First, Let’s Lower the Bar

-

John Mauldin

John Mauldin

- |

- November 12, 2010

- |

- Comments

- |

- View PDF

John Mauldin

John MauldinHealth-Care Realities

The Chinese Renminbi is Going Down, Not Up

First, Let’s Lower the Bar

They Need to Borrow How Much? Really?

Irish Eyes Are Not Smiling

La Jolla, New York and a Forbes Cruise

China’s currency is rising ever so slowly against the dollar. But is that hurting China? We will look at a very interesting chart and some research. And then we’ll gain some more insight into why the employment numbers seemed to surprise. I guess if you lower the bar, it’s easier to jump over. I also deal with the pushback from last week’s Outside the Box! And Ireland is on my radar. There is a lot to cover, so let’s jump in.

I start this week’s letter on a flight from Cleveland (where I was at the Cleveland Clinic meeting with my good friend and doctor Mike Roizen (of Oprah and the various “YOU” books with Mehmet Oz) on some non-health-related business, and we talked last night about the state of health care. Mike keeps pointing out that much of our health-care cost comes from chronic diseases that are either directly or partially lifestyle choices. And he is right. The data shows it. Smoking, overeating, lack of exercise – all contribute to our health-care bills. And health care was on my mind.

Now, a little mea culpa. I get letters from readers who start their missive out with something like, “I know you probably won’t read this, but…” Well, I can’t say I read every letter, but someone does and I get and read as many as I can. And my rule is that I get all the negative ones, and any letters that show particular thoughtfulness and give me suggested reading or just good suggestions. I do pay attention to you. It takes some time, I admit, but I think it is important.

And the feedback I got on last week’s Outside the Box on health care was definitely running much more on the negative side. And as it turns out, for good reason. There were just simply some factual errors in the piece that made it more partisan than it sounded when I first read it. And many readers justifiably took me to task for that.

What attracted me to the piece to begin with was the central fact that the incentives within the health-care bill give businesses significant monetary reasons to do things that are not in what I think of as the best interests of the economy or labor. Businesses will be able to save a great deal of money by canceling their employer-paid insurance plans and simply paying the fine and offering their employees some kind of cash payment to buy managed-care programs. Go to Friday’s USA Today. Read the story on Medicare-managed health care, about the shortage of specialty doctors and the denial of benefits that I think of as routine in my more or less plain-vanilla health insurance plan. I don’t think people are going to be happy.

Second, there is the incentive to hire part-time employees over full-time, and thereby not have to provide insurance. This is already an issue I see every week with my own kids, as getting full-time jobs even in relatively OK Texas is an issue. As a nation, we are already witnessing a disconcerting and still-rising level of part-time employment. Do we really want to encourage more of that?

If there is one thing we know in economics (and there are admittedly distressingly few of them), it is that people respond to incentives, whether intended or unintended. I don’t think the writers of the health-care bill intended to increase part-time employees, keep payrolls under 50 employees, or encourage businesses to dump their health insurance or move to outsourcing, etc. But if you are a business person facing budget and sales shortfalls, rising prices, and fierce competition (is there any other kind?), saving $2-3,000 per employee is going to be tempting. When two part-time employees cost $3-6000 a year less than one full-time? What do you choose when the boss is breathing down your neck about expenses? The recent employment data tells me that already businesses are opting for more part-time workers. It doesn’t work for every business, but it will for a lot of them. I hope that is not going to be the case, but I want policies that encourage and reward good corporate behavior.

For many people who read the letter, the factual errors obscured the main points. Frankly, I understand. I often have that reaction in reading other material myself. But Outside the Box is not “other material.” I put this out there, and with the core standards we have in place, I should not have been as tone deaf. I WILL be better. And in a few weeks, we will have a new website with reader forums and feedback (targeting December – this is a major project and they always take more time than I would like).

Two things I did take away from the feedback. First, most of my readers are amazingly civil in an era where simple civility on the internet is not the norm. And second, this is an extremely emotional issue. Most of us have stories about people who have been hurt by not having access to health care. And it is a lot more complex, with more moving parts, than any issue we face as a nation.

