Higher for Longer?

-

John Mauldin

John Mauldin

- |

- March 8, 2024

- |

- Comments

- |

- View PDF

John Mauldin

John Mauldin“There is a difference between you and me. We both looked into the abyss, but when it looked back at us, you blinked.”

-Batman, referencing Nietzsche in 2010’s Justice League: Crisis on Two Earths

-My first thought on the quote: Think Jerome Powell and the FOMC

The idea that “market expectations” tell us anything about the economy’s future is – or should be – in serious doubt. That’s not to say the market is wrong. It just changes its mind so often as to be useless. And most of the time, it changes its mind after the fact.

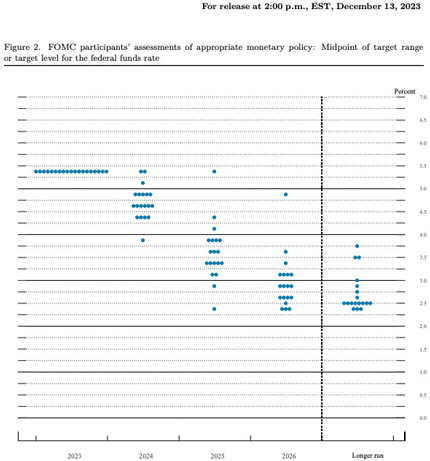

Currently we see this in the outlook for interest rate cuts. Futures prices implied as many as six cuts early this year even though the FOMC members who will actually make that choice were signaling nothing of the sort in their dot plots. The last round in January showed an average of three cuts expected, with two committee members wanting to hold rates steady all year.

Source: The Fed’s New Dot Plot — And What It Says About Interest Rates | Bankrate

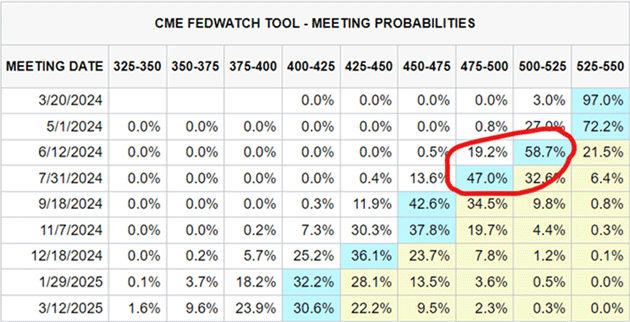

The market is still telling us they expect the Fed to cut 4 times this year. Here is the market projections for rate cuts after the NFP release. The market will be wrong.

Source: Samuel Rines, CORBU Research

Cue Mick Jagger: “You can’t always get what you want, but… sometimes you get what you need.”

We’ll get another round of dot plots later this month, so it’s possible Fed leaders will move closer to market expectations. More likely, in my opinion, is they will go the other way, throwing cold water on the notion rates will “normalize” this year. Aside from the fact no one knows what “normal” should be, the economic data simply doesn’t show a compelling need to cut rates.

For this letter, I want you to put yourself in the position of an FOMC member. Since you are not a political hack, you want to do what you think is best for the overall economy and Main Street while recognizing some sectors may not be happy.

As we will see, your fellow FOMC members are worried about inflation coming back if they cut rates too fast. That would be a far worse outcome than simply waiting a few more months. Cutting rates only to have renewed inflation force another hike is more than just an embarrassment. It would have serious implications for almost all sectors of the economy.

Inflation isn’t yet close enough to the Fed’s 2% target to declare victory. It’s improving, yes. But 2.6% isn’t the same as 2%. And 2% is still too high for retirees.

As I have for several years, I think rates will stay “high” for a long time. That’s bad news if, for example, you are a highly leveraged business or you are looking for a new home. It’s also bad news for interest expense on government debt. But, at least in theory, those aren’t the Fed’s mandate. Its two concerns are price stability and maximum employment. The second of those is in a good place but the first one is still in progress.

Not so long ago, these rates we now consider painfully high weren’t unusual. The economy was actually better in many ways, too. “Higher for longer” may sound scary if you have a lot of debt, but to Fed officials, it’s not necessarily so bad. And savers/retirees love higher rates.

