrawn from Greek banks in January, which was equivalent to the peak monthly outflow during the crisis of the last few years. You can bet the outflow did not turn around when Varoufakis came back empty-handed from his trip.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Essentially, Draghi told both the Greeks and the rest of the Eurozone that they needed to come to an agreement and do it fast. ECB collateral rules are arbitrary, and Draghi has arbitrarily put a time limit on the decision process. The total amount of time left is under three weeks, but there are interim deadlines that are even more important. The Greeks are to submit their financing proposals to the Eurozone finance ministers at their meeting on February 11 (next Wednesday).

Greece can probably fund itself into March by stretching out payments and engaging in a few bits of financial chicanery. But if the ECB does not extend their financing past February 28, the Greek banks are finished as solvent institutions. The ECB is basically saying that unless Greece agrees to continue to honor its agreements, funding will not be renewed or extended. At that point, Varoufakis would essentially have to issue Greek “scrip” in order to allow the banks to continue to function, but who would want that paper?

Things may come to a head even sooner than February 28:

Jeroen Dijsselbloem, who chairs the Eurogroup of eurozone finance ministers, told Reuters that Greece had to apply for an extension of its reform-for-loans plan by February 16 to ensure the eurozone keeps backing it financially. He stressed that the meeting on this date would be Greece's last chance to apply for the bailout extension, because some eurozone countries will need any agreement approved by their parliaments. The EFSF eurozone bailout fund, which is in charge of lending to Greece, will need time to complete its formalities, too.

But extending the bailout program, even temporarily, would mean agreeing to its terms that are hotly contested by Greece, leaving little common ground between Athens and the eurozone. (The Telegraph)

The clock is ticking. The 16th is just a week away. Not a lot of time for negotiations, and the rest of Europe doesn’t appear to be willing to give Greece more time. This seems to be a take-it-or-leave-it offer.

I’ve been talking with a number of people who have insights into the Greek issue. One trader/analyst at a major hedge fund, whose job it is to know these things, says that it’s very difficult to get a handle on how much interbank debt there is and who owes what to whom. Some of the big banks are telling us things are okay, but he worries about whether we can trust them.

How much of that €40 billion in interbank debt to Greek banks is subject to haircuts or defaults? How do you ring-fence that debt? If you don’t, it could be massively deflationary in an already deflation-prone system. We simply have no idea of the repercussions. Maybe the ECB steps in and makes the various banks whole if Greece leaves. Then again, maybe it decides that moral hazard must not be encouraged. It is certainly taking a hard line already with Greece.

On Friday after the close of US markets, Standard & Poor’s downgraded Greece to B- from B, just one level above default range. It kept its outlook negative, which means that Greece’s rating is likely to be cut further. “S&P said the downgrade ‘reflects our view that the liquidity constraints weighing on Greece’s banks and its economy have narrowed the timeframe during which the new government can reach an agreement on a financing programme with its official creditors” (The Telegraph).

It is not clear what the Greeks will do. A significant majority of the population wants to stay in the euro. But if Tsipras and Syriza back down, it is unlikely their government will last the year.

The problem is compounded by the fact that Greeks have already started not paying certain of their taxes that Syriza has indicated it wants to cut or eliminate. That drying up of revenue worsens the funding crisis the Greek government will face in early March.

Even if Greece were to leave the Eurozone and go back to the drachma, the promises the new government has made cannot be kept without further harming the country. They want to expand the government bureaucracy, raise the minimum wage, and increase taxes on businesses. None of these measures will spur economic growth and create jobs, which is what the country needs. Unit labor and productivity cost in Greece since the creation of the euro in 2000 has been roughly three times that in Germany. Even with the cost of labor dropping significantly, Greece is still not competitive on a productivity-per-worker basis with Germany and much of rest of Northern Europe.