I spent some time with Newt Gingrich this Wednesday. He seems to me surprisingly upbeat about the potential for solutions to the health-care issue. He points out that there are some amazing medical advances just around the corner. A cure for Alzheimer’s would save, according to Newt, about $20 trillion over the coming decades. Cancer? Heart disease? My friend Pat Cox suggests we are on the edge of a tsunami of medical breakthroughs.

But we have been seemingly on the edge for a long time. As I wrote a few weeks ago:

Let's look down the road. I think we will at best be in a Muddle Through Economy for the next two years. Unemployment is going to be above 8%, best-case, in 2012. If the Bush tax cuts are not extended, in my opinion it is almost a lock that we go into recession next year, unemployment goes to 12%, and underemployment gets even worse. That is not a good climate for Obama and the Democrats in 2012. It is especially bad when you look at the number of Democratic Senate seats up for re-election that are in conservative states. The Republicans could take a serious majority in the Senate.

And then what? Right now Republicans are running on promises that they will not cut Medicare and Social Security, but are going to reduce spending and get us closer to a balanced budget. But everyone knows that the only way to get the budget into some reasonable semblance of balance will be to either cut Medicare benefits or increase taxes.”

There are only the two options. Yes, you can reform medical care, and I think much of Obamacare should certainly be repealed, but that does not get us anywhere close to dealing with the real issue, and that's a fact. There are tens of trillions in unfunded liabilities in our future, which must be dealt with.

Let me be very clear on this. I am not really worried about the supposed $75 trillion in unfunded Medicare liabilities in our future. That is an impossible number. If something can't happen it won't happen. Long before we get to that apocalypse, we find a bond market that simply refuses to fund US debt at anywhere near an affordable cost. Crisis and chaos will ensue.

People only accept change when they are faced with necessity, and only recognize necessity when a crisis is upon them.

- Jean Monnet

The simple reality is that if We the People of the US want Medicare, in even a reformed and more efficient manner, we must find a way to pay for it. It will not be cheap. Raising income taxes on the "rich" is not enough. You have to go back and raise income taxes on the middle class, too. Oh, wait, that will be a drag on the economy and consumer spending. And in any event it will not be enough.

The only real way to pay for those benefits will be a value-added tax, or VAT. And while it could be introduced gradually, let there be no mistake that it will be a drag on economic growth. Government spending does not have a multiplier effect on the economy. It is at best neutral. What creates growth is private investment, increases in productivity, and increases in population. That's it. Tax increases have a negative multiplier.

A significant VAT along with our current income taxes will give us an economy that looks more like the slow-growth, high-unemployment world of Europe. Can we figure out how to deal with that? Sure. But it is not growth-neutral.

Republicans in 2013 will be like the dog that caught the car. What do you do with it? The last time they (embarrassingly, we) really screwed it up. The defining political question of this decade will not be Iraq or Afghanistan, or the environment or any of a host of other problems. The single most important question will be what do you do with Medicare? Cut it or fund it? Reform it for sure, but reform is not enough to pay for the cost increases that will come from an increasingly aging Boomer generation.

There is no free lunch. At some point, Republicans cannot run on "no cuts in Medicare" and "no new taxes" and be honest. At least not this decade. Maybe when we have cured cancer and Alzheimer's and heart disease and the common cold at some future point, medical costs will go down, but in the meantime we have to deal with reality.

You may be able to fool the voters, but you will not be able to fool the bond market. Not dealing with reality will create a very vicious response. Ask Greece.

And that is the national conversation we must have with ourselves. There is a cost to government. There is a cost to extended Medicare benefits. (I am blithely assuming we deal with all the "easy" stuff like Social Security, and make real cuts in other areas.)

Enough on medical issues. Let’s jump into the rest of the letter.