Ticking Higher

I want to review something that used to be obvious, but no longer is. Why does the Fed raise and lower interest rates?

The answer is in that dual mandate. The Fed tightens when it wants to encourage price stability (i.e., control inflation) and loosens when necessary to promote maximum employment or economic growth generally.

(Which is why stagflation is so bad. High inflation and rising unemployment? No policy “works” because whatever you do will cause severe pain. See Volcker as a reference.)

Because policy changes take so long (the lag effect) to show the desired effects, the Fed tends to overshoot in both directions. They loosen too much and start inflationary booms, then tighten too much and send the economy into recession. Those are avoidable in theory. In practice, not so much, which is why the “soft landing” scenario seemed unlikely this time two years ago.

Now we are in a weird situation: Inflation has diminished but the boom is still going. It’s not like the expansions we saw before 2008. Nevertheless, GDP growth, employment, and other indicators are generally positive. Inflation, while higher than targeted, is much lower than it was.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Can you point to signs of weakness? Sure. Plenty of cracks in the armor. There are always weak data points in any economy. We all read them every day. But they aren’t yet popping wide open, and it could be a long time before they do. The Fed responds to data, not hints, and for now the data shows no urgent need to stimulate more growth. Again, the FOMC members also know looser policy will involve some risk of stimulating too much growth and bringing inflation back.

That view, while not universal, is compelling some serious observers to predict little or no loosening ahead. Apollo Global Management’s Torsten Slok made headlines last week by saying the Fed won’t cut rates at all in 2024. He says it in a kind of “emperor has no clothes” way, like Wall Street simply refuses to see reality.

Here’s Slok:

“The market came into 2023 expecting a recession. The market went into 2024 expecting six Fed cuts. The reality is that the US economy is simply not slowing down, and the Fed pivot has provided a strong tailwind to growth since December.

“As a result, the Fed will not cut rates this year, and rates are going to stay higher for longer.”

(Yes, yes, DR, I know that some GDP forecasts for Q1 are coming down, but they are still quite positive.)

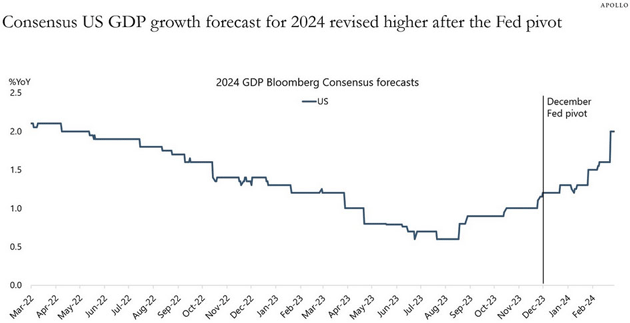

Things move fast so let’s recall this “December pivot” he mentions. That month’s FOMC statement implied the committee believed rates had gone high enough. They had paused six months earlier, inflation had not returned, and the Fed suddenly seemed more concerned that high rates were slowing growth. That meant rate cuts were back on the table.

Now, we don’t know exactly what was said in the committee room. But whatever it was, the Fed seems to have enticed a lot of money off the sidelines and into various investments, both stocks and corporate CapEx. It is visible in the GDP growth forecasts.

Source: Apollo Global

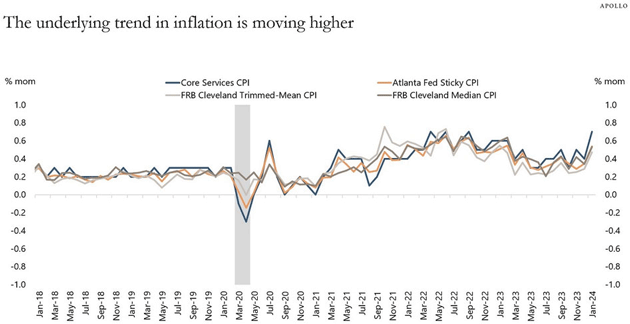

Lower bond yields after the December FOMC provided what Slok calls a “tailwind to growth” which he thinks pushed the Fed back into inflation-fighting mode. They look at charts like the one below and don’t like it at all. (Note this chart shows month-over-month inflation trends, not annual.)