A Game of Chicken, European-Style

We have two implacable forces moving toward each other at rather high speed. Let’s turn now to my friend Kiron Sarkar, who summarized the thinking on the European side of the table this morning in an email to me:

In addition to the issues I have already reported on, (basically, it's politically impossible for the EZ to accept an overt debt haircut on Greece's outstanding debt to the EZ at this stage), a number of other issues have popped up which will harden the EZ's/ECB's resolve and, in effect, make them get tougher with Greece. They include:

- Spain wants the EZ to get tough with Greece, as the government does not want to provide further ammunition to Podemos, the anti-austerity party (basically the Spanish Syriza), to gain further support. The crushing of Syriza will stem support for Podemos and other fledgling anti-austerity/EU parties, which have been gaining support in the EU. Spain is a far greater potential problem for the EZ than Greece;

- The upcoming French bi-election could result in Marine Le Pen's National Front winning – Hollande/French support for Tsipras will hurt him/the current regime further;

- Finland and Holland are getting tougher with Greece, to appease their own electorates, who are opposed to a debt haircut for Greece;

- German resolve is stiffening. The German's have had enough of references to the Nazis by Tsipras/Mr V/the Greeks. There has been a huge domestic political backlash, following Tsipras’/Mr V's comments;

- Mr. V. [Varoufakis] had disastrous meetings with Mr. Dijesselbloem and Mr. Schaeuble, the German finance minister. That is not going to do the Greeks any favours;

- France will not cross Germany; and better Italian data, together with Mr. Renzi's win over Berlusconi over the election of the President, has emboldened Renzi – forget the public comments;

- PM Mr. Orban in Hungary has his own domestic problems and is not liked in the EU, in any event. It is felt that Slovakia and Austria can be contained. Ireland will shut up and hope that Greece accepts the better deal (which they will get, either way) in due course;

- Furthermore, the recent Greek habit of not paying their taxes has emboldened the hawks in Berlin. They have told Merkel that it is yet another sign of Greek unreliability;

- German domestic public opinion (which Merkel follows closely) is turning sharply against Syriza/Tsipras/Mr. V. There is a growing opinion in Mrs. Merkel’s CDU and their sister party, the CSU, that the contagion risks of Grexit can be contained!!! The SPD do not want to alienate voters by supporting Greece. Finally, further aid to Greece requires the approval of the German Parliament – the Bundestag – no done deal;

- Initial US support for Greece is softening (turning?);

- Cyprus is starting to play up again – a “victory” for Syriza will encourage them to play act again;

- The threat (oh yeah) that Greece will turn to China/Russia for financial support is unrealistic, long-term. China does not want to cross Germany and, in any event, will move cautiously. Russia is a wilder card, but they have enough financial and other problems of their own;

- Syriza's coalition partners (the Independent Greeks) have the defense ministry portfolio and are pro-NATO. Unfortunately, the Defense Minister is an unsavory character and is also seriously anti-Semitic. The current coalition agrees only on its opposition to the bailout programme – expect violent disagreements (a bust-up?) once that has been settled, either way;

- Finally, Germany (and a number of other important EZ countries) are fed up with Greece/Cyprus's attitude towards issues such as Macedonia/Cyprus itself/EU sanctions on Russia re Ukraine, etc.

Greece’s position was not helped by a Varoufakis press conference in Germany during which he talked about Nazis. Yes, I know he was referring to the Nazi party in his own country, but he reminded the Germans that they were once run by Nazis, and it didn’t work out very well for them, so they should understand and give Greece a lot of money. I’m not sure why he thought that would be a helpful analogy, but it just further poisoned the well.

Then Tsipras gave his first major speech to the Greek Parliament on Sunday, in which he said again that Greece wants no more bailout money, that he still plans to renegotiate its debt deal, and that he still seeks a “bridge agreement” to tide the country over until a new pact is sealed. He apparently believes that Draghi and the Eurozone finance ministers in Europe don’t really mean it when they say there will be no bridge agreement without an agreement to maintain previous commitments.