The Chinese Renminbi is Going Down, Not Up

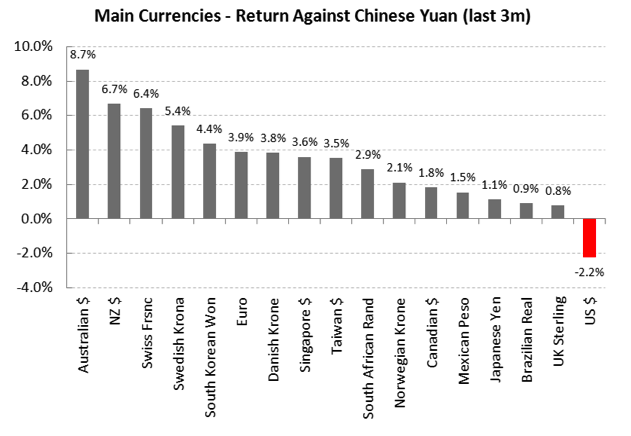

While I was sitting in the trading room of my co-author of The Endgame, Jonathan Tepper, last week, we got to talking about the need for the Chinese currency to rise against the dollar, and of late it has been, slowly, accompanied by the moaning and groaning of the Chinese leadership. But has it really gone up? Take a look at the following charts I had the guys at Variant Perception make for us.

Notice that of China’s main trading partners, the US is the only one against whose currency the yuan has risen over the last three months. If you are in the eurozone, you have seen an almost 4% rise.

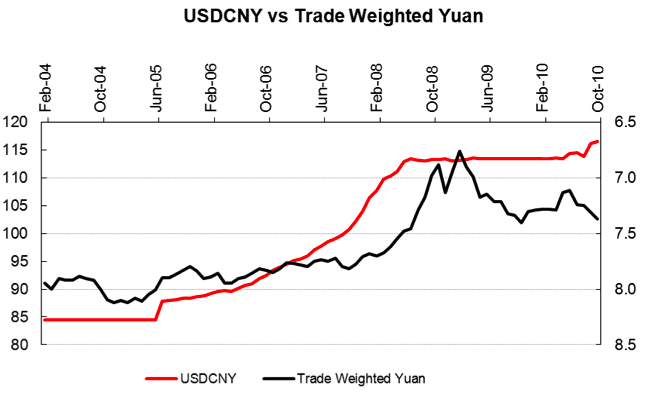

Now look at the next chart. We are comparing the Chinese yuan against the dollar and then against the trade-weighted Chinese yuan. Notice that for the last 18 months the trade-weighted yuan has dropped well over 10%! In terms of real trade with China’s real trading partners, the yuan has fallen in value! That is extraordinary.

Expect more calls from around the world for China to allow its currency to rise. And as China has to deal with inflation, it may be in their interest. We will see. But it does make you go “hmmm.”

First, Let’s Lower the Bar

I was sitting in London when the employment numbers came out last Friday, and I didn’t have time to really get into the data. I did send you Lacy Hunt’s quick analysis as to why it was weaker than it appeared, but something else did not seem right. I follow a few people who are pretty good at predicting the employment numbers (like Philippa Dunne of The Liscio Report). Most were expecting numbers in the 60,000 range. Most unusual for there to be such a big miss from these guys. I read the press release and saw nothing to raise my eyebrows. And then Alan Abelson in Barron’s gave us the following, after reciting the headline number:

“Happily, the always astute Stephanie Pomboy of MacroMavens provided a quickie explanation:

“ ‘The seasonal bar which the payroll data must jump was (inexplicably and dramatically) lowered from prior Octobers.

“ ‘Thus, in October 2009, the BLS set the bar at 870,000 jobs, similar to the 840,000 it anticipated in October 2008. This year, by contrast, it lowered the bar to 768,000. Mumbo, jumbo, payrolls presented “an upside surprise” of 100,000.’

“According to John Williams at Shadow Government Statistics, the BLS’ fiddling with the figures via what he calls ‘seasonal-factor games’ actually created 200,000 phantom jobs last month. John cites such finagling as the reason his prediction of an October decline and a rise in the jobless rate was wrong. It also explains why seasonally adjusted payrolls were revised upward by 110,000 in September, including 56,000 in August.”

In the opinion of your humble analyst, if they are going to make such changes, they should be announced up-front or noted prominently in the press release. People (foolishly) trade on these numbers and money is made and lost. This is serious stuff.

They Need to Borrow How Much? Really?