Source: Apollo Global

Zoom in on the right side there. Note the lines all began trending downward in mid-2022 as the Fed finally got serious about inflation. They flattened after the tightening paused in mid-2023. Now they’re ticking higher again. Since you are a FOMC member, this is hard to tolerate. It makes 5.5% rates look about right, certainly not too high, and certainly shows no need for rate cuts.

|

“I Need to See More Progress”

The FOMC dot plots are anonymous so we can’t connect the dots’ forecasts to specific members. Some are more open than others. Atlanta Fed President Raphael Bostic said back in December he expected two rate cuts in 2024 if inflation stayed under control. Last week he changed that to just one cut, which he thinks will come in the third quarter and be followed by a pause. That’s a bit less hawkish than Torsten Slok, but not much.

Bostic expanded on his views in a remarkably clear and non-technical letter posted this week to the Atlanta Fed’s website. I highly recommend you read it. Bostic is a PhD economist but doesn’t sound like one.

“I believe inflation is on track to slowly return to the Committee's 2 percent objective, alongside a strong labor market and expanding economic activity. That's unusual. Typically, unemployment rises when the Fed tightens monetary policy to subdue outbreaks of inflation like the one we experienced beginning in 2021. So, a return to price stability without deep economic pain would constitute a resounding success by historical standards.

“Just how different is this episode? Research tells us that when the Fed tightened policy aggressively in previous cycles, the unemployment rate rose by about 1.5 percentage points, on average. That hasn't happened this time, so far at least. When the Committee began raising the federal funds rate in March 2022, unemployment was 3.6 percent. After 11 rate hikes, January's unemployment rate stood at 3.7 percent.

“The unemployment rate has remained benign as monthly employment growth has held up remarkably well. Revisions from the Bureau of Labor Statistics bumped up the job growth numbers for late 2023, and the original report for January exceeded all expectations. Importantly, data also showed that job creation in January broadened beyond the small number of sectors—notably, health care—that had accounted for an outsize share of growth in the second half of 2023. I don't overreact to one month's data, to be sure. But a job market that had been cooling—effectively slowing to a normal state—has shown fresh signs of strength.

“The story is similar for economic growth. Econometric evidence suggests that past tightening cycles led to about a half-percentage-point decline in real gross domestic product over two to two-and-a-half years—a recession, basically. Bucking that history, real GDP grew at a 3.3 percent annual rate in the fourth quarter of 2023 by the Bureau of Economic Analysis's initial estimate, and at a 3.1 percent clip for all of 2023. That's a more robust performance than private sector forecasts anticipated and, quite frankly, more robust than what we at the Atlanta Fed expected.”

John here. What you just read was Bostic’s optimistic argument. Next comes the “But…” portion. Note the part I highlighted in bold.

“As promising as that all sounds, the resounding success I mentioned—a return to price stability without economic pain—is hardly assured. That is largely thanks to the second of my three points: Because uncertainty is rampant in the domestic and global economies, it is premature to claim victory in the fight against inflation.

“January inflation readings came in surprisingly high, the latest reminder that the path to price stability is not a straight line. I need to see more progress to feel fully confident that inflation is on a sure path to averaging 2 percent over time. Only when I gain that confidence will I feel the time is right to begin lowering the federal funds rate to dial back restrictive monetary policy…

“There is another upside risk I'll highlight. As my staff and I have talked to business decision-makers in recent weeks, the theme we've heard rings of expectant optimism. Despite business activity broadly moderating, firms are not distressed. Instead, many executives tell us they are on pause, ready to deploy assets and ramp up hiring when the time is right.

“I asked one gathering of business leaders if they were ready to pounce at the first hint of an interest rate cut. The response was an overwhelming "yes."

“If that scenario were to unfold on a large scale, it holds the potential to unleash a burst of new demand that could reverse the progress toward rebalancing supply and demand. That would create upward pressure on prices. This threat of what I'll call pent-up exuberance is a new upside risk that I think bears scrutiny in coming months.”