As Kiron noted above, there seems to be a growing consensus that Europe can contain the problems from a Greek exit of the Eurozone. What are the chances of Greece’s leaving, either willingly or unwillingly? After the speech Tsipras gave today, I think it’s a 50-50 thing. Tspiras and Varoufakis seem to believe that the risk of a major Eurozone crisis if Greece leaves is a big enough threat to force Europe to fund them in order to avoid it.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

The European Commission has put out its projections for 2015. Buried in the tables is its projection for inflation for Europe: -0.1%. They have Greece at -3.3% year-over-year and Spain at -1.5%. Italy is expected to experience mild deflation.

Japan is fighting deflation with a level of quantitative easing that is 15% of its GDP, and it is not clear that it’s winning. The European Central Bank wants to fight deflation with half that level of QE, spread out over a longer period. Rates are already so low that it is essentially meaningless to try to drive them down. How much can 20 basis points actually do for you? Ask Japan.

QE may indeed help spur European stock markets, and banks will benefit, but what does that do for Main Street Europe?

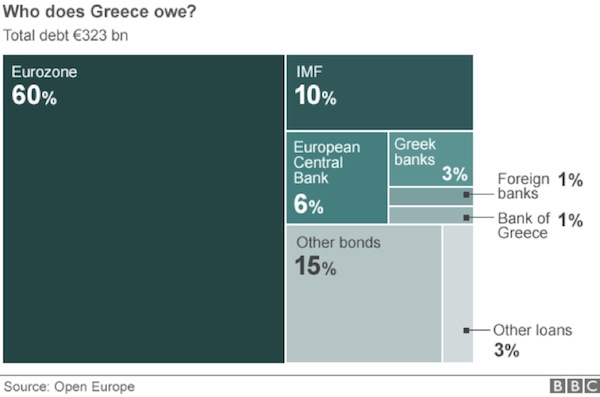

A Greek exit from the Eurozone will only make deflation pressures worse. The chart below shows where Greece owes its €323 billion. I assume that the vast majority of this debt will go “poof” at the moment of exit. The ECB can paper over a lot of it, or at least I think they can, but the question is, how much of the private debt will they cover?

And how will the interbank debt be dealt with? What about the remaining debt that is held by foreign banks, as well as Greek bonds in all sorts of funds?

Does Greece remain in NATO? Do we really want an anti-NATO country in the Balkans? That would be rather a nuisance. Can Greece stay in the free trade zone created by the European Union even if it leaves the European Monetary Union (the Eurozone)? Can the Greeks run a dual-currency system somewhat the way Argentina does, one where the official currency is the drachma but real transactions are done in euros? If the current Greek government gains the power of the printing press, it is quite likely that we will see very high inflation in short order, at least in terms of the drachma.

Could it be that Tsipras really wants to leave the euro but feels it will be better for him politically if it appears that Greece is forced out of the euro because the ECB has taken away the ELA? If you go back to his early speeches, he was all for leaving the euro unless Greece got total debt forgiveness.

Exactly what could the ECB and the rest of the EU do if Greece leaves? It’s not as if they can repossess a few Greek islands. Can you go after private Greek assets outside of the country? That approach would seem to be highly problematical. The lawyers could be fighting over this for years.

There are no clear answers for any of these questions. We have an inexperienced government trying to bluff in a poker game full of professional card sharks. The good news is that the situation is unlikely to remain unresolved for months or years. We are talking days and weeks.

After the last bailout, I said that Greece would end up defaulting again. The bailout agreement was not unlike the one imposed upon Germany at the end of World War I. It was simply mathematically impossible for it to work. I have sympathies for both sides.

Many of us have had the uncomfortable experience of watching a marriage of close friends come apart. Sometimes, a divorce really is the best thing, but it is nearly always painful and very expensive. The old joke goes something like this: Why is divorce so expensive? Because it’s worth it.