The team over at Recovery Partners sent this note along:

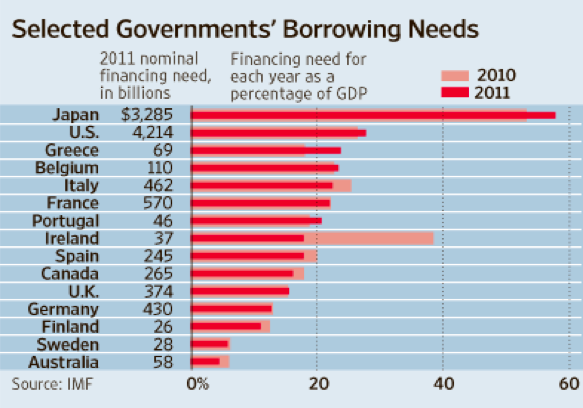

“This week we heard from the IMF that the total borrowing requirements of key governments in 2011 will amount to around $10.2 trillion. The estimate represents a rise of 7% from 2010 and over 27% of the annual GDP of the developed economies. This rollover profile exposes the vulnerabilities in the maturity composition of Sovereign liability portfolios and the likelihood that most Sovereigns will find it impossible to appropriately de-risk their financial exposures by extending term or otherwise executing an immunization strategy. The bottom line is that unless deficit control and the establishment of debt management performance benchmarks is adopted as a matter of urgency in many economies, it becomes very easy to envision the near term onset of another round of severe financial turbulence.”

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

That is obviously a lot of money. It is also government borrowing that is crowding out private investment. And as we look over the “pond,” the euro is again under pressure. Just when you thought QE2 was going to tank the dollar.

Irish Eyes Are Not Smiling

Mother Ireland (Dad said we were once Muldoons before we were kicked out) is having problems. It was only a few years ago that we talked about the Irish Miracle. They had gotten a grip on their fiscal deficits and were even running surpluses. And then came the housing bubble, and their bank problems dwarfed those (relatively) of the US.

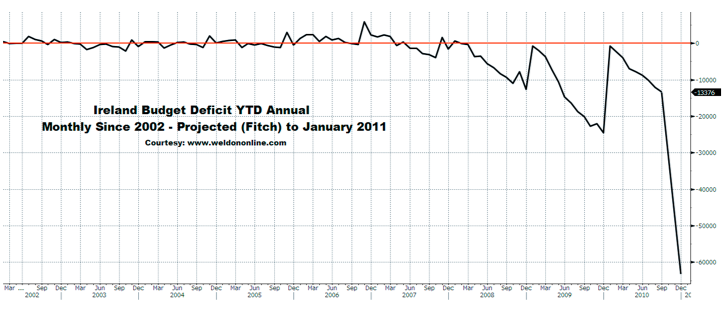

Ireland is simply not having a good go of it. They can’t seem top catch a break of late –their Irish luck is abandoning them. Let’s look at some charts from my favorite slicer and dicer of data, Greg Weldon, which just hit my inbox. After noting the rise in suicides and calls to suicide hotlines due to economic pressures on farmers (who are caught in a drought) and foreclosures, he writes:

“… the Irish Central Bank determined that Ireland’s financial institutions needed MORE capital, essentially DOUBLING the cost of the original bailout, and obliterating ANY chance for cutting the Budget Deficit in 2010. In fact, according to “The Economist”, if we were to include the cost of the financial system bailout, and, consider the decline in GDP … Ireland’s Deficit-to-GDP Ratio, already FOUR TIMES the EU’s (allegedly) ‘hard-ceiling’ of 3%, as just under 12% … would EXPLODE, to 32% !!!!

“Subsequently, on October 6th Fitch cut their sovereign debt ‘rating’ for Ireland, to AA-, from A+, in order to … ‘reflect the exceptional and greater-than-expected cost of the nation’s bailout of its banking system.’

“Then note the ‘projected’ Deficit when we include the government’s increasingly large bailout of the country’s financial institutions. Irish eyes are no longer smiling … rather, Irish eyes are crying.