John here again. I’m pretty sure Bostic chose his words carefully. He wants to be “fully confident inflation is on a sure path to averaging 2 percent over time” before he would be comfortable cutting rates. His language sets a high bar.

(I am more and more a fan of Bostic. Quite the opposite of Alan Greenspan who once said: “I know you think you understand what you thought I said but I'm not sure you realize that what you heard is not what I meant.”)

But Bostic’s biggest concern is what he calls “expectant optimism” and “pent-up exuberance.” Business leaders, at least in his region, say they will leap into action as soon as they see interest rates start falling. He worries this would mean a “burst of new demand” that produces more inflation pressure.

Bostic is just one voter, but I suspect others have similar leanings. And they all, whatever their views, know the next easing will be a critical decision. I think they will want to make it unanimous. Achieving that consensus could easily take longer than current market expectations (see below), if not all year.

Potential Sparks

If the FOMC really wants to see inflation consistently at 2% before it cuts, then housing prices are the main barrier. Most other spending categories are either in range or on track to be there soon.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

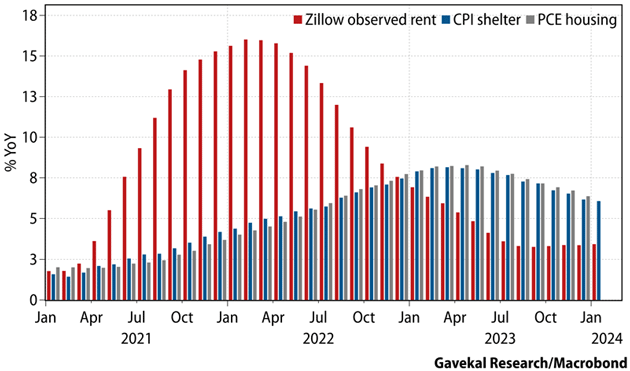

By many non-government measures, housing prices are indeed softening. This has been slow to affect the official inflation benchmarks because they’re intentionally designed not to react quickly. Here’s a good illustration (via good friend David Bahnsen).

Source: David Bahnsen of TBG

Note that recent Zillow rent growth has been stabilized well above 3%. Nonetheless, the housing portions of CPI and PCE were gradually improving until some unexpected strength in the January data. Now it seems that may have been a data glitch. We know this only because a bunch of analysts pestered the Bureau of Labor Statistics to explain how owners’ equivalent rent could increase 0.6% when rent rose only 0.4%.

After weeks of awkward silence, the agency finally explained it had “refined the weighting method” for the OER part of CPI. It had to do with the proportion of single-family homes to “non-detached” homes like townhouses and condos. They do this every year but, in this case, it seems to have made an unusually big difference.

If we assume that was a one-time event, then maybe housing prices will keep moderating. I should note, since I mention Torsten Slok, he sees both rental rates and home prices rising, and has some data to prove it. Others have quite contradictory data. They could all be right; all real estate is local, as the saying goes. But on a national average?

The broader point in almost any scenario is that housing inflation, if it improves, will improve only slowly. That’s hard to square with the high level of confidence FOMC members like Bostic say they want to see.

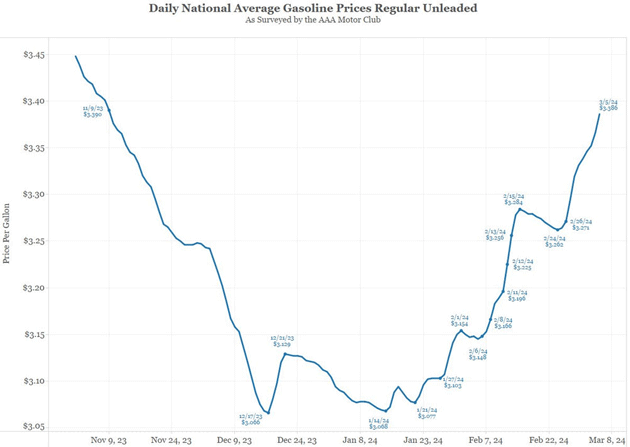

Nor is housing the only potential inflation spark. Here’s a gasoline chart from Jim Bianco, showing a recent surge in gasoline prices.