In the end, I think Greece will be better off leaving the euro and negotiating as hard as possible to stay within the European Union. Europe, after absorbing the cost, will be able to move on and begin to deal with the sovereign debt problems of the other troubled countries, including France. In a way, Greece is just a distraction from the very real crisis brewing in the rest of Europe. Stay tuned.

The 2015 Strategic Investment Conference

As I said at the beginning of the letter, George Friedman of Stratfor and Bill White, the former chief economist at the Bank for International Settlements have just agreed to speak at my conference. They will be joined by (in no particular order) Peter Briger of the $66 billion Fortress Investment Group, who will talk on the state of credit in the world; David Rosenberg; Dr. Lacy Hunt; Grant Williams; Raoul Pal; Paul McCulley; David Harding (of the $25 billion Winton fund family); Louis Gave; Jim Bianco; Larry Meyer (former Fed Governor); the irrepressible Jeff Gundlach; the wickedly brilliant Stephanie Pomboy; Ian Bremmer; David Zervos; Michael Pettis (flying in from China); and Kyle Bass, along with Jack Rivkin of Altegris and your humble analyst. There will still be a few more to add to the list, but it’s already shaping up to be our best conference ever.

The conference is in San Diego, April 30–May 2, and will once again be at the Hyatt Manchester. For the first time this year, our conference is open to everyone, not just accredited investors. You want to register now so that you can get the early-bird discount.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Since the first year of the Strategic Investment Conference, my one rule has been to create a conference that I want to attend. Unlike many conferences, this one has no sponsors who pay to speak. Normal conferences have a few headliners to attract a crowd and then a lot of fill-ins. Every speaker at my conference is an A-list speaker I want to hear, who would headline anywhere else. And because all the speakers know the quality of the lineup, they bring their A games.

Attendees routinely tell me that this is the best conference anywhere, every year. And most of the speakers hang around to hear what is being said, which means you get to meet them at breaks and dinners. Plus, this year I am arranging for quite a number of writers and analysts to show up, just to be there to talk with you. And I must say that the best part of the conference is mingling with fellow attendees. You will make new friends and be able to share ideas with other investors just like yourself. I really hope you can make it.

Registration is simple. Use this link. While the conference is not cheap, the largest cost is your time, and I try to make it worth every minute. There are also two private breakfasts where hedge funds will be presenting. Altegris will contact you to let you know the details.

The Cayman Islands, Dallas, Florida, Switzerland, and New York

I will be somewhere close to a beach as you read this, either on Little Cayman with my friend Raoul Pal or at a conference on the large island later in the week. I will be presenting with my friend Nouriel Roubini at the Cayman Alternative Investment Summit, one of the premier alternative investment conferences of the year. They always attract very interesting speakers and entertainment. I see a few days of R&R on the beach (as well as in the gym) before and after the conference. Maybe I can catch up on some of my reading, too.

Then I will be back in Dallas to speak at an open forum for financial advisors, sponsored by S&P and called “Managing Risk and the Future of Factor-Based Strategies.” If you are an investment professional, you can register at this link.

At the beginning of March I will be in Orlando to do a keynote presentation for the American Banking Association and share a dinner with my old friend Greg Weldon. A few weeks after that, I fly to Geneva and Zürich, where I have a very packed schedule. In addition to speaking, I’m particularly looking forward to being with Dylan Grice and meeting Bill White for the first time, plus lots of other friends. I’m sure I will be staggered by the cost of everything in Switzerland, but the train ride from Geneva to Zürich is worth every penny. On a side note, Bill White was smart enough to negotiate his speaking fee in Swiss francs while I’m getting dollars for mine. That should probably tell you all you need to know about whose advice you should listen to.

I have some other speeches in Dallas and will then head to New York at the end of March.

The twins are in town to see their new nephew (Henry Junior), and it appears that I’m going to get all my kids together for brunch. I’m pretty excited about that. I’ll write next week about what I learned in the Caymans. Have a great week in the meantime.

Your wondering how cheap a Greek vacation will get analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.