“During a debate on Tuesday in the Parliament, Prime Minister Cowen said …

“ ‘… If this country and this parliament fails to make the necessary adjustments, then we put at risk the funding of the State after July of next year and what will happen then is that we will be faced with a situation where we will only be able to spend EUR 31 billion. The State could not go on spending EUR 50 billion a year, when it was only taking in EUR 31 billion. Being only able to spend EUR 31 billion would involve a serious adjustment in the level of (government) services that could be provided. No responsible government, therefore, could contemplate that approach.’

“Say what … no responsible government could contemplate spending what they take in?? Indeed, herein lies the core of the crisis … to cut spending by the amount needed to ‘fix’ the fiscal mess that European countries now find themselves facing … would be so dramatic as to cause INTENSE economic PAIN, enough so to drive even more Irish farmers, policemen, realtors, and plumbers … to suicide.”

I have been writing for years that much of Europe was in far worse shape than the US, and we are not in a good way. Irish 5-year bonds now cost 8.44%, up from below 4% in August, just three months ago. Ireland is going to have to finance debt of almost 40% of GDP this year and 20% next year. As they roll over that debt, interest-rate costs are going to skyrocket, making those budget cuts even harder.

And the same goes for Greece, Portugal, and Spain. With German Chancellor Angela Merkel having to face elections, she says her goal is to “enforce fiscal discipline in the euro area and avoid putting German taxpayer money on the line in any future bailout.” She noted at the G-20 meeting yesterday:

“There may be a conflict here between the interests of the financial world and the interests of politicians… We can’t constantly explain to our voters that taxpayers have to be on the hook for certain risks rather than those who make a lot of money taking those risks.”

This is not going to be easy. I expect it to end in tears for some of the more troubled countries. It is all so very sad.

La Jolla, New York and a Forbes Cruise

If it seems like I have been living on planes of late, I guess it’s because I have. And in another last-minute trip, Tiffani and I will go to La Jolla to meet with Jon Sundt and the management of Genworth, which has bought Altegris. I am rather enthusiastic about the new arrangement, as it opens up all sorts of possibilities.

Then I am home for a while. Thanksgiving will feature lots of kids and friends, and I am looking forward to it. I really enjoy cooking and the whole feel of the holiday. Then Tiffani and Ryan and I go to LA, where we get on a ship for the Forbes Cruise. I am looking forward to a little R&R going down the Mexican coast, and spending time with old friends and making new ones. I have to sing for my supper a few times, but I can do that. It is actually fun for me.

Like what you're reading?

Get this free newsletter in your inbox every Saturday! Read our privacy policy here.

Then a quick trip to New York in mid-December (details to be determined), and then home for the holidays and Christmas. I love this time of year.

Have a great weekend and enjoy the season.

Your ready to relax analyst,

John Mauldin

P.S. If you like my letters, you'll love reading Over My Shoulder with serious economic analysis from my global network, at a surprisingly affordable price. Click here to learn more.

Put Mauldin Economics to work in your portfolio. Your financial journey is unique, and so are your needs. That's why we suggest the following options to suit your preferences:

-

John’s curated thoughts: John Mauldin and editor Patrick Watson share the best research notes and reports of the week, along with a summary of key takeaways. In a world awash with information, John and Patrick help you find the most important insights of the week, from our network of economists and analysts. Read by over 7,500 members. See the full details here.

-

Income investing: Grow your income portfolio with our dividend investing research service, Yield Shark. Dividend analyst Kelly Green guides readers to income investments with clear suggestions and a portfolio of steady dividend payers. Click here to learn more about Yield Shark.

-

Invest in longevity: Transformative Age delivers proven ways to extend your healthy lifespan, and helps you invest in the world’s most cutting-edge health and biotech companies. See more here.

-

Macro investing: Our flagship investment research service is led by Mauldin Economics partner Ed D’Agostino. His thematic approach to investing gives you a portfolio that will benefit from the economy’s most exciting trends—before they are well known. Go here to learn more about Macro Advantage.

Read important disclosures here.

YOUR USE OF THESE MATERIALS IS SUBJECT TO THE TERMS OF THESE DISCLOSURES.

Tags

Did someone forward this article to you?

Click here to get Thoughts from the Frontline in your inbox every Saturday.