Source: Jim Bianco

The Fed’s 2% inflation goal looks at core indexes which exclude energy, so this isn’t directly part of it. But it will eventually seep into the core if fuel prices keep rising.

Where does this leave the rate cut prospects? As of now, I think Bostic’s “one cut and a pause” is probably the best case scenario for those who want lower rates. No cuts at all are a non-trivial possibility. We’ll know more with the next dot plots on March 20.

A few economists, notably Larry Summers, see a small chance the Fed will raise rates this year if inflation starts climbing again. I don’t know about that but, barring a deep and sudden economic downturn or a real problem in bond markets, rates don’t seem likely to fall all that much.

A man hears what he wants to hear and disregards the rest. We all have our biases. You can find a LOT of cracks in the economic data. Enough to fill your bearish economic heart.

But again, imagine you are on the FOMC. Your colleague Bostic and others are surprised and pleased to see the economy doing well after a quick, steep tightening cycle. You really want to keep it going. The dilemma you face is two parts:

-

If you cut too soon and inflation comes back, it could seriously create stagflation, the worst of all worlds for the Fed.

-

If you wait too long, the economy could roll over into recession. That means you might have to cut deeper and faster than you would like.

Plus, just to make life harder, this is an election year. You will be accused of political mischief no matter what you do. Traditionally, you try not to make major monetary policy changes a few months before an election. If you are going to cut rates, maybe the best thing to do is cut in June and then signal a “Bostic Pause” until November. Then you can assess the need for more cuts.

The only way you act is if the data overwhelmingly calls for rate cuts. What could that be? Turmoil in the bond market? A surprising downturn in employment? You really have to ignore the stock market. As an FOMC member, you aren’t responsible for maintaining historically high valuations.

Powell said this week it’s time to consider rate cuts, but steered clear of saying when. You can read into his masterfully vague but hopeful comments whatever you wanted to hear. Greenspan would approve. We will see who blinks….

No Better Time for an SIC

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

We have almost finished putting together what will be the single best faculty we have ever had for any of the 19 previous Strategic Investment Conferences. But given all the new complexities in the market, economy, and the world, we need the best thinking and insights we can get. This conference reminds me a lot of what was going on in 2008. Different economy, but every bit as complex, both good and bad.

We have so many topics that simply must be discussed: artificial intelligence, geopolitics and the risk of war, an election year which is going to be volatile and contentious. Many parts of the stock market are at nosebleed-high valuations. Yet technological marvels abound. We have to cover the incredible advances in biotechnology and aging. Of course, the Fed. I have assembled a dream team to discuss social and economic cycles.

In short, this is simply going to be the best SIC I have ever put together. I am blown away by the willingness of so many “celebrities” to join in the discussion. And the technology we are using this year will allow you even deeper interaction with speakers and other attendees.

The conference will again be virtual, every other day for five days from April 22 to May 1. You can watch it live and interact, watch it on your own time, read the transcripts, or listen to the presentations. It all works with your schedule.

Don't procrastinate, sign up today. Click here to see some of the confirmed speakers. Trust me, it gets better and better. There will be some surprises on the political and geopolitical side, to be announced soon. All of which will impact our portfolios and lives. You know you really want to!

New York, DC, and Tiffani

I need to get to New York sometime in early April and will be in Washington, DC, in mid-April. It would be great if we could combine the two. I will be back in Dorado for the SIC.

My daughter Tiffani will be here next week. We are working together on some projects. It is good to be working with her, hopefully not briefly. Her birthday is this week. How can I have multiples kids in their 40s or almost?

I can't begin to convey how excited I am about this year’s SIC. You really need to sign up and attend. And with that, it is time to hit the send button. Have a great week and spend more time with friends, even if it’s on the phone or video! That always pays life dividends. Life is just so much fun!

|

Your not even thinking about slowing down analